Analisis Ketersediaan Air Menggunakan Model Rain Run NRECA ...

LONG RUN IMPACT OF SHARE QUYBACK INITIATION TOWARD THE SHARE PRICE OF FIRMS LISTED IN KUALA LUMPUR STOCK EXCHANGE

Chong Chuan ei

shy

HG 6015

Corporate Master in C548

Business Administration 2013 2013

PJ~~1atMaklumat Akademik MALAYSIA SARAWAK

LONG RUN IMPACT OF SHARE BUYBACK INITIATION TOWARD THE SHARE PRICE

OF FIRMS LISTED IN KUALA LUMPUR STOCK EXCHANGE

PKHIDMAT MAKLUMAT AKADEMIK

1llllllIllliri~1111111I1 1000246892

CHONG CHUAN WEI

A thesis submitted

In fulfilment of the requirements for the degree of Corporate Master in Business Administration

bull ~ bullbull - ltshy

1 _ bullbull

Faculty of Economics and Business

UNIVERSITI MALA YSIASARAW AK

2013

Statement of Originality

The work describe in this project entitled

Long Run Impact of Share Buyback Initiation toward the Share Price of Firms t Listed in Kuala Lumpur Stock Exchange

is to the best of the author s knowledge that of the author except

where due reference is made

May 292013 Chong Chuan Wei 11031806

shy v

~ l

-

I - bull

r

ABSTRAK

Impak J(Jngka Pangjang Pembelian Balik Saham kepada Harga Saham Syarikat

tersenarai di Bursa Malaysia

Oleh

Chong Chuan Wei

Kajiall ini dijalankan untuk cuba menyiasat dan menilai impak jangka pangjang

daripada pembelian baik saham terhadap harga syarikat yang terdapat di Bursa

Malaysia Kajian ini melibatkan syarikat yang menjalankan pembelian balik saham dari

tahull 1999 sehingga tahun 2008 di Bursa Malaysia Harga syarikat akan direkod

mengikut bulan selama tiga tahun selepas pembelian pertama dijalankan Kemlldian

rekod harga saham illi akan dikira dengall menggunakan formula Buy-and-Hold BHR

dan Buy-and-Hold Abnormal Return BHAR menggunakan Kuala Lumpur Komposite

Indeks KLCI sebagai penanda aras Nilai t-statistik dikira untuk menentukan kewujudan

BHAR Nilai t-statistik menunjukkan nilai BHAR tidak sama dengan kosong Selepas ilu

nilai BHAR akan diregresi dengan nisbah buku-kepada-pasaran dan jumlah nilai

pasaran Selepas menjalankan ujian regresi tersebut kesimpulan menunjukkan bahawa

nisbah bukll-kepada-pasaran dan i]lmlah harga pasaran mempunyai kesan terhadap

~ l

BHAR

Kata kunci Pembelian Balik Saham BHR BHAR buku-kepada-pasaran harga pasaran

ABSTRACT

Long Run Impact of Share Buyback Initiation toward the Share Price of Firms Listed in Kuala Lumpur Stock Exchange

By

Chong Chuan Wei

(ThiS paper is attempted to investigate and e~aluate the long run impact of share buyback

initiation toward the share price of firms in Kuala Lumpur Stock Exchange This

research involves firms that initiated share buyback from the year of 1999 until 2008 in

Kuala Lumpur Stock EXChang~The share price is recorded every month for three years

after the first share buyback is carried out The recorded share price will later be

calculated with formula of Buy-and-Hold BHR and Buy-and-Hold Abnormal Return

BHAR by using Kuala Lumpur Composite Index as the benchmark T -statistic value is

computed manually to show the existence of BHAR value The t-statistic value computed

showed that BHAR value is not equal to zero After that BHAR value is regressed with

book-to-market ratio and market value of the firmmiddot Aftltrro~ out the regression the J L

t

conclusion found that both Book-to-Market and Market Value show relationship with

share price

Keywords Share Buyback BHR BHAR Book-to-MarketMarket Value

t f

ACKNOWLEGMENT

In the effort of making this study successful I would like to express my sincere

appreciation to my supervisor Dr Mohamad Jais for his guidance and support in the

whole process of this study Even though Dr Mohamad Jais was busy I am glad that he is

always willing to spend some time with me to discuss the study The expertise and

knowledge of my supervisor has benefited me to complete this study on time Dr

Mohamad Jais has provided me meaningful insight of the research

Besides that I would also like to express my appreciation to my course mates that

provided me valuable ideas and suggestions Furthermore I would like to express my

gratitude to my family members for their understanding and morale support in

completing this study The help and patie~ce given had strengthened me to complete this

study successfully

-

I l bull I

Pusat Khidmat Maklumat Akademik UNlVERSm MALAYSIA SARAWAK

TABLE OF CONTENTS

ABSTRACT

ABSTRAK

ACKNOWLEDMENT

CHAPTER 1 INTRODUCTION 11 OVERVIEW

12 BACKGROUND OF THE STUDY 4

713 PROBLEM STATEMENT

14 OBJECTIVE OF THE STUDY 8

15 SIGNIFICANCE OF THE STUDY 8

916 SCOPE OF THE STUDY

17 ORGANIZATION OF THE CHt-PTER 10

CHAPTER 2 LITERATURE REVIEW

21 OVERVIEW 11

22 THEORIES ON THE MOTIVES OF SHARE BUYBACK THAT 12

SUPPORT EXISTENCE OF ABNORMAL RETURNS

23 ANNOUNCEMENT IMPACTS 14 - y bull bull Y I shy bull

1 ~t bull bull

24 PRIOR STUDY ON ABNORMAL RETURN OF SHARE BUYBACK 16

FIRMS IN KLSE

25 CUMULATIVE ABNORMAL RETURN (CAR) VERSUS BUY AND 18

HOLD ABNORMAL RETURN (BHARf

1 bull ( I I

i

26 SUMMARY 20

CHAPTER 3 rnTHODOLOGY

31 OVERVIEW 21

32 DATA DESCRIPTION 21

33 METHODOLOGY 22

34 THEORETICAL FRAMEWORK

35 EMPIRICAL MODEL FOR CROSS REGRESSION

26

26

36 HYPOTHESIS DEVELOPMENT 27

37 SUMMARY 28

CHAPTER 4 RESULTS AND DISCUSSION

41 OVERVIEW 29

42 AVERAGE BUY-AND-HOLD ABNORMAL RETURNS ON THE

LONG RUN PERFORMANCE 29

43 RELATIONSHIP BETWEEN BHAR WITH MARKET VALUE AND

BOOK-TO-MARKET RATIO 32

44 SUMMARY 35

CHAPTER 5 DISCUSSION_ IMPLICATIONS LIMITATION AND

RECOMMEDA TION

51 INTRODUCTION

J

bull H

36

52 DISCUSSION 36

53 IMPLICATIONS 36 54 LImITATIONS AND RECOMMENDATION OF THE STUDY 37

55 CONCLUSION 38

~ ~

I 1 1 bull t middot

--

LIST OF TABLES

TABLE 11 mANGES IN LAWS REGARDING SHARE REPURCHASE 2

FROM 1995 TO 2001 IN THE SELECTED COUNTRIES

TABLE 31 THE DISTRIBUTION OF LISTED COMPANIES IN KLSE THAT 22

INITIA TED SHARE BUYBACK PROGRAM FROM THE YEAR

1999 UNTIL 2008

TABLE 41 DESCRIPTIVE STATISTICS OF BHAR OF INDIVIDUAL YEAR 30

FROM 1999 TO 2008

TABLE 42 DESCRIPTIVE STATISTICS OF BHR AND BHAR FROM 1 31

YEAR TO 3 YEAR AFTER SHARE BUYBACK INITIATION

TABLE 43 CORRELATION TEST BETWEEN BHAR LMV AND BTM 32

TABLE 44 DESCRIPTIVE STATISTIC OF 3 YEAR BHAR WITH 33

DIFFERENT CATEGORY OF BTM VALUE

TABLE 45 DESCRIPTIVE STATISTIC OF 3 YEAR BHAR WITH 33

DIFFERENT CATEGORY OF MV

TABLE 46 ESTIMATION RESULTS ON THE REGRESSION BETWEEN 34

BHAR AND THE INDEPENDENT X~B~S I bullbullL I

I

bull bull

I

I

LIST OF DIAGRAM

DIAGRAM 341 RELATIONSHIP BETWEEN BUY -AND-HOLD ABNORMAL 26

RETURN WITH NATURAL LOGARITHM OF MARKET

VALUE AND BOOK-TO-MARKET RATIO

~

I

LIST OF ABBREVIATIONS

middotmiddotmiddotmiddotmiddot middot-middotmiddotmiddotmiddotmiddotmiddot-middot---middotmiddot-middot--middotmiddotr-middotmiddot~-middotmiddotmiddot~-middotmiddot-middot- -----------------------_shy middotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddot1

