Sidang Akhbar Prestasi Ekonomi Suku Pertama Tahun 2019 · 2 Sidang akhbar akan meliputi Prestasi...

28

Prestasi Ekonomi Suku Pertama Tahun 2019 Gabenor Bank Negara Malaysia 16 Mei 2019 Sidang Akhbar

-

Upload

hoangthien -

Category

Documents

-

view

221 -

download

0

Transcript of Sidang Akhbar Prestasi Ekonomi Suku Pertama Tahun 2019 · 2 Sidang akhbar akan meliputi Prestasi...

Prestasi Ekonomi Suku Pertama Tahun 2019

Gabenor

Bank Negara Malaysia

16 Mei 2019

Sidang Akhbar

2

Sidang akhbar akan meliputi

Prestasi ekonomi pada suku pertama 2019

Perkembangan monetari dan kewangan

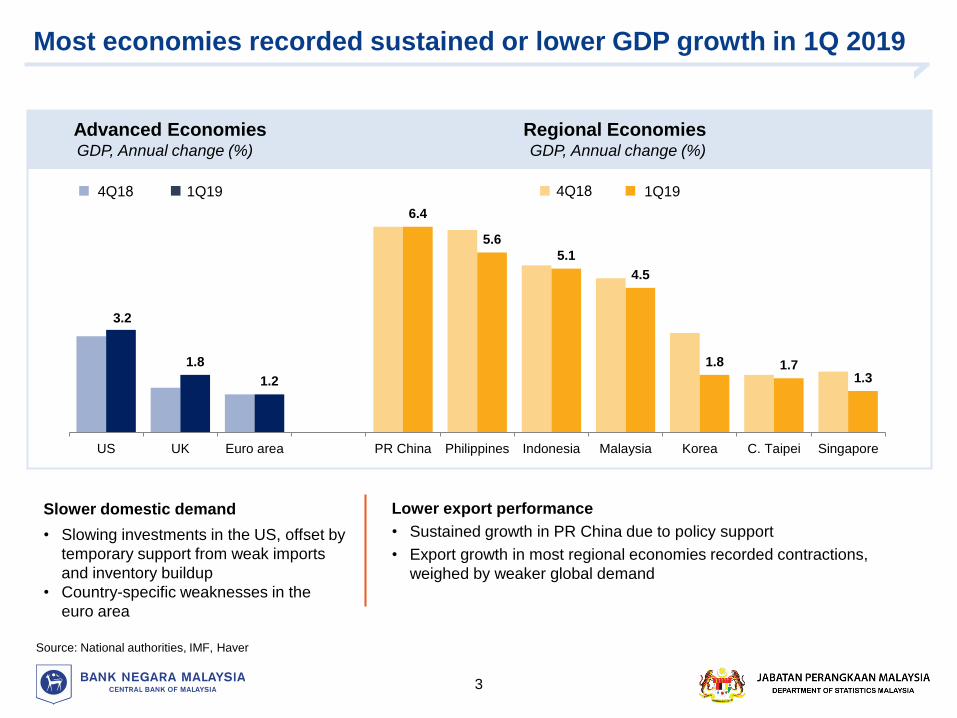

Most economies recorded sustained or lower GDP growth in 1Q 2019

3

Advanced Economies Regional EconomiesGDP, Annual change (%) GDP, Annual change (%)

4Q18 1Q19

Lower export performance

• Sustained growth in PR China due to policy support

• Export growth in most regional economies recorded contractions,

weighed by weaker global demand

Slower domestic demand

• Slowing investments in the US, offset by

temporary support from weak imports

and inventory buildup

• Country-specific weaknesses in the

euro area

4Q18 1Q19

Source: National authorities, IMF, Haver

3.2

1.8

1.2

6.4

5.6

5.1

4.5

1.8 1.71.3

US UK Euro area PR China Philippines Indonesia Malaysia Korea C. Taipei Singapore

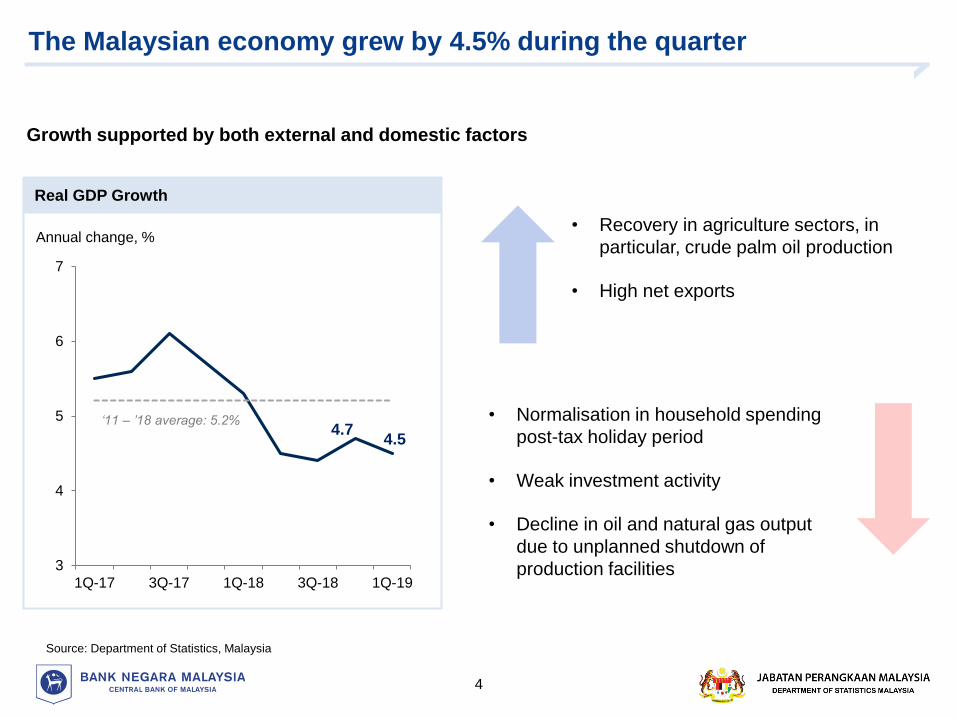

The Malaysian economy grew by 4.5% during the quarter

4

Growth supported by both external and domestic factors

• Normalisation in household spending

post-tax holiday period

• Weak investment activity

• Decline in oil and natural gas output

due to unplanned shutdown of

production facilities

• Recovery in agriculture sectors, in

particular, crude palm oil production

• High net exports

Annual change, %

4.74.5

3

4

5

6

7

1Q-17 3Q-17 1Q-18 3Q-18 1Q-19

‘11 – ’18 average: 5.2%

Real GDP Growth

Source: Department of Statistics, Malaysia

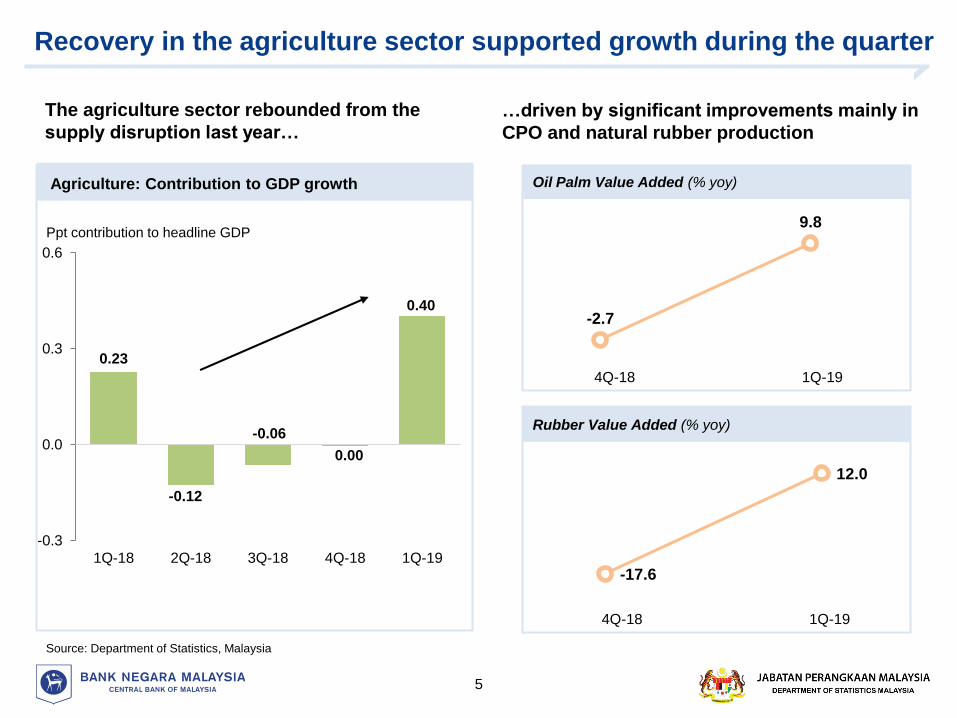

0.23

-0.12

-0.06

0.00

0.40

-0.3

0.0

0.3

0.6

1Q-18 2Q-18 3Q-18 4Q-18 1Q-19

Recovery in the agriculture sector supported growth during the quarter

5

Source: Department of Statistics, Malaysia

Ppt contribution to headline GDP

…driven by significant improvements mainly in

CPO and natural rubber production

The agriculture sector rebounded from the

supply disruption last year…

Agriculture: Contribution to GDP growth

-2.7

9.8

Oil Palm Value Added (% yoy)

4Q-18 1Q-19

Rubber Value Added (% yoy)

4Q-18 1Q-19

-17.6

12.0

-2

0

2

4

6

1Q-18 2Q-18 3Q-18 4Q-18 1Q-19

Agriculture MiningConstruction ManufacturingServices GDP Growth

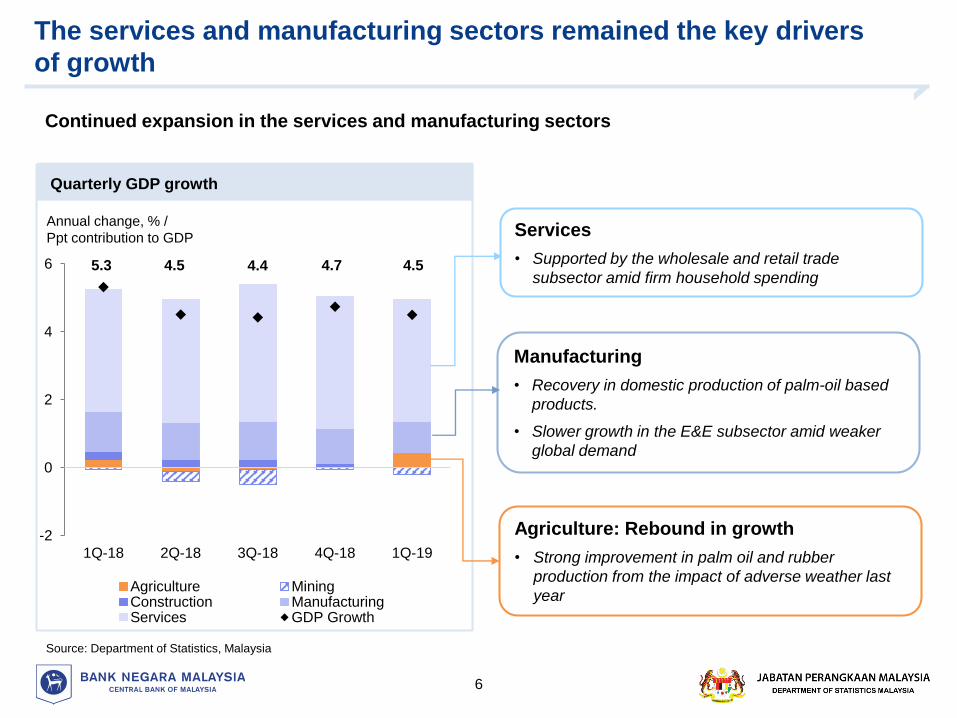

The services and manufacturing sectors remained the key drivers

of growth

6

Source: Department of Statistics, Malaysia

Annual change, % /

Ppt contribution to GDP

Agriculture: Rebound in growth

• Strong improvement in palm oil and rubber

production from the impact of adverse weather last

year

Services

• Supported by the wholesale and retail trade

subsector amid firm household spending

Continued expansion in the services and manufacturing sectors

4.75.3 4.5 4.4

Quarterly GDP growth

4.5

Manufacturing

• Recovery in domestic production of palm-oil based

products.