Abbreviation i Description

1-- - -~--l--- ---- ------ -- -------- -- ~

l_~~~ _ ____ Icumulati~~~~~orma~ ~eturn ______ ____ I BHR I Buy-and-Hold Return

middotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddot _ _middotmiddot_ -middot---middotf[SHAR---- ------l Buy~a~d=HoidAb~_~aTmiddotRetu

_ _- _ _- j_-_ r-LMV ---middot ----middot--r Nat~~al L--garithmmiddot~f M~k~tVal~~

---- shy[S-TM --------middotr Book-t~~Ma~ket~ati~ middot---middot middot----- middotmiddotmiddot-middotmiddotmiddot-middotmiddotmiddot- 1I l_ _____________ J _____ ___ __ _______ ___ _ ____1

1-- j bull

-

CHAPTER 1

INTRODUCTION

10 Overview

Share repurchase happened when a company bJ ys back its own shares Then the

company has the options either to cancel or hold them as treasury share that can be reshy

issued next time (Atrill 2009) Share buyback is one of the popular options besides

giving dividend for company who wish to distribute cash back to the shareholder

Jagannathan (2000) found out that open market repurchases in United States is pro-

cyclical and used by firms with higher temporary and non-operating cash flows

compare to dividend that tends to increase steadily over time and preferred by the firms

with higher permanent operating cash flows Jagannathan (2000) stated that share

repurchase usually happen following poor stock market performance while dividends

normally increase after good company perfonnance (cited in Vemimmen Quiry

Dallocchio Fur amp Salvi 2009)

According to Damodaran (200 I) there are basically three types of share buyback

process as below

(a) open-market repurchase by buying only a s~~ll~n~~il(6~omiddotoutStaDding stock in bull

the open market _

bull tmiddot

(b) tender offer where a finn plan to repurchase a large amount of the outstanding stock

for example 10 or more The finn will announce to the shareholders by specifying the

details like prte amount and duration of the repurchase

(c) negotiated repurchases is less widely used as the finn will negotiate with one of its

stockholder who owns a substantial amount of the shanes

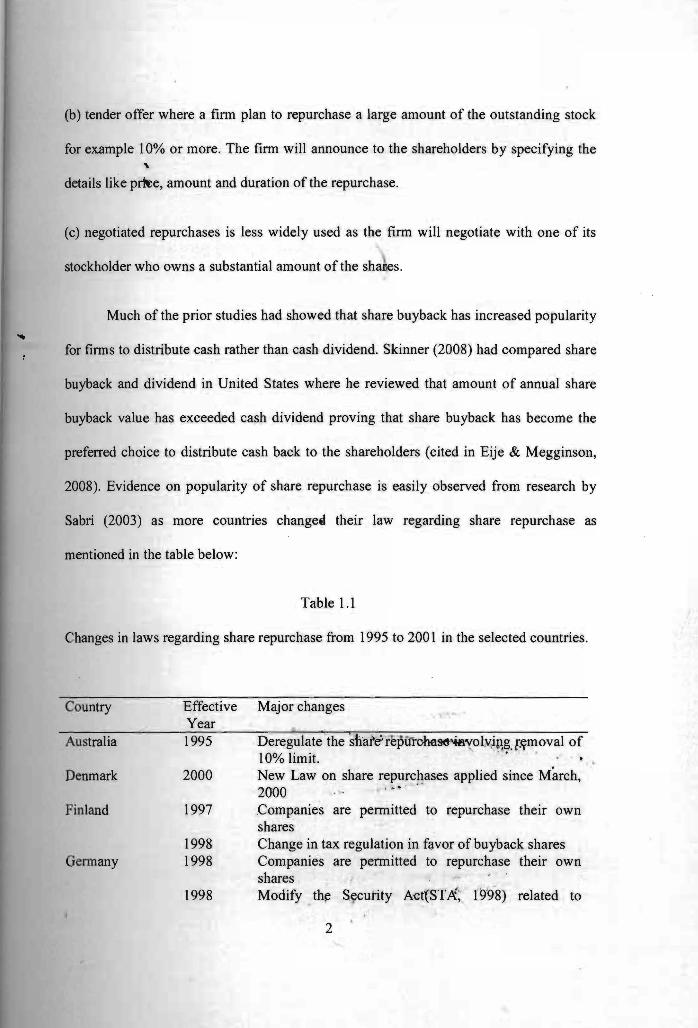

Much of the prior studies had showed that share buyback has increased popularity

for finns to distribute cash rather than cash dividend Skinner (2008) had compared share

buyback and dividend in United States where he reviewed that amount of annual share

buyback value has exceeded cash dividend proving that share buyback has become the

preferred choice to distribute cash back to the shareholders (cited in Eije amp Megginson

2008) Evidence on popularity of share repurchase is easily observed from research by

Sabri (2003) as more countries changetf their law regarding share repurchase as

mentioned in the table below

Table 11

Changes in laws regarding share repurchase from 1995 to 2001 in the selected countries

Country

Australia

Effective Year 1995

Major changes

Deregulate the ~haIe- repUroha9ltt4ftVolv~PK [~moval of 10 limit

Denmark 2000 New Law on share repurchases applied since March 2000

Finland 1997 Companies shares

are pennitted to repurchase their own

Germany 1998 1998

1998

Change in tax regulation in favor of buyback shares Companies are pennitted to repurchase their own shares Modify th~ Security Act(STA 1998) related to

2

India

Japan

Netherlands Norway

Malaysia

Singapore

New Zealand Sweden

South Africa

Taiwan

1999

1995

2001 1999

1997

1998

1999

2000 1999 2000

1999

2000

disclosures of finns buy its own share Companies are pennitted to repurchase their own shares Companies are pennitted to repurchase their own shares Changes in Tax laws to encourage buybacks of shares Companies are pennitted to repurchase their own shares A public listed companies to repurchase its own shares or to give finallcial assistance to other persons to repurchase its own shares Companies are pennitted to repurchase their own shares Approving revision of share buybacks by Singapore Monterey Authority Issue tax treatment of buyback shares The buybacks of own shares law was amended Listed companies are pennitted to repurchase their own shares Listed companies are allowed to repurchase their own share by changing the companies Act of 1973 Listed companies are allowed to repurchase their own share

United Kingdom 1999 A consultation paper regard that Investment companies middotto be allowed to repurchase their own shares using capital profits

1996 A consultation paper regard to financial assistance by a company for the acquisition its own share

Sources Adopted from the finding by Sabri (2003) Using Treasury Repurchase Share to Stabilize

Stock Markets International Journal Of Business 8(4) 2003

There are also lots of studies that reviewed the purpose of inns repurchasing their

shares Among those Vemimmen Quiry Dallocchio Fur and Salvi (2009) stated several

possible reasons for share buybacks as below bull pr bull ~

(a) lack of better investment opportunity that cause Jllanager return excess funds for

shareholders to seek investment elsewhere

(b) managers give signal for goods news in future believing the shares are undervalued I

3

- I

(c) tax incentive as share buy backs is not taxable compare to paying dividend

(d) transferring value between shareholders who refuse to sell and shareholders who

~

accept the offer

(e) change leverage ratio by adjusting amount of equity

(t) prevent take over

(g) counter the dilution effect of share options

(h) provide managers tlexibiiity to make small adjustments in the capital structure and

etc

Generally share repurchase is believed to help the company achieving increase

in earnings per share (PIE) as the number of outstanding equity reduces However there are also arguments about this manipulation where the increase of PIE ratio is

accompanied with higher debt ratio which will post risk to the stability of the company

(Demodaran 2001)

12 Background of the study

Since share buyback was allowed in Malaysia on 1 September 1997 it is

increasingly gaining attention as compani~s st~ftea fo middotbii~~ its ~aros in large volume Based on the study by Is~ Ghani a~~ Lee on Malaysia listed company from

2001 to 2005 there were 149 firms with a total of 17864 repurchases days and total

purchase of 2309313664 shares This number is expected to increase as share

t I bull

4

=-shy I

pusat Khidmat Maklumat Akade~ UNIVERSm MALAYSIA SARAW

repurchase evolved to become a useful financial tool that is carried out by the

management to distribute excess cash to shareholders other than paying dividend

As share buyback is becoming commonly carried out many researches have been

done on announcement impact of share buyback Some the researches also reviewed that

share buyback announcement may not be carried ou as stated and hence it did not

generate positive impacts to the share price in the long run (Zhang 2002) Much fewer

researches were done on long tenn impact of actual share buyback as it required

significant amount of data that some stock exchange did not enclose

Although open market share repurchase is regularly being studied in United

States researchers nonnally encounter trouble in getting actual repurchase data as United

States has a general lack of disclosure requirement associated with share repurchase In