• Slower growth in the E&E subsector amid weaker

global demand

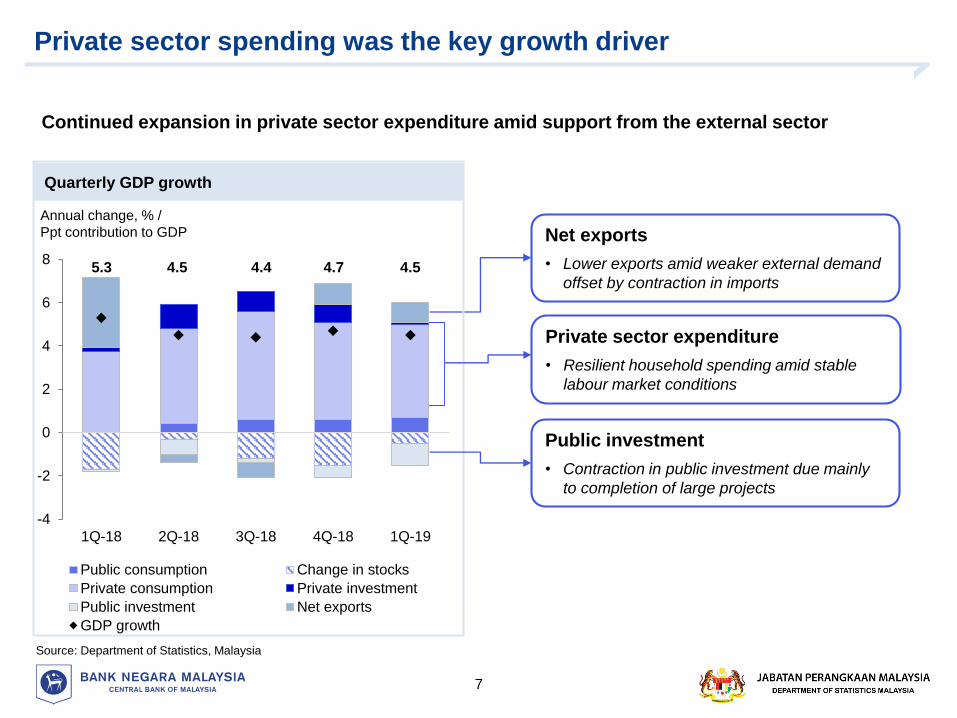

Continued expansion in private sector expenditure amid support from the external sector

Source: Department of Statistics, Malaysia

Private sector spending was the key growth driver

Private sector expenditure

• Resilient household spending amid stable

labour market conditions

Net exports

• Lower exports amid weaker external demand

offset by contraction in imports

Annual change, % /

Ppt contribution to GDP

Quarterly GDP growth

Public investment

• Contraction in public investment due mainly

to completion of large projects

-4

-2

0

2

4

6

8

1Q-18 2Q-18 3Q-18 4Q-18 1Q-19

Public consumption Change in stocks

Private consumption Private investment

Public investment Net exports

GDP growth

5.3 4.5 4.4 4.7 4.5

7

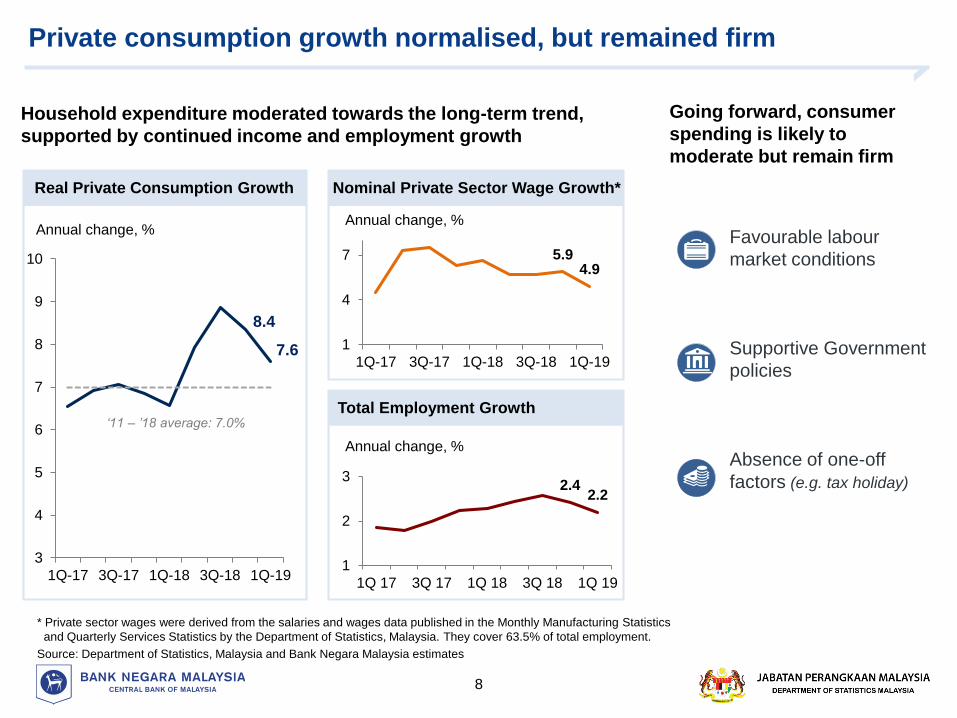

Private consumption growth normalised, but remained firm

8

* Private sector wages were derived from the salaries and wages data published in the Monthly Manufacturing Statistics

and Quarterly Services Statistics by the Department of Statistics, Malaysia. They cover 63.5% of total employment.

Source: Department of Statistics, Malaysia and Bank Negara Malaysia estimates

Household expenditure moderated towards the long-term trend,

supported by continued income and employment growth

Annual change, %

8.4

7.6

3

4

5

6

7

8

9

10

1Q-17 3Q-17 1Q-18 3Q-18 1Q-19

‘11 – ’18 average: 7.0%

Going forward, consumer

spending is likely to

moderate but remain firm

5.94.9

1

4

7

1Q-17 3Q-17 1Q-18 3Q-18 1Q-19

Real Private Consumption Growth

Annual change, %

Nominal Private Sector Wage Growth*

2.42.2

1

2

3

1Q 17 3Q 17 1Q 18 3Q 18 1Q 19

Annual change, %

Total Employment Growth

Favourable labour

market conditions

Supportive Government

policies

Absence of one-off

factors (e.g. tax holiday)