United States listed finn can buy back its own shares without making any

announcements and finns that already made announcements are under no obligation to

implement their proposed plans (Brockman amp Chung 2012) Thus this is difficult for

researcher to study the impact of actual share repurchases especially those that require

detail timing prices or magnitudes of the repurchases

In my study the issue of data does not occur as KLSE has a full disclosure on

share buyback In Malaysia a listed corporation middotltfanoniY1Ufcbas4its Qwn shares after ~ t middot t

getting authorization of its shareholders in a general meeting The share repurchase is

subject to rules under the Companies Act 1965 section 67 A and Part lIlA of the

Companies Regulations 1966 The shareholders will be infonned either through a

statement accompanying its notice of general meeting or a circular After the general

5

meeting that is called to consider the proposed share repurchase the listed corporation

must implediately announce the outcome to the stock exchange A listed corporation in

KLSE is only aJ1owed to purchase or hold not more than 10 of its issued and paid-up

capital

After a repurchase is carried out the listed corporation must immediately

announce to KLSE not later than 630pm on the day the purchase is made This

announcement will have to contain the detail as below

(a) date of purchase

(b) description of shares purchased

(0) number of shares purchased

(d) price of each share or where relevant the highest and lowest price paid

(e) total consideration paid

(0 number of shares purchased retained in treasury

(g) number of share purchased which are proposed to be cancelled

(h) cumulative net outstanding treasury s~ares at the date of notification where ~~ - ~ ~~

j bull bull L t

applicable

(i) where all or any of the shares are proposed to be cancelled the adjusted share capital

bull t r I

lt bull

6

13 Problem statement

Studyon abnormal return of share price for share buyback firms had been carried

out numerously across the countries that initiated share buyback Much of these studies

had indicated that there exists positive return on the share price either short run or long

run after share buyback announcement or actual sh~re buyback initiation Most of the

previous studies about share buyback in Malaysia were focus on share buyback

announcement and short term studies following the actual share repurchases As Malaysia

only allowed share buyback since 1 September 1997 it posts difficulties for the previous

researchers to study on the long run impacts after share buyback initiation as limited

numbers of data is available Therefore research on long run impact is crucial to clarify

whether there exits any long run abnormal return by comparing with the Kuala Lumpur

Composite Index KLCI as the benchmark

Other than that obtaining abnormal return is always the primary aim of deciding

any stock investment By assuming management has better timing and upfront

infonnation share repurchase would signal a good entry to gain an abnormal return

Therefore this study will benefit all the market participants towards long run impact of

share buyback initiation With data easily available in the Kuala Lumpur Stock

Exchange KLSE website it will be an in~eres~i~g topic to discover the relationship of - -111 ~ II

actual share buyback and its share price

- In order to streamline the large numbers of share buyback companies and further

identify those that really contribute to abnormal return characteristics of those companies

are investigated as well The long run return computed will be later linked to the specific i_ [ I

7

characteristic of these individual companies namely book-to-market ratio (BTM) and

marketyalue (MV) which are characteristics commonly study in the prior studies

14 Research Objectives

141 General Objective

This study aims to determine the long run abnormal return for firms that chose to initiate

share buyback program from 1999 to 2008 in Kuala Lumpur Stock Exchange

142 Specific Objectives

(a) To investigate the long run abnormal return of share repurchases to share price of

the repurchase firms from 1999 to 2008

(b) Investigate the relationship of long run abnormal return of share buyback companies with its market value (MV) and book-to-market (BTM) ratio

15 Significant of the study

As share buyback only initiated in Kuala Lumpur Exchange (KLSE) since 1997

very few publish journal have been done to review its relationship with its share price

Only few published journal was found to study on the short term announcement impact

using Cumulative Abnormal Return CAR This itpto15abiyo6e1hthe srn~JJI1umber of companies participating in share b~yback when the prsram is approved that become

limitation to the previous study As a result there exists the need to study the impact of

share buyback to the share price in a longer duration

If

) ~

8

_ - - - --

Other than that as investors always looking for indicators to achieve abnonnal

retuTJ in the stock market share repurchase that is said to have signaling effect will

probably be agood sign to buy or sell a stock Asymmetry infonnation lead many market

participants especially the retail investor to confuse on the intention of share buyback It

is still unknown whether share buyback really benefited the shareholders This proves

that it is important for this study to examine whether there exist any long run abnonnal

return after share buyback initiation so that it can be used as an indicator for market

participants

16 Scope of the study

This study intends to examine the long run impact of actual share buyback

initiation towards its share price of listed companies in Kuala Lumpur Exchange (KLSE)

The share buyback companies that will be covered are from 1 January 1999 until 31

December 2008 Each of these share buyback company will later be tracked down for

monthly perfonnance using Buy-and-Hold Abnonnal Return(BHAR) method starting

from the first day of initiating share buyback program until for the end of the three years

to examine the long run impact of share repurchase towards its share price Each of this

BHAR value will later be regressed with the book-to-market ratio (BTM) and natural

logarithm of market value (MV) to examine the ~~istence of any relationship bull ~ ~ j-

l ~ l i

I I bull

9

=========~--- ---- -- ----------------==-----------shy

17 Organization of the chapter

Chapt~r one covers introduction on the concept of share repurchase and the

happening around the listed nations It will also involve list of related research and issue

on share repurchase Chapter two involves literature review about the previous research It will review

several theories on share buyback that support existence of positive return research on

impact of announcement and actual repurchase characteristics of the share buyback

companies that possess abnormal returns the methodologies and others

Chapter 3 contains discussion on data coHection where the source will be stated

clearly The theoretical framework will be reviewed in detail follow by the derivation of

empirical model of this study and the method to be used for this study

Chapter 4 contains the result and detail discussion by compare and contrast with

previous findings The empirical result will be interpreted and discussed

Chapter 5 will contain the conclusion of this study policy implications and

limitation of the study

y ~ ~

bull [~ I

~ o

10

CHAPTER 2

LITERATURE REVIEW

21 Overview

As share buyback only initiated in Malaysia on 1997 after Asian Financial Crisis

there are still very few published journals found related to the issue of share buyback in

Malaysia One of the few published journal found is Market Reaction to Actual Share

Repurchase in Malaysia by Isa Ghani and Lee in 2011 which also stated in the journal

that they only found a published journal before their study which is Price Reaction to

Stock Repurchases Evidence from KLSE done by Lim and Bacha in 2002

In this chapter discussion will be started with motives behind the initiation of

share buyback that support existence of abnormal returns followed with previous finding

on the performance of share price following share repurchase As mentioned previously

due to relatively few published journal abotrt share repurchase in the Malaysia context

much of the argument will be based on previous research done in foreign countries that

may have some different behaviours from Malaysias situation

I

II

22 Theories on the motives of share buyback that support existence of abnormal

returns There e many theories about the reasons a company conducts a share buyback

Among the most popular theories that regularly being studied are signaling effects free

cash flows dividend substitution defensive strategies changing capital structures and

others In 2000 Ditmar did a research to test the motives of share buyback in United

States involving repurchase from the year 1977 till 1996 In his research he cited the

failure of previous research in determining the motives of share buyback where they only

tested a few motives neglecting other potential factors Therefore by using a censored

regression analysis he tested five motives of share buyback as below

(a) Excess Capital Hypothesis Repurchases and Distribution Policy

(b) Undervaluation Hypothesis Repurchases and Investment Policy

(c) Optimal Leverage Ratio Hypothesis Repurchases and Capital Structure Policy

(d) Management Incentive Hypothesis Repurchases and Compensation Policy

(e) Takeover Deterrence Hypothesis Repurchases and Corporate Control

Ditmar found out that it is possible that firms to repurchase stock for several reasons and

the statistics result support the hypothesis of excess capital the optimal leverage ratio the

undervaluation and the takeover deterrence

Lee and Suh in 20 II found that- the amOUI)ts of ~hare repurchases across countries bull - bull --- ~ bull ~1 bull 0

are significantly associated with large cash holdings Their study indicated that fmhs

across countries that repurchase share usually hold large amount of excess cash and

experience raised in amount of cash holdings prior to repurchases The increases in

excess cash appear to be achieved from decrease in capital ~xpen~iture instead of

l bull [ I I

12

PJ~~1atMaklumat Akademik MALAYSIA SARAWAK

LONG RUN IMPACT OF SHARE BUYBACK INITIATION TOWARD THE SHARE PRICE

OF FIRMS LISTED IN KUALA LUMPUR STOCK EXCHANGE

PKHIDMAT MAKLUMAT AKADEMIK

1llllllIllliri~1111111I1 1000246892

CHONG CHUAN WEI

A thesis submitted

In fulfilment of the requirements for the degree of Corporate Master in Business Administration

bull ~ bullbull - ltshy

1 _ bullbull

Faculty of Economics and Business

UNIVERSITI MALA YSIASARAW AK

2013

Statement of Originality

The work describe in this project entitled

Long Run Impact of Share Buyback Initiation toward the Share Price of Firms t Listed in Kuala Lumpur Stock Exchange

is to the best of the author s knowledge that of the author except

where due reference is made

May 292013 Chong Chuan Wei 11031806

shy v

~ l

-

I - bull

r

ABSTRAK

Impak J(Jngka Pangjang Pembelian Balik Saham kepada Harga Saham Syarikat

tersenarai di Bursa Malaysia

Oleh

Chong Chuan Wei

Kajiall ini dijalankan untuk cuba menyiasat dan menilai impak jangka pangjang

daripada pembelian baik saham terhadap harga syarikat yang terdapat di Bursa

Malaysia Kajian ini melibatkan syarikat yang menjalankan pembelian balik saham dari

tahull 1999 sehingga tahun 2008 di Bursa Malaysia Harga syarikat akan direkod

mengikut bulan selama tiga tahun selepas pembelian pertama dijalankan Kemlldian

rekod harga saham illi akan dikira dengall menggunakan formula Buy-and-Hold BHR

dan Buy-and-Hold Abnormal Return BHAR menggunakan Kuala Lumpur Komposite

Indeks KLCI sebagai penanda aras Nilai t-statistik dikira untuk menentukan kewujudan

BHAR Nilai t-statistik menunjukkan nilai BHAR tidak sama dengan kosong Selepas ilu

nilai BHAR akan diregresi dengan nisbah buku-kepada-pasaran dan jumlah nilai

pasaran Selepas menjalankan ujian regresi tersebut kesimpulan menunjukkan bahawa

nisbah bukll-kepada-pasaran dan i]lmlah harga pasaran mempunyai kesan terhadap

~ l

BHAR

Kata kunci Pembelian Balik Saham BHR BHAR buku-kepada-pasaran harga pasaran

ABSTRACT

Long Run Impact of Share Buyback Initiation toward the Share Price of Firms Listed in Kuala Lumpur Stock Exchange

By

Chong Chuan Wei

(ThiS paper is attempted to investigate and e~aluate the long run impact of share buyback

initiation toward the share price of firms in Kuala Lumpur Stock Exchange This

research involves firms that initiated share buyback from the year of 1999 until 2008 in

Kuala Lumpur Stock EXChang~The share price is recorded every month for three years

after the first share buyback is carried out The recorded share price will later be

calculated with formula of Buy-and-Hold BHR and Buy-and-Hold Abnormal Return

BHAR by using Kuala Lumpur Composite Index as the benchmark T -statistic value is

computed manually to show the existence of BHAR value The t-statistic value computed

showed that BHAR value is not equal to zero After that BHAR value is regressed with

book-to-market ratio and market value of the firmmiddot Aftltrro~ out the regression the J L

t

conclusion found that both Book-to-Market and Market Value show relationship with

share price

Keywords Share Buyback BHR BHAR Book-to-MarketMarket Value

t f

ACKNOWLEGMENT

In the effort of making this study successful I would like to express my sincere

appreciation to my supervisor Dr Mohamad Jais for his guidance and support in the

whole process of this study Even though Dr Mohamad Jais was busy I am glad that he is

always willing to spend some time with me to discuss the study The expertise and

knowledge of my supervisor has benefited me to complete this study on time Dr

Mohamad Jais has provided me meaningful insight of the research

Besides that I would also like to express my appreciation to my course mates that

provided me valuable ideas and suggestions Furthermore I would like to express my

gratitude to my family members for their understanding and morale support in

completing this study The help and patie~ce given had strengthened me to complete this

study successfully

-

I l bull I

Pusat Khidmat Maklumat Akademik UNlVERSm MALAYSIA SARAWAK

TABLE OF CONTENTS

ABSTRACT

ABSTRAK

ACKNOWLEDMENT

CHAPTER 1 INTRODUCTION 11 OVERVIEW

12 BACKGROUND OF THE STUDY 4

713 PROBLEM STATEMENT

14 OBJECTIVE OF THE STUDY 8

15 SIGNIFICANCE OF THE STUDY 8

916 SCOPE OF THE STUDY

17 ORGANIZATION OF THE CHt-PTER 10

CHAPTER 2 LITERATURE REVIEW

21 OVERVIEW 11

22 THEORIES ON THE MOTIVES OF SHARE BUYBACK THAT 12

SUPPORT EXISTENCE OF ABNORMAL RETURNS

23 ANNOUNCEMENT IMPACTS 14 - y bull bull Y I shy bull

1 ~t bull bull

24 PRIOR STUDY ON ABNORMAL RETURN OF SHARE BUYBACK 16

FIRMS IN KLSE

25 CUMULATIVE ABNORMAL RETURN (CAR) VERSUS BUY AND 18

HOLD ABNORMAL RETURN (BHARf

1 bull ( I I

i

26 SUMMARY 20

CHAPTER 3 rnTHODOLOGY

31 OVERVIEW 21

32 DATA DESCRIPTION 21

33 METHODOLOGY 22

34 THEORETICAL FRAMEWORK

35 EMPIRICAL MODEL FOR CROSS REGRESSION

26

26

36 HYPOTHESIS DEVELOPMENT 27

37 SUMMARY 28

CHAPTER 4 RESULTS AND DISCUSSION

41 OVERVIEW 29

42 AVERAGE BUY-AND-HOLD ABNORMAL RETURNS ON THE

LONG RUN PERFORMANCE 29

43 RELATIONSHIP BETWEEN BHAR WITH MARKET VALUE AND

BOOK-TO-MARKET RATIO 32

44 SUMMARY 35

CHAPTER 5 DISCUSSION_ IMPLICATIONS LIMITATION AND

RECOMMEDA TION

51 INTRODUCTION

J

bull H

36

52 DISCUSSION 36

53 IMPLICATIONS 36 54 LImITATIONS AND RECOMMENDATION OF THE STUDY 37

55 CONCLUSION 38

~ ~

I 1 1 bull t middot

--

LIST OF TABLES

TABLE 11 mANGES IN LAWS REGARDING SHARE REPURCHASE 2

FROM 1995 TO 2001 IN THE SELECTED COUNTRIES

TABLE 31 THE DISTRIBUTION OF LISTED COMPANIES IN KLSE THAT 22

INITIA TED SHARE BUYBACK PROGRAM FROM THE YEAR

1999 UNTIL 2008

TABLE 41 DESCRIPTIVE STATISTICS OF BHAR OF INDIVIDUAL YEAR 30

FROM 1999 TO 2008

TABLE 42 DESCRIPTIVE STATISTICS OF BHR AND BHAR FROM 1 31

YEAR TO 3 YEAR AFTER SHARE BUYBACK INITIATION

TABLE 43 CORRELATION TEST BETWEEN BHAR LMV AND BTM 32

TABLE 44 DESCRIPTIVE STATISTIC OF 3 YEAR BHAR WITH 33

DIFFERENT CATEGORY OF BTM VALUE

TABLE 45 DESCRIPTIVE STATISTIC OF 3 YEAR BHAR WITH 33

DIFFERENT CATEGORY OF MV

TABLE 46 ESTIMATION RESULTS ON THE REGRESSION BETWEEN 34

BHAR AND THE INDEPENDENT X~B~S I bullbullL I

I

bull bull

I

I

LIST OF DIAGRAM

DIAGRAM 341 RELATIONSHIP BETWEEN BUY -AND-HOLD ABNORMAL 26

RETURN WITH NATURAL LOGARITHM OF MARKET

VALUE AND BOOK-TO-MARKET RATIO

~

I

LIST OF ABBREVIATIONS

middotmiddotmiddotmiddotmiddot middot-middotmiddotmiddotmiddotmiddotmiddot-middot---middotmiddot-middot--middotmiddotr-middotmiddot~-middotmiddotmiddot~-middotmiddot-middot- -----------------------_shy middotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddot1

Abbreviation i Description

1-- - -~--l--- ---- ------ -- -------- -- ~

l_~~~ _ ____ Icumulati~~~~~orma~ ~eturn ______ ____ I BHR I Buy-and-Hold Return

middotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddot _ _middotmiddot_ -middot---middotf[SHAR---- ------l Buy~a~d=HoidAb~_~aTmiddotRetu

_ _- _ _- j_-_ r-LMV ---middot ----middot--r Nat~~al L--garithmmiddot~f M~k~tVal~~

---- shy[S-TM --------middotr Book-t~~Ma~ket~ati~ middot---middot middot----- middotmiddotmiddot-middotmiddotmiddot-middotmiddotmiddot- 1I l_ _____________ J _____ ___ __ _______ ___ _ ____1

1-- j bull

-

CHAPTER 1

INTRODUCTION

10 Overview

Share repurchase happened when a company bJ ys back its own shares Then the

company has the options either to cancel or hold them as treasury share that can be reshy

issued next time (Atrill 2009) Share buyback is one of the popular options besides

giving dividend for company who wish to distribute cash back to the shareholder

Jagannathan (2000) found out that open market repurchases in United States is pro-

cyclical and used by firms with higher temporary and non-operating cash flows

compare to dividend that tends to increase steadily over time and preferred by the firms

with higher permanent operating cash flows Jagannathan (2000) stated that share

repurchase usually happen following poor stock market performance while dividends

normally increase after good company perfonnance (cited in Vemimmen Quiry

Dallocchio Fur amp Salvi 2009)