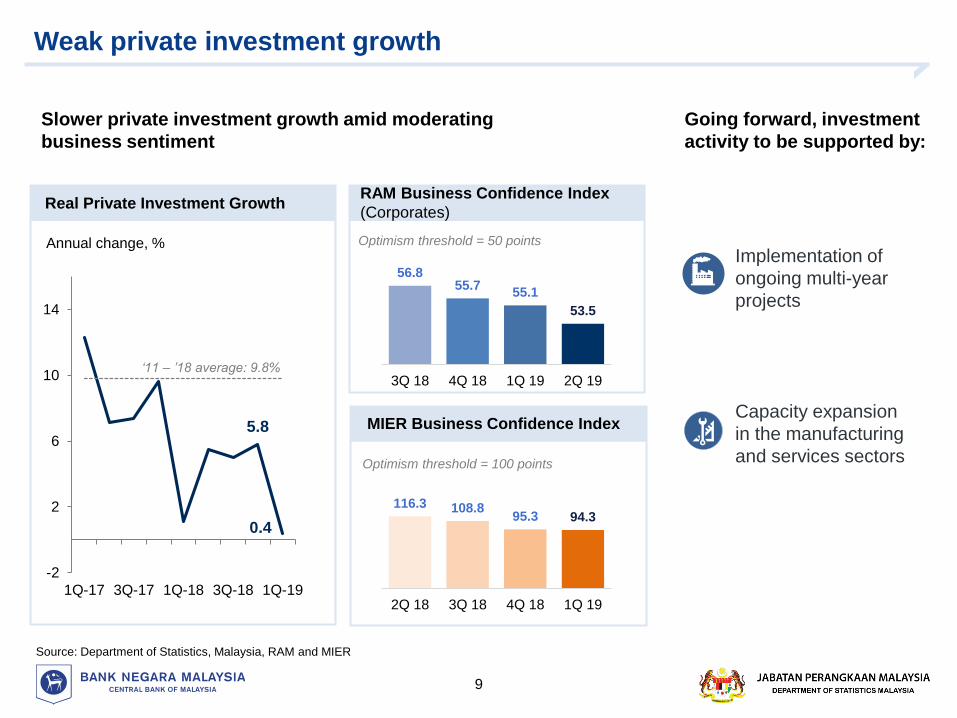

Weak private investment growth

9

5.8

0.4

-2

2

6

10

14

1Q-17 3Q-17 1Q-18 3Q-18 1Q-19

Source: Department of Statistics, Malaysia, RAM and MIER

‘11 – ’18 average: 9.8%

Annual change, %

RAM Business Confidence Index

(Corporates)

Slower private investment growth amid moderating

business sentiment

Real Private Investment Growth

Going forward, investment

activity to be supported by:

Implementation of

ongoing multi-year

projects

Optimism threshold = 50 points

56.855.7

55.1

53.5

3Q 18 4Q 18 1Q 19 2Q 19

MIER Business Confidence Index

116.3 108.895.3 94.3

2Q 18 3Q 18 4Q 18 1Q 19

Optimism threshold = 100 points

Capacity expansion

in the manufacturing

and services sectors

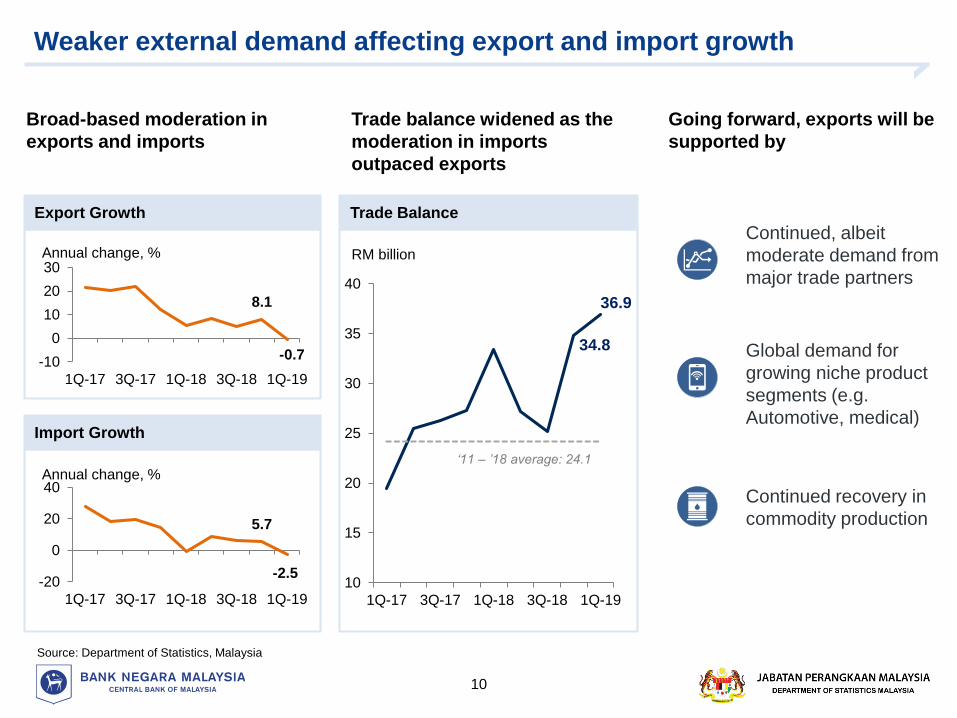

Weaker external demand affecting export and import growth

10

Broad-based moderation in

exports and imports

RM billion

34.8

36.9

10

15

20

25

30

35

40

1Q-17 3Q-17 1Q-18 3Q-18 1Q-19

‘11 – ’18 average: 24.1

Source: Department of Statistics, Malaysia

Going forward, exports will be

supported by

8.1

-0.7-10

0

10

20

30

1Q-17 3Q-17 1Q-18 3Q-18 1Q-19

Trade Balance

Trade balance widened as the

moderation in imports

outpaced exports

Annual change, %

Export Growth

5.7

-2.5-20

0

20

40

1Q-17 3Q-17 1Q-18 3Q-18 1Q-19

Annual change, %

Import Growth

Continued, albeit

moderate demand from

major trade partners

Global demand for

growing niche product

segments (e.g.