According to Damodaran (200 I) there are basically three types of share buyback

process as below

(a) open-market repurchase by buying only a s~~ll~n~~il(6~omiddotoutStaDding stock in bull

the open market _

bull tmiddot

(b) tender offer where a finn plan to repurchase a large amount of the outstanding stock

for example 10 or more The finn will announce to the shareholders by specifying the

details like prte amount and duration of the repurchase

(c) negotiated repurchases is less widely used as the finn will negotiate with one of its

stockholder who owns a substantial amount of the shanes

Much of the prior studies had showed that share buyback has increased popularity

for finns to distribute cash rather than cash dividend Skinner (2008) had compared share

buyback and dividend in United States where he reviewed that amount of annual share

buyback value has exceeded cash dividend proving that share buyback has become the

preferred choice to distribute cash back to the shareholders (cited in Eije amp Megginson

2008) Evidence on popularity of share repurchase is easily observed from research by

Sabri (2003) as more countries changetf their law regarding share repurchase as

mentioned in the table below

Table 11

Changes in laws regarding share repurchase from 1995 to 2001 in the selected countries

Country

Australia

Effective Year 1995

Major changes

Deregulate the ~haIe- repUroha9ltt4ftVolv~PK [~moval of 10 limit

Denmark 2000 New Law on share repurchases applied since March 2000

Finland 1997 Companies shares

are pennitted to repurchase their own

Germany 1998 1998

1998

Change in tax regulation in favor of buyback shares Companies are pennitted to repurchase their own shares Modify th~ Security Act(STA 1998) related to

2

India

Japan

Netherlands Norway

Malaysia

Singapore

New Zealand Sweden

South Africa

Taiwan

1999

1995

2001 1999

1997

1998

1999

2000 1999 2000

1999

2000

disclosures of finns buy its own share Companies are pennitted to repurchase their own shares Companies are pennitted to repurchase their own shares Changes in Tax laws to encourage buybacks of shares Companies are pennitted to repurchase their own shares A public listed companies to repurchase its own shares or to give finallcial assistance to other persons to repurchase its own shares Companies are pennitted to repurchase their own shares Approving revision of share buybacks by Singapore Monterey Authority Issue tax treatment of buyback shares The buybacks of own shares law was amended Listed companies are pennitted to repurchase their own shares Listed companies are allowed to repurchase their own share by changing the companies Act of 1973 Listed companies are allowed to repurchase their own share

United Kingdom 1999 A consultation paper regard that Investment companies middotto be allowed to repurchase their own shares using capital profits

1996 A consultation paper regard to financial assistance by a company for the acquisition its own share

Sources Adopted from the finding by Sabri (2003) Using Treasury Repurchase Share to Stabilize

Stock Markets International Journal Of Business 8(4) 2003

There are also lots of studies that reviewed the purpose of inns repurchasing their

shares Among those Vemimmen Quiry Dallocchio Fur and Salvi (2009) stated several

possible reasons for share buybacks as below bull pr bull ~

(a) lack of better investment opportunity that cause Jllanager return excess funds for

shareholders to seek investment elsewhere

(b) managers give signal for goods news in future believing the shares are undervalued I

3

- I

(c) tax incentive as share buy backs is not taxable compare to paying dividend

(d) transferring value between shareholders who refuse to sell and shareholders who

~

accept the offer

(e) change leverage ratio by adjusting amount of equity

(t) prevent take over

(g) counter the dilution effect of share options

(h) provide managers tlexibiiity to make small adjustments in the capital structure and

etc

Generally share repurchase is believed to help the company achieving increase

in earnings per share (PIE) as the number of outstanding equity reduces However there are also arguments about this manipulation where the increase of PIE ratio is

accompanied with higher debt ratio which will post risk to the stability of the company

(Demodaran 2001)

12 Background of the study

Since share buyback was allowed in Malaysia on 1 September 1997 it is

increasingly gaining attention as compani~s st~ftea fo middotbii~~ its ~aros in large volume Based on the study by Is~ Ghani a~~ Lee on Malaysia listed company from

2001 to 2005 there were 149 firms with a total of 17864 repurchases days and total

purchase of 2309313664 shares This number is expected to increase as share

t I bull

4

=-shy I

pusat Khidmat Maklumat Akade~ UNIVERSm MALAYSIA SARAW

repurchase evolved to become a useful financial tool that is carried out by the

management to distribute excess cash to shareholders other than paying dividend

As share buyback is becoming commonly carried out many researches have been

done on announcement impact of share buyback Some the researches also reviewed that

share buyback announcement may not be carried ou as stated and hence it did not

generate positive impacts to the share price in the long run (Zhang 2002) Much fewer

researches were done on long tenn impact of actual share buyback as it required

significant amount of data that some stock exchange did not enclose

Although open market share repurchase is regularly being studied in United

States researchers nonnally encounter trouble in getting actual repurchase data as United

States has a general lack of disclosure requirement associated with share repurchase In

United States listed finn can buy back its own shares without making any

announcements and finns that already made announcements are under no obligation to

implement their proposed plans (Brockman amp Chung 2012) Thus this is difficult for

researcher to study the impact of actual share repurchases especially those that require

detail timing prices or magnitudes of the repurchases

In my study the issue of data does not occur as KLSE has a full disclosure on

share buyback In Malaysia a listed corporation middotltfanoniY1Ufcbas4its Qwn shares after ~ t middot t

getting authorization of its shareholders in a general meeting The share repurchase is

subject to rules under the Companies Act 1965 section 67 A and Part lIlA of the

Companies Regulations 1966 The shareholders will be infonned either through a

statement accompanying its notice of general meeting or a circular After the general

5

meeting that is called to consider the proposed share repurchase the listed corporation

must implediately announce the outcome to the stock exchange A listed corporation in

KLSE is only aJ1owed to purchase or hold not more than 10 of its issued and paid-up

capital

After a repurchase is carried out the listed corporation must immediately

announce to KLSE not later than 630pm on the day the purchase is made This

announcement will have to contain the detail as below

(a) date of purchase

(b) description of shares purchased

(0) number of shares purchased

(d) price of each share or where relevant the highest and lowest price paid

(e) total consideration paid

(0 number of shares purchased retained in treasury

(g) number of share purchased which are proposed to be cancelled

(h) cumulative net outstanding treasury s~ares at the date of notification where ~~ - ~ ~~

j bull bull L t

applicable

(i) where all or any of the shares are proposed to be cancelled the adjusted share capital

bull t r I

lt bull

6

13 Problem statement

Studyon abnormal return of share price for share buyback firms had been carried

out numerously across the countries that initiated share buyback Much of these studies

had indicated that there exists positive return on the share price either short run or long

run after share buyback announcement or actual sh~re buyback initiation Most of the

previous studies about share buyback in Malaysia were focus on share buyback

announcement and short term studies following the actual share repurchases As Malaysia

only allowed share buyback since 1 September 1997 it posts difficulties for the previous

researchers to study on the long run impacts after share buyback initiation as limited

numbers of data is available Therefore research on long run impact is crucial to clarify

whether there exits any long run abnormal return by comparing with the Kuala Lumpur

Composite Index KLCI as the benchmark

Other than that obtaining abnormal return is always the primary aim of deciding

any stock investment By assuming management has better timing and upfront

infonnation share repurchase would signal a good entry to gain an abnormal return

Therefore this study will benefit all the market participants towards long run impact of

share buyback initiation With data easily available in the Kuala Lumpur Stock

Exchange KLSE website it will be an in~eres~i~g topic to discover the relationship of - -111 ~ II

actual share buyback and its share price

- In order to streamline the large numbers of share buyback companies and further

identify those that really contribute to abnormal return characteristics of those companies

are investigated as well The long run return computed will be later linked to the specific i_ [ I

7

characteristic of these individual companies namely book-to-market ratio (BTM) and

marketyalue (MV) which are characteristics commonly study in the prior studies

14 Research Objectives

141 General Objective

This study aims to determine the long run abnormal return for firms that chose to initiate

share buyback program from 1999 to 2008 in Kuala Lumpur Stock Exchange

142 Specific Objectives

(a) To investigate the long run abnormal return of share repurchases to share price of

the repurchase firms from 1999 to 2008

(b) Investigate the relationship of long run abnormal return of share buyback companies with its market value (MV) and book-to-market (BTM) ratio

15 Significant of the study

As share buyback only initiated in Kuala Lumpur Exchange (KLSE) since 1997

very few publish journal have been done to review its relationship with its share price