Automotive, medical)

Continued recovery in

commodity production

11

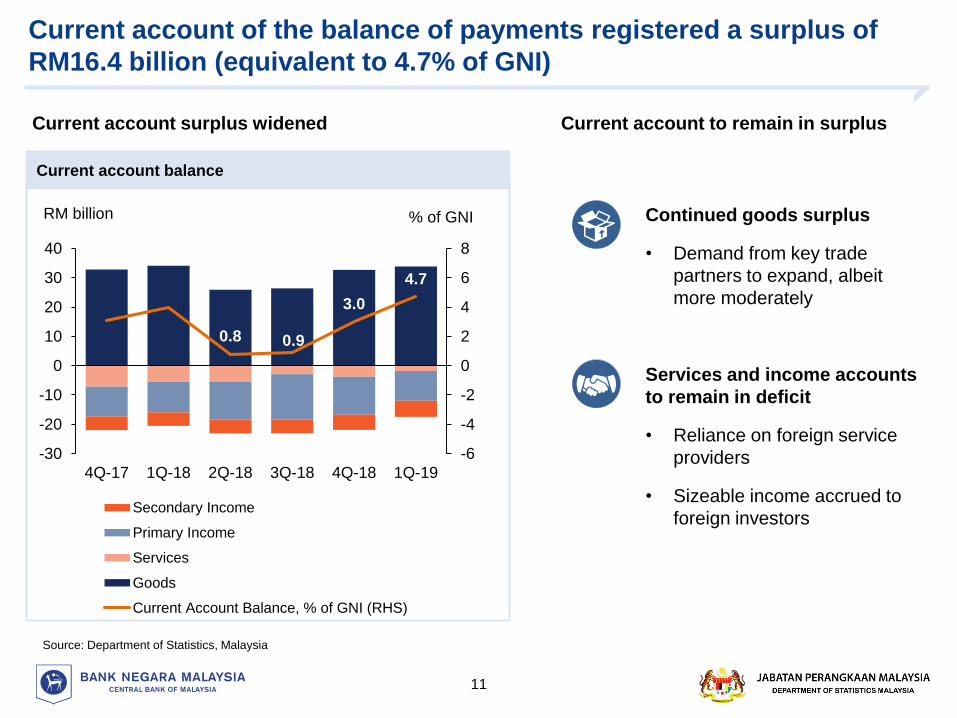

Current account of the balance of payments registered a surplus of

RM16.4 billion (equivalent to 4.7% of GNI)

0.8 0.9

3.0

4.7

-6

-4

-2

0

2

4

6

8

-30

-20

-10

0

10

20

30

40

4Q-17 1Q-18 2Q-18 3Q-18 4Q-18 1Q-19

% of GNIRM billion

Secondary Income

Primary Income

Services

Goods

Current Account Balance, % of GNI (RHS)

Current account to remain in surplus

Continued goods surplus

• Demand from key trade

partners to expand, albeit

more moderately

Services and income accounts

to remain in deficit

• Reliance on foreign service

providers

• Sizeable income accrued to

foreign investors

Source: Department of Statistics, Malaysia

Current account surplus widened

Current account balance

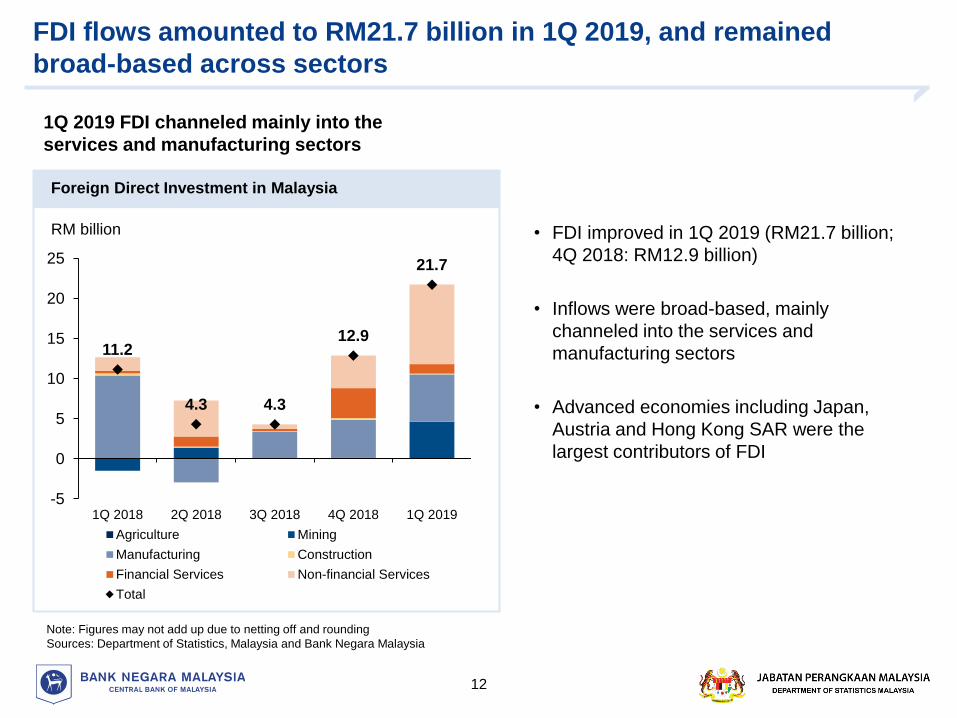

FDI flows amounted to RM21.7 billion in 1Q 2019, and remained

broad-based across sectors

12

Note: Figures may not add up due to netting off and rounding

Sources: Department of Statistics, Malaysia and Bank Negara Malaysia

• FDI improved in 1Q 2019 (RM21.7 billion;

4Q 2018: RM12.9 billion)