Only few published journal was found to study on the short term announcement impact

using Cumulative Abnormal Return CAR This itpto15abiyo6e1hthe srn~JJI1umber of companies participating in share b~yback when the prsram is approved that become

limitation to the previous study As a result there exists the need to study the impact of

share buyback to the share price in a longer duration

If

) ~

8

_ - - - --

Other than that as investors always looking for indicators to achieve abnonnal

retuTJ in the stock market share repurchase that is said to have signaling effect will

probably be agood sign to buy or sell a stock Asymmetry infonnation lead many market

participants especially the retail investor to confuse on the intention of share buyback It

is still unknown whether share buyback really benefited the shareholders This proves

that it is important for this study to examine whether there exist any long run abnonnal

return after share buyback initiation so that it can be used as an indicator for market

participants

16 Scope of the study

This study intends to examine the long run impact of actual share buyback

initiation towards its share price of listed companies in Kuala Lumpur Exchange (KLSE)

The share buyback companies that will be covered are from 1 January 1999 until 31

December 2008 Each of these share buyback company will later be tracked down for

monthly perfonnance using Buy-and-Hold Abnonnal Return(BHAR) method starting

from the first day of initiating share buyback program until for the end of the three years

to examine the long run impact of share repurchase towards its share price Each of this

BHAR value will later be regressed with the book-to-market ratio (BTM) and natural

logarithm of market value (MV) to examine the ~~istence of any relationship bull ~ ~ j-

l ~ l i

I I bull

9

=========~--- ---- -- ----------------==-----------shy

17 Organization of the chapter

Chapt~r one covers introduction on the concept of share repurchase and the

happening around the listed nations It will also involve list of related research and issue

on share repurchase Chapter two involves literature review about the previous research It will review

several theories on share buyback that support existence of positive return research on

impact of announcement and actual repurchase characteristics of the share buyback

companies that possess abnormal returns the methodologies and others

Chapter 3 contains discussion on data coHection where the source will be stated

clearly The theoretical framework will be reviewed in detail follow by the derivation of

empirical model of this study and the method to be used for this study

Chapter 4 contains the result and detail discussion by compare and contrast with

previous findings The empirical result will be interpreted and discussed

Chapter 5 will contain the conclusion of this study policy implications and

limitation of the study

y ~ ~

bull [~ I

~ o

10

CHAPTER 2

LITERATURE REVIEW

21 Overview

As share buyback only initiated in Malaysia on 1997 after Asian Financial Crisis

there are still very few published journals found related to the issue of share buyback in

Malaysia One of the few published journal found is Market Reaction to Actual Share

Repurchase in Malaysia by Isa Ghani and Lee in 2011 which also stated in the journal

that they only found a published journal before their study which is Price Reaction to

Stock Repurchases Evidence from KLSE done by Lim and Bacha in 2002

In this chapter discussion will be started with motives behind the initiation of

share buyback that support existence of abnormal returns followed with previous finding

on the performance of share price following share repurchase As mentioned previously

due to relatively few published journal abotrt share repurchase in the Malaysia context

much of the argument will be based on previous research done in foreign countries that

may have some different behaviours from Malaysias situation

I

II

22 Theories on the motives of share buyback that support existence of abnormal

returns There e many theories about the reasons a company conducts a share buyback

Among the most popular theories that regularly being studied are signaling effects free

cash flows dividend substitution defensive strategies changing capital structures and

others In 2000 Ditmar did a research to test the motives of share buyback in United

States involving repurchase from the year 1977 till 1996 In his research he cited the

failure of previous research in determining the motives of share buyback where they only

tested a few motives neglecting other potential factors Therefore by using a censored

regression analysis he tested five motives of share buyback as below

(a) Excess Capital Hypothesis Repurchases and Distribution Policy

(b) Undervaluation Hypothesis Repurchases and Investment Policy

(c) Optimal Leverage Ratio Hypothesis Repurchases and Capital Structure Policy

(d) Management Incentive Hypothesis Repurchases and Compensation Policy

(e) Takeover Deterrence Hypothesis Repurchases and Corporate Control

Ditmar found out that it is possible that firms to repurchase stock for several reasons and

the statistics result support the hypothesis of excess capital the optimal leverage ratio the

undervaluation and the takeover deterrence

Lee and Suh in 20 II found that- the amOUI)ts of ~hare repurchases across countries bull - bull --- ~ bull ~1 bull 0

are significantly associated with large cash holdings Their study indicated that fmhs

across countries that repurchase share usually hold large amount of excess cash and

experience raised in amount of cash holdings prior to repurchases The increases in

excess cash appear to be achieved from decrease in capital ~xpen~iture instead of

l bull [ I I

12

Statement of Originality

The work describe in this project entitled

Long Run Impact of Share Buyback Initiation toward the Share Price of Firms t Listed in Kuala Lumpur Stock Exchange

is to the best of the author s knowledge that of the author except

where due reference is made

May 292013 Chong Chuan Wei 11031806

shy v

~ l

-

I - bull

r

ABSTRAK

Impak J(Jngka Pangjang Pembelian Balik Saham kepada Harga Saham Syarikat

tersenarai di Bursa Malaysia

Oleh

Chong Chuan Wei

Kajiall ini dijalankan untuk cuba menyiasat dan menilai impak jangka pangjang

daripada pembelian baik saham terhadap harga syarikat yang terdapat di Bursa

Malaysia Kajian ini melibatkan syarikat yang menjalankan pembelian balik saham dari

tahull 1999 sehingga tahun 2008 di Bursa Malaysia Harga syarikat akan direkod

mengikut bulan selama tiga tahun selepas pembelian pertama dijalankan Kemlldian

rekod harga saham illi akan dikira dengall menggunakan formula Buy-and-Hold BHR

dan Buy-and-Hold Abnormal Return BHAR menggunakan Kuala Lumpur Komposite

Indeks KLCI sebagai penanda aras Nilai t-statistik dikira untuk menentukan kewujudan

BHAR Nilai t-statistik menunjukkan nilai BHAR tidak sama dengan kosong Selepas ilu

nilai BHAR akan diregresi dengan nisbah buku-kepada-pasaran dan jumlah nilai

pasaran Selepas menjalankan ujian regresi tersebut kesimpulan menunjukkan bahawa

nisbah bukll-kepada-pasaran dan i]lmlah harga pasaran mempunyai kesan terhadap

~ l

BHAR

Kata kunci Pembelian Balik Saham BHR BHAR buku-kepada-pasaran harga pasaran

ABSTRACT

Long Run Impact of Share Buyback Initiation toward the Share Price of Firms Listed in Kuala Lumpur Stock Exchange

By

Chong Chuan Wei

(ThiS paper is attempted to investigate and e~aluate the long run impact of share buyback

initiation toward the share price of firms in Kuala Lumpur Stock Exchange This

research involves firms that initiated share buyback from the year of 1999 until 2008 in

Kuala Lumpur Stock EXChang~The share price is recorded every month for three years

after the first share buyback is carried out The recorded share price will later be

calculated with formula of Buy-and-Hold BHR and Buy-and-Hold Abnormal Return

BHAR by using Kuala Lumpur Composite Index as the benchmark T -statistic value is

computed manually to show the existence of BHAR value The t-statistic value computed

showed that BHAR value is not equal to zero After that BHAR value is regressed with

book-to-market ratio and market value of the firmmiddot Aftltrro~ out the regression the J L

t

conclusion found that both Book-to-Market and Market Value show relationship with

share price

Keywords Share Buyback BHR BHAR Book-to-MarketMarket Value

t f

ACKNOWLEGMENT

In the effort of making this study successful I would like to express my sincere

appreciation to my supervisor Dr Mohamad Jais for his guidance and support in the

whole process of this study Even though Dr Mohamad Jais was busy I am glad that he is

always willing to spend some time with me to discuss the study The expertise and

knowledge of my supervisor has benefited me to complete this study on time Dr

Mohamad Jais has provided me meaningful insight of the research

Besides that I would also like to express my appreciation to my course mates that

provided me valuable ideas and suggestions Furthermore I would like to express my

gratitude to my family members for their understanding and morale support in

completing this study The help and patie~ce given had strengthened me to complete this

study successfully

-

I l bull I

Pusat Khidmat Maklumat Akademik UNlVERSm MALAYSIA SARAWAK

TABLE OF CONTENTS

ABSTRACT

ABSTRAK

ACKNOWLEDMENT

CHAPTER 1 INTRODUCTION 11 OVERVIEW

12 BACKGROUND OF THE STUDY 4

713 PROBLEM STATEMENT

14 OBJECTIVE OF THE STUDY 8

15 SIGNIFICANCE OF THE STUDY 8

916 SCOPE OF THE STUDY

17 ORGANIZATION OF THE CHt-PTER 10

CHAPTER 2 LITERATURE REVIEW

21 OVERVIEW 11

22 THEORIES ON THE MOTIVES OF SHARE BUYBACK THAT 12

SUPPORT EXISTENCE OF ABNORMAL RETURNS

23 ANNOUNCEMENT IMPACTS 14 - y bull bull Y I shy bull

1 ~t bull bull

24 PRIOR STUDY ON ABNORMAL RETURN OF SHARE BUYBACK 16

FIRMS IN KLSE

25 CUMULATIVE ABNORMAL RETURN (CAR) VERSUS BUY AND 18

HOLD ABNORMAL RETURN (BHARf

1 bull ( I I

i

26 SUMMARY 20

CHAPTER 3 rnTHODOLOGY

31 OVERVIEW 21

32 DATA DESCRIPTION 21

33 METHODOLOGY 22

34 THEORETICAL FRAMEWORK

35 EMPIRICAL MODEL FOR CROSS REGRESSION

26

26

36 HYPOTHESIS DEVELOPMENT 27

37 SUMMARY 28

CHAPTER 4 RESULTS AND DISCUSSION

41 OVERVIEW 29

42 AVERAGE BUY-AND-HOLD ABNORMAL RETURNS ON THE

LONG RUN PERFORMANCE 29

43 RELATIONSHIP BETWEEN BHAR WITH MARKET VALUE AND

BOOK-TO-MARKET RATIO 32

44 SUMMARY 35

CHAPTER 5 DISCUSSION_ IMPLICATIONS LIMITATION AND

RECOMMEDA TION

51 INTRODUCTION

J

bull H

36

52 DISCUSSION 36

53 IMPLICATIONS 36 54 LImITATIONS AND RECOMMENDATION OF THE STUDY 37

55 CONCLUSION 38

~ ~

I 1 1 bull t middot

--

LIST OF TABLES

TABLE 11 mANGES IN LAWS REGARDING SHARE REPURCHASE 2

FROM 1995 TO 2001 IN THE SELECTED COUNTRIES

TABLE 31 THE DISTRIBUTION OF LISTED COMPANIES IN KLSE THAT 22

INITIA TED SHARE BUYBACK PROGRAM FROM THE YEAR

1999 UNTIL 2008

TABLE 41 DESCRIPTIVE STATISTICS OF BHAR OF INDIVIDUAL YEAR 30

FROM 1999 TO 2008

TABLE 42 DESCRIPTIVE STATISTICS OF BHR AND BHAR FROM 1 31

YEAR TO 3 YEAR AFTER SHARE BUYBACK INITIATION

TABLE 43 CORRELATION TEST BETWEEN BHAR LMV AND BTM 32

TABLE 44 DESCRIPTIVE STATISTIC OF 3 YEAR BHAR WITH 33

DIFFERENT CATEGORY OF BTM VALUE

TABLE 45 DESCRIPTIVE STATISTIC OF 3 YEAR BHAR WITH 33

DIFFERENT CATEGORY OF MV

TABLE 46 ESTIMATION RESULTS ON THE REGRESSION BETWEEN 34

BHAR AND THE INDEPENDENT X~B~S I bullbullL I

I

bull bull

I

I

LIST OF DIAGRAM

DIAGRAM 341 RELATIONSHIP BETWEEN BUY -AND-HOLD ABNORMAL 26

RETURN WITH NATURAL LOGARITHM OF MARKET

VALUE AND BOOK-TO-MARKET RATIO

~

I

LIST OF ABBREVIATIONS

middotmiddotmiddotmiddotmiddot middot-middotmiddotmiddotmiddotmiddotmiddot-middot---middotmiddot-middot--middotmiddotr-middotmiddot~-middotmiddotmiddot~-middotmiddot-middot- -----------------------_shy middotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddot1

Abbreviation i Description

1-- - -~--l--- ---- ------ -- -------- -- ~

l_~~~ _ ____ Icumulati~~~~~orma~ ~eturn ______ ____ I BHR I Buy-and-Hold Return

middotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddotmiddot _ _middotmiddot_ -middot---middotf[SHAR---- ------l Buy~a~d=HoidAb~_~aTmiddotRetu

_ _- _ _- j_-_ r-LMV ---middot ----middot--r Nat~~al L--garithmmiddot~f M~k~tVal~~

---- shy[S-TM --------middotr Book-t~~Ma~ket~ati~ middot---middot middot----- middotmiddotmiddot-middotmiddotmiddot-middotmiddotmiddot- 1I l_ _____________ J _____ ___ __ _______ ___ _ ____1

1-- j bull

-

CHAPTER 1

INTRODUCTION

10 Overview

Share repurchase happened when a company bJ ys back its own shares Then the

company has the options either to cancel or hold them as treasury share that can be reshy

issued next time (Atrill 2009) Share buyback is one of the popular options besides

giving dividend for company who wish to distribute cash back to the shareholder

Jagannathan (2000) found out that open market repurchases in United States is pro-

cyclical and used by firms with higher temporary and non-operating cash flows

compare to dividend that tends to increase steadily over time and preferred by the firms

with higher permanent operating cash flows Jagannathan (2000) stated that share

repurchase usually happen following poor stock market performance while dividends

normally increase after good company perfonnance (cited in Vemimmen Quiry

Dallocchio Fur amp Salvi 2009)

According to Damodaran (200 I) there are basically three types of share buyback

process as below

(a) open-market repurchase by buying only a s~~ll~n~~il(6~omiddotoutStaDding stock in bull

the open market _

bull tmiddot

(b) tender offer where a finn plan to repurchase a large amount of the outstanding stock

for example 10 or more The finn will announce to the shareholders by specifying the

details like prte amount and duration of the repurchase

(c) negotiated repurchases is less widely used as the finn will negotiate with one of its

stockholder who owns a substantial amount of the shanes

Much of the prior studies had showed that share buyback has increased popularity

for finns to distribute cash rather than cash dividend Skinner (2008) had compared share

buyback and dividend in United States where he reviewed that amount of annual share

buyback value has exceeded cash dividend proving that share buyback has become the

preferred choice to distribute cash back to the shareholders (cited in Eije amp Megginson

2008) Evidence on popularity of share repurchase is easily observed from research by

Sabri (2003) as more countries changetf their law regarding share repurchase as

mentioned in the table below

Table 11

Changes in laws regarding share repurchase from 1995 to 2001 in the selected countries

Country

Australia

Effective Year 1995

Major changes

Deregulate the ~haIe- repUroha9ltt4ftVolv~PK [~moval of 10 limit

Denmark 2000 New Law on share repurchases applied since March 2000

Finland 1997 Companies shares

are pennitted to repurchase their own

Germany 1998 1998

1998

Change in tax regulation in favor of buyback shares Companies are pennitted to repurchase their own shares Modify th~ Security Act(STA 1998) related to

2

India

Japan

Netherlands Norway

Malaysia

Singapore

New Zealand Sweden

South Africa

Taiwan

1999

1995

2001 1999

1997

1998

1999

2000 1999 2000

1999

2000

disclosures of finns buy its own share Companies are pennitted to repurchase their own shares Companies are pennitted to repurchase their own shares Changes in Tax laws to encourage buybacks of shares Companies are pennitted to repurchase their own shares A public listed companies to repurchase its own shares or to give finallcial assistance to other persons to repurchase its own shares Companies are pennitted to repurchase their own shares Approving revision of share buybacks by Singapore Monterey Authority Issue tax treatment of buyback shares The buybacks of own shares law was amended Listed companies are pennitted to repurchase their own shares Listed companies are allowed to repurchase their own share by changing the companies Act of 1973 Listed companies are allowed to repurchase their own share

United Kingdom 1999 A consultation paper regard that Investment companies middotto be allowed to repurchase their own shares using capital profits

1996 A consultation paper regard to financial assistance by a company for the acquisition its own share

Sources Adopted from the finding by Sabri (2003) Using Treasury Repurchase Share to Stabilize

Stock Markets International Journal Of Business 8(4) 2003

There are also lots of studies that reviewed the purpose of inns repurchasing their

shares Among those Vemimmen Quiry Dallocchio Fur and Salvi (2009) stated several

possible reasons for share buybacks as below bull pr bull ~

(a) lack of better investment opportunity that cause Jllanager return excess funds for

shareholders to seek investment elsewhere

(b) managers give signal for goods news in future believing the shares are undervalued I

3

- I

(c) tax incentive as share buy backs is not taxable compare to paying dividend

(d) transferring value between shareholders who refuse to sell and shareholders who

~

accept the offer

(e) change leverage ratio by adjusting amount of equity

(t) prevent take over

(g) counter the dilution effect of share options

(h) provide managers tlexibiiity to make small adjustments in the capital structure and

etc

Generally share repurchase is believed to help the company achieving increase

in earnings per share (PIE) as the number of outstanding equity reduces However there are also arguments about this manipulation where the increase of PIE ratio is

accompanied with higher debt ratio which will post risk to the stability of the company

(Demodaran 2001)

12 Background of the study

Since share buyback was allowed in Malaysia on 1 September 1997 it is

increasingly gaining attention as compani~s st~ftea fo middotbii~~ its ~aros in large volume Based on the study by Is~ Ghani a~~ Lee on Malaysia listed company from