• Inflows were broad-based, mainly

channeled into the services and

manufacturing sectors

• Advanced economies including Japan,

Austria and Hong Kong SAR were the

largest contributors of FDI

1Q 2019 FDI channeled mainly into the

services and manufacturing sectors

Foreign Direct Investment in Malaysia

RM billion

11.2

4.3 4.3

12.9

21.7

-5

0

5

10

15

20

25

1Q 2018 2Q 2018 3Q 2018 4Q 2018 1Q 2019

Agriculture Mining

Manufacturing Construction

Financial Services Non-financial Services

Total

Monetary and Financial Developments

13

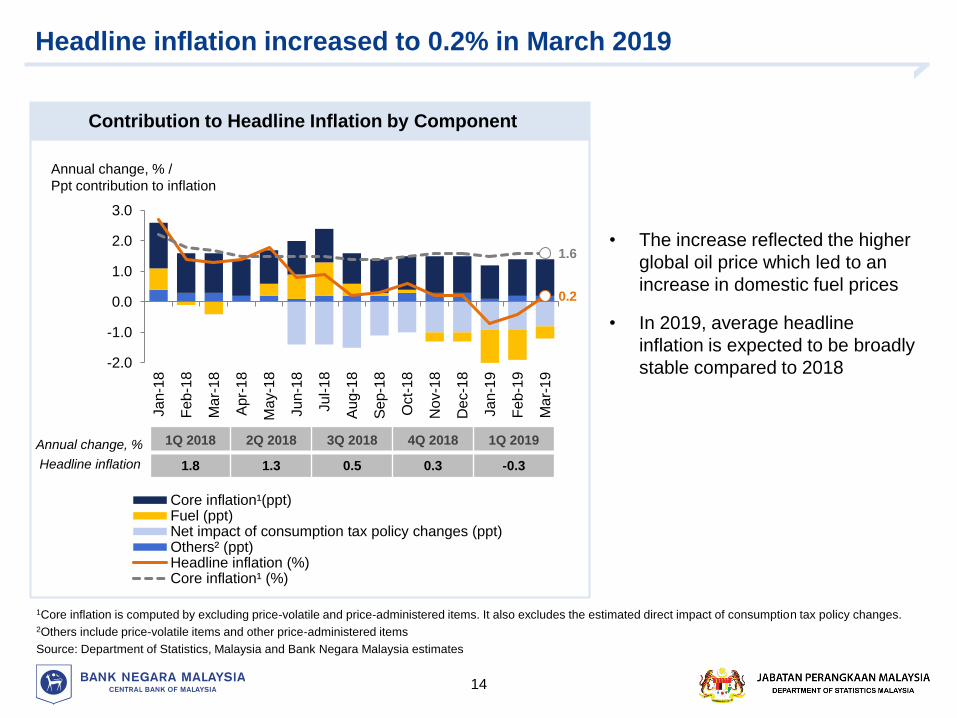

Headline inflation increased to 0.2% in March 2019

14

1Core inflation is computed by excluding price-volatile and price-administered items. It also excludes the estimated direct impact of consumption tax policy changes.2Others include price-volatile items and other price-administered items

Source: Department of Statistics, Malaysia and Bank Negara Malaysia estimates

Annual change, % /

Ppt contribution to inflation

0.2

1.6

-2.0

-1.0

0.0

1.0

2.0

3.0

Ja

n-1

8

Fe

b-1

8

Ma

r-1

8

Ap

r-1

8

Ma

y-1

8

Ju

n-1

8

Ju

l-1

8

Au

g-1

8

Se

p-1

8

Oct-

18

No

v-1

8

Dec-1

8

Ja

n-1

9

Fe

b-1

9

Ma

r-1

9

Core inflation¹(ppt)Fuel (ppt)Net impact of consumption tax policy changes (ppt)Others² (ppt)Headline inflation (%)Core inflation¹ (%)