2001 to 2005 there were 149 firms with a total of 17864 repurchases days and total

purchase of 2309313664 shares This number is expected to increase as share

t I bull

4

=-shy I

pusat Khidmat Maklumat Akade~ UNIVERSm MALAYSIA SARAW

repurchase evolved to become a useful financial tool that is carried out by the

management to distribute excess cash to shareholders other than paying dividend

As share buyback is becoming commonly carried out many researches have been

done on announcement impact of share buyback Some the researches also reviewed that

share buyback announcement may not be carried ou as stated and hence it did not

generate positive impacts to the share price in the long run (Zhang 2002) Much fewer

researches were done on long tenn impact of actual share buyback as it required

significant amount of data that some stock exchange did not enclose

Although open market share repurchase is regularly being studied in United

States researchers nonnally encounter trouble in getting actual repurchase data as United

States has a general lack of disclosure requirement associated with share repurchase In

United States listed finn can buy back its own shares without making any

announcements and finns that already made announcements are under no obligation to

implement their proposed plans (Brockman amp Chung 2012) Thus this is difficult for

researcher to study the impact of actual share repurchases especially those that require

detail timing prices or magnitudes of the repurchases

In my study the issue of data does not occur as KLSE has a full disclosure on

share buyback In Malaysia a listed corporation middotltfanoniY1Ufcbas4its Qwn shares after ~ t middot t

getting authorization of its shareholders in a general meeting The share repurchase is

subject to rules under the Companies Act 1965 section 67 A and Part lIlA of the

Companies Regulations 1966 The shareholders will be infonned either through a

statement accompanying its notice of general meeting or a circular After the general

5

meeting that is called to consider the proposed share repurchase the listed corporation

must implediately announce the outcome to the stock exchange A listed corporation in

KLSE is only aJ1owed to purchase or hold not more than 10 of its issued and paid-up

capital

After a repurchase is carried out the listed corporation must immediately

announce to KLSE not later than 630pm on the day the purchase is made This

announcement will have to contain the detail as below

(a) date of purchase

(b) description of shares purchased

(0) number of shares purchased

(d) price of each share or where relevant the highest and lowest price paid

(e) total consideration paid

(0 number of shares purchased retained in treasury

(g) number of share purchased which are proposed to be cancelled

(h) cumulative net outstanding treasury s~ares at the date of notification where ~~ - ~ ~~

j bull bull L t

applicable

(i) where all or any of the shares are proposed to be cancelled the adjusted share capital

bull t r I

lt bull

6

13 Problem statement

Studyon abnormal return of share price for share buyback firms had been carried

out numerously across the countries that initiated share buyback Much of these studies

had indicated that there exists positive return on the share price either short run or long

run after share buyback announcement or actual sh~re buyback initiation Most of the

previous studies about share buyback in Malaysia were focus on share buyback

announcement and short term studies following the actual share repurchases As Malaysia

only allowed share buyback since 1 September 1997 it posts difficulties for the previous

researchers to study on the long run impacts after share buyback initiation as limited

numbers of data is available Therefore research on long run impact is crucial to clarify

whether there exits any long run abnormal return by comparing with the Kuala Lumpur

Composite Index KLCI as the benchmark

Other than that obtaining abnormal return is always the primary aim of deciding

any stock investment By assuming management has better timing and upfront

infonnation share repurchase would signal a good entry to gain an abnormal return

Therefore this study will benefit all the market participants towards long run impact of

share buyback initiation With data easily available in the Kuala Lumpur Stock

Exchange KLSE website it will be an in~eres~i~g topic to discover the relationship of - -111 ~ II

actual share buyback and its share price

- In order to streamline the large numbers of share buyback companies and further

identify those that really contribute to abnormal return characteristics of those companies

are investigated as well The long run return computed will be later linked to the specific i_ [ I

7

characteristic of these individual companies namely book-to-market ratio (BTM) and

marketyalue (MV) which are characteristics commonly study in the prior studies

14 Research Objectives

141 General Objective

This study aims to determine the long run abnormal return for firms that chose to initiate

share buyback program from 1999 to 2008 in Kuala Lumpur Stock Exchange

142 Specific Objectives

(a) To investigate the long run abnormal return of share repurchases to share price of

the repurchase firms from 1999 to 2008

(b) Investigate the relationship of long run abnormal return of share buyback companies with its market value (MV) and book-to-market (BTM) ratio

15 Significant of the study

As share buyback only initiated in Kuala Lumpur Exchange (KLSE) since 1997

very few publish journal have been done to review its relationship with its share price

Only few published journal was found to study on the short term announcement impact

using Cumulative Abnormal Return CAR This itpto15abiyo6e1hthe srn~JJI1umber of companies participating in share b~yback when the prsram is approved that become

limitation to the previous study As a result there exists the need to study the impact of

share buyback to the share price in a longer duration

If

) ~

8

_ - - - --

Other than that as investors always looking for indicators to achieve abnonnal

retuTJ in the stock market share repurchase that is said to have signaling effect will

probably be agood sign to buy or sell a stock Asymmetry infonnation lead many market

participants especially the retail investor to confuse on the intention of share buyback It

is still unknown whether share buyback really benefited the shareholders This proves

that it is important for this study to examine whether there exist any long run abnonnal

return after share buyback initiation so that it can be used as an indicator for market

participants

16 Scope of the study

This study intends to examine the long run impact of actual share buyback

initiation towards its share price of listed companies in Kuala Lumpur Exchange (KLSE)

The share buyback companies that will be covered are from 1 January 1999 until 31

December 2008 Each of these share buyback company will later be tracked down for

monthly perfonnance using Buy-and-Hold Abnonnal Return(BHAR) method starting

from the first day of initiating share buyback program until for the end of the three years

to examine the long run impact of share repurchase towards its share price Each of this

BHAR value will later be regressed with the book-to-market ratio (BTM) and natural

logarithm of market value (MV) to examine the ~~istence of any relationship bull ~ ~ j-

l ~ l i

I I bull

9

=========~--- ---- -- ----------------==-----------shy

17 Organization of the chapter

Chapt~r one covers introduction on the concept of share repurchase and the

happening around the listed nations It will also involve list of related research and issue

on share repurchase Chapter two involves literature review about the previous research It will review

several theories on share buyback that support existence of positive return research on

impact of announcement and actual repurchase characteristics of the share buyback

companies that possess abnormal returns the methodologies and others

Chapter 3 contains discussion on data coHection where the source will be stated

clearly The theoretical framework will be reviewed in detail follow by the derivation of

empirical model of this study and the method to be used for this study

Chapter 4 contains the result and detail discussion by compare and contrast with

previous findings The empirical result will be interpreted and discussed

Chapter 5 will contain the conclusion of this study policy implications and

limitation of the study

y ~ ~

bull [~ I

~ o

10

CHAPTER 2

LITERATURE REVIEW

21 Overview

As share buyback only initiated in Malaysia on 1997 after Asian Financial Crisis

there are still very few published journals found related to the issue of share buyback in

Malaysia One of the few published journal found is Market Reaction to Actual Share

Repurchase in Malaysia by Isa Ghani and Lee in 2011 which also stated in the journal

that they only found a published journal before their study which is Price Reaction to

Stock Repurchases Evidence from KLSE done by Lim and Bacha in 2002

In this chapter discussion will be started with motives behind the initiation of

share buyback that support existence of abnormal returns followed with previous finding

on the performance of share price following share repurchase As mentioned previously

due to relatively few published journal abotrt share repurchase in the Malaysia context

much of the argument will be based on previous research done in foreign countries that

may have some different behaviours from Malaysias situation

I

II

22 Theories on the motives of share buyback that support existence of abnormal

returns There e many theories about the reasons a company conducts a share buyback

Among the most popular theories that regularly being studied are signaling effects free

cash flows dividend substitution defensive strategies changing capital structures and

others In 2000 Ditmar did a research to test the motives of share buyback in United

States involving repurchase from the year 1977 till 1996 In his research he cited the

failure of previous research in determining the motives of share buyback where they only

tested a few motives neglecting other potential factors Therefore by using a censored

regression analysis he tested five motives of share buyback as below

(a) Excess Capital Hypothesis Repurchases and Distribution Policy

(b) Undervaluation Hypothesis Repurchases and Investment Policy

(c) Optimal Leverage Ratio Hypothesis Repurchases and Capital Structure Policy

(d) Management Incentive Hypothesis Repurchases and Compensation Policy

(e) Takeover Deterrence Hypothesis Repurchases and Corporate Control

Ditmar found out that it is possible that firms to repurchase stock for several reasons and

the statistics result support the hypothesis of excess capital the optimal leverage ratio the

undervaluation and the takeover deterrence

Lee and Suh in 20 II found that- the amOUI)ts of ~hare repurchases across countries bull - bull --- ~ bull ~1 bull 0

are significantly associated with large cash holdings Their study indicated that fmhs

across countries that repurchase share usually hold large amount of excess cash and

experience raised in amount of cash holdings prior to repurchases The increases in