Contribution to Headline Inflation by Component

• The increase reflected the higher

global oil price which led to an

increase in domestic fuel prices

• In 2019, average headline

inflation is expected to be broadly

stable compared to 2018

1Q 2018 2Q 2018 3Q 2018 4Q 2018 1Q 2019

1.8 1.3 0.5 0.3 -0.3Headline inflation

Annual change, %

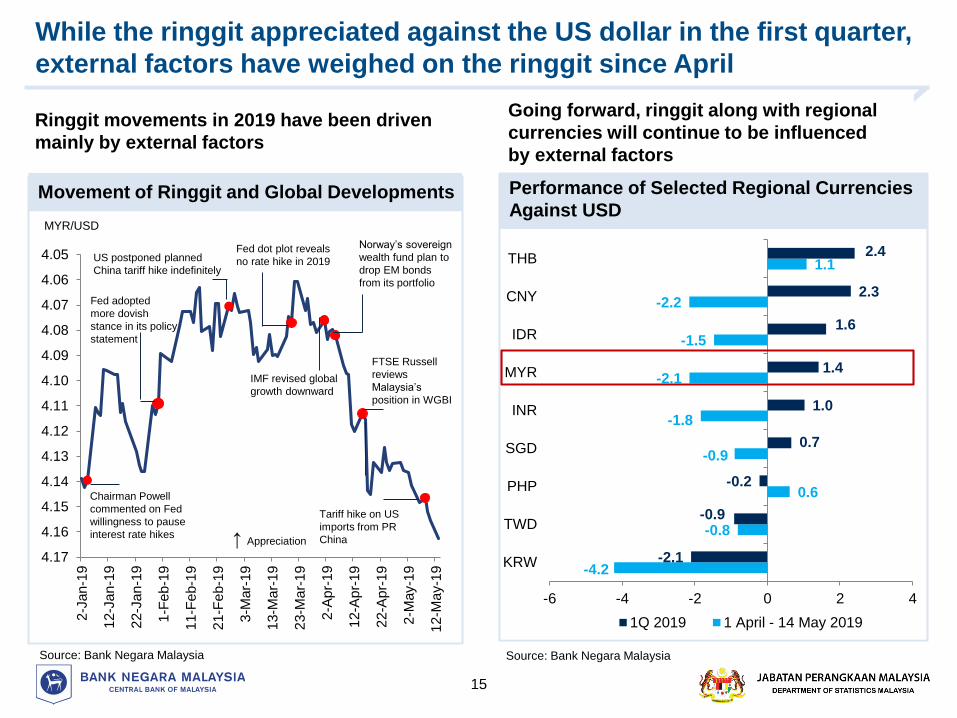

While the ringgit appreciated against the US dollar in the first quarter,

external factors have weighed on the ringgit since April

15

Ringgit movements in 2019 have been driven

mainly by external factors

4.05

4.06

4.07

4.08

4.09

4.10

4.11

4.12

4.13

4.14

4.15

4.16

4.17

2-J

an

-19

12-J

an

-19

22-J

an

-19

1-F

eb

-19

11-F

eb-1

9

21-F

eb-1

9

3-M

ar-

19

13-M

ar-

19

23-M

ar-

19

2-A

pr-

19

12-A

pr-

19

22-A

pr-

19

2-M

ay-1

9

12-M

ay-1

9

Fed adopted

more dovish

stance in its policy

statement

Fed dot plot reveals

no rate hike in 2019

FTSE Russell

reviews

Malaysia’s

position in WGBI

IMF revised global

growth downward

US postponed planned

China tariff hike indefinitely

Chairman Powell

commented on Fed

willingness to pause

interest rate hikes ↑ Appreciation

Tariff hike on US

imports from PR

China

Going forward, ringgit along with regional

currencies will continue to be influenced

by external factors

Source: Bank Negara Malaysia

Norway’s sovereign

wealth fund plan to

drop EM bonds

from its portfolio

Movement of Ringgit and Global Developments

MYR/USD

Performance of Selected Regional Currencies

Against USD

-4.2

-0.8

0.6

-0.9

-1.8

-2.1

-1.5

-2.2

1.1

-2.1

-0.9

-0.2

0.7

1.0

1.4

1.6

2.3

2.4

-6 -4 -2 0 2 4

KRW

TWD

PHP

SGD

INR

MYR

IDR

CNY

THB

1Q 2019 1 April - 14 May 2019

Source: Bank Negara Malaysia

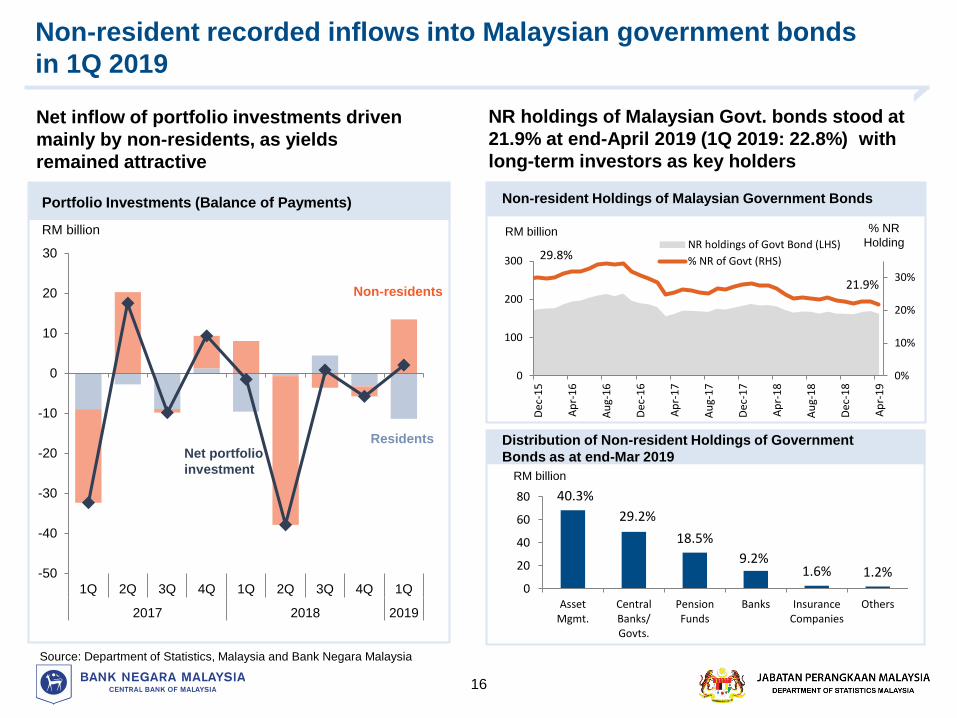

Non-resident recorded inflows into Malaysian government bonds

in 1Q 2019

16

Net inflow of portfolio investments driven

mainly by non-residents, as yields

remained attractive

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

RM billion

Residents

Non-residents

Net portfolio

investment

40.3%

29.2%

18.5%

9.2%1.6% 1.2%

0

20

40

60

80

AssetMgmt.

CentralBanks/Govts.

PensionFunds

Banks InsuranceCompanies

Others

RM billion

Portfolio Investments (Balance of Payments)

Distribution of Non-resident Holdings of Government

Bonds as at end-Mar 2019

-50

-40

-30

-20

-10

0

10

20

30

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

2017 2018 2019

NR holdings of Malaysian Govt. bonds stood at

21.9% at end-April 2019 (1Q 2019: 22.8%) with

long-term investors as key holders

21.9%

0%

10%

20%

30%

0

100

200

300

Dec

-15

Ap

r-1

6

Au

g-1

6

Dec

-16

Ap

r-1

7

Au

g-1

7

Dec

-17

Ap

r-1

8

Au

g-1

8

Dec

-18

Ap

r-1

9

NR holdings of Govt Bond (LHS)

% NR of Govt (RHS)29.8%

RM billion % NR

Holding

Non-resident Holdings of Malaysian Government Bonds

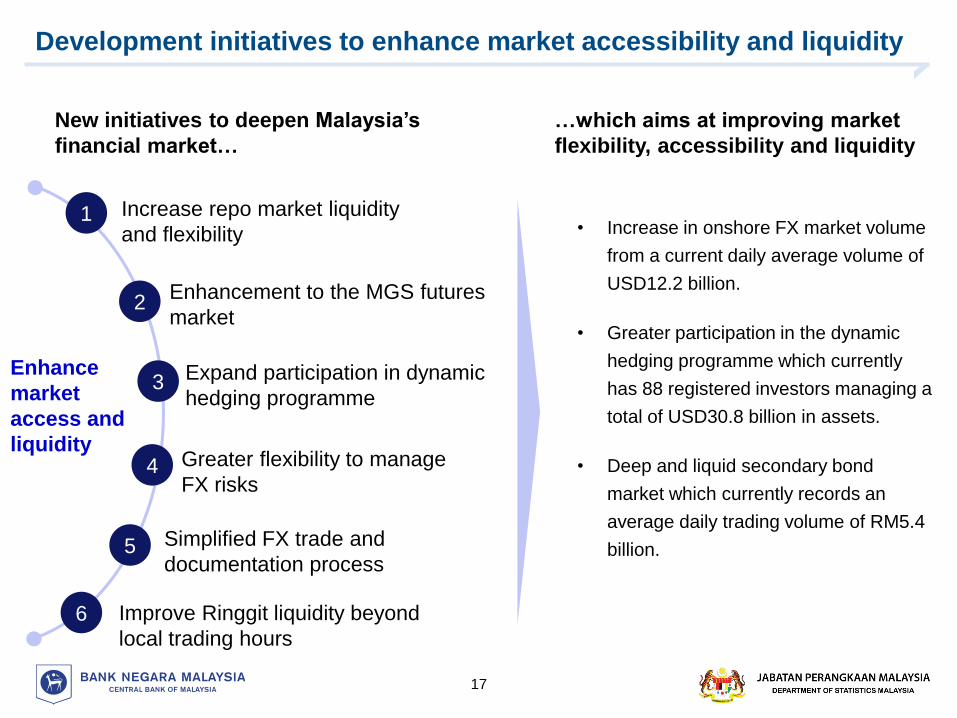

Development initiatives to enhance market accessibility and liquidity

17

Greater flexibility to manage

FX risks

Enhancement to the MGS futures

market

Expand participation in dynamic

hedging programme

Enhance

market

access and

liquidity

Increase repo market liquidity

and flexibility

Simplified FX trade and

documentation process

Improve Ringgit liquidity beyond

local trading hours

1

2

3

4

5

6

• Increase in onshore FX market volume

from a current daily average volume of

USD12.2 billion.

• Greater participation in the dynamic

hedging programme which currently

has 88 registered investors managing a

total of USD30.8 billion in assets.

• Deep and liquid secondary bond

market which currently records an

average daily trading volume of RM5.4

billion.

…which aims at improving market

flexibility, accessibility and liquidity

New initiatives to deepen Malaysia’s

financial market…

18

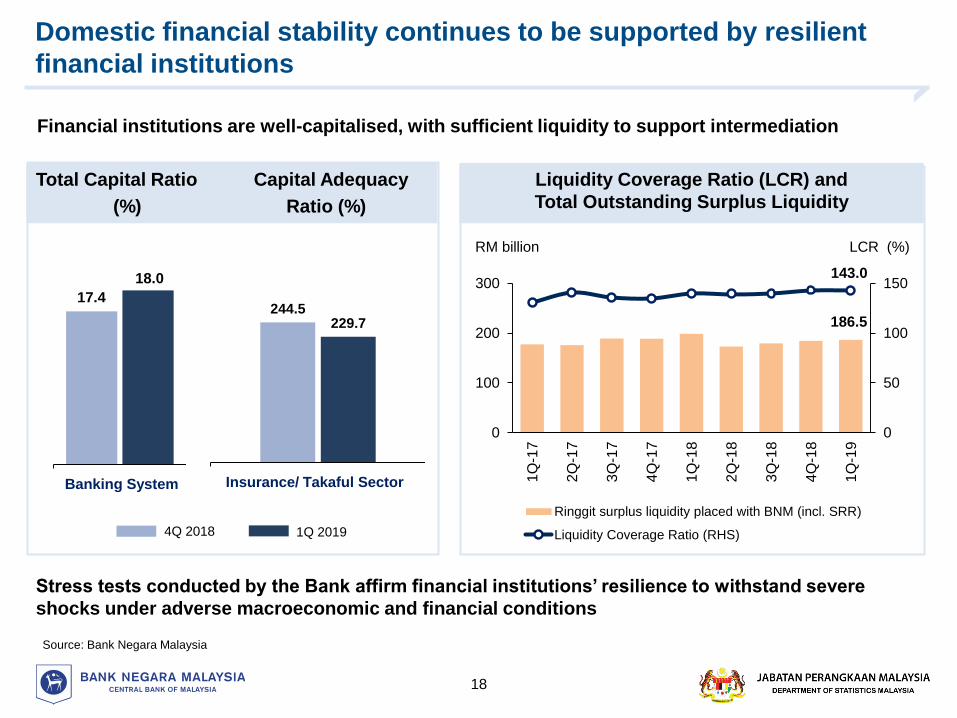

Financial institutions are well-capitalised, with sufficient liquidity to support intermediation

Stress tests conducted by the Bank affirm financial institutions’ resilience to withstand severe

shocks under adverse macroeconomic and financial conditions

Source: Bank Negara Malaysia

RM billion LCR (%)

Total Capital Ratio Capital Adequacy

(%) Ratio (%)

Liquidity Coverage Ratio (LCR) and

Total Outstanding Surplus Liquidity

Domestic financial stability continues to be supported by resilient

financial institutions

1Q 20194Q 2018

Insurance/ Takaful SectorBanking System

244.5229.7

17.4

18.0

186.5

143.0

0

50

100

150

0

100

200

300

1Q

-17

2Q

-17

3Q

-17

4Q

-17

1Q

-18

2Q

-18

3Q

-18

4Q

-18

1Q

-19

Ringgit surplus liquidity placed with BNM (incl. SRR)

Liquidity Coverage Ratio (RHS)

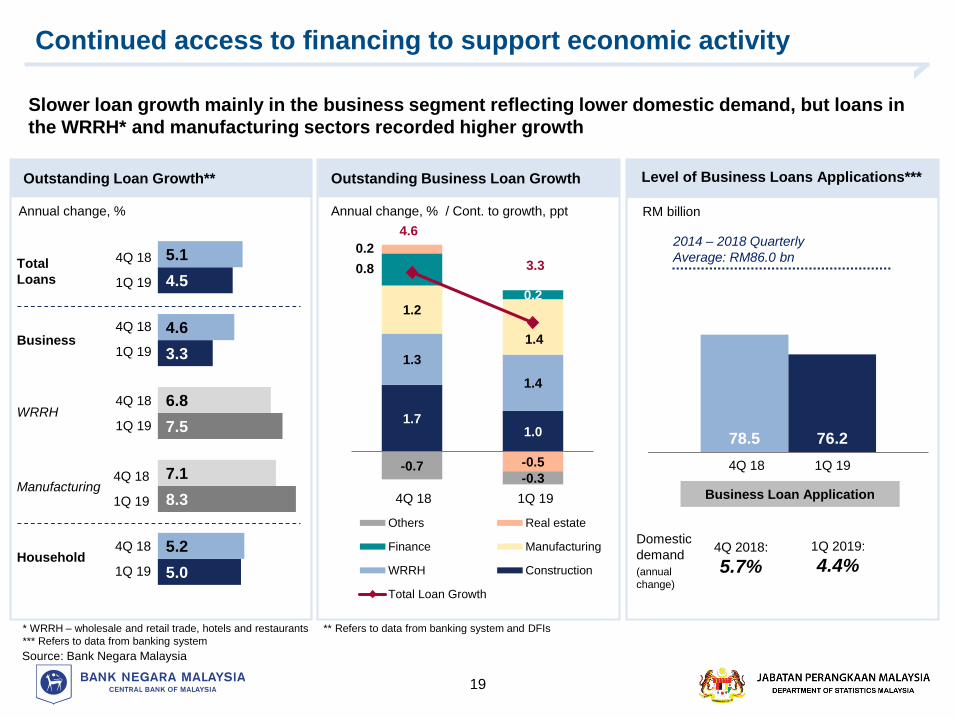

Continued access to financing to support economic activity

19

78.5 76.2

Business loan applications

Slower loan growth mainly in the business segment reflecting lower domestic demand, but loans in

the WRRH* and manufacturing sectors recorded higher growth

Annual change, % Annual change, % / Cont. to growth, ppt

5.0

8.3

7.5

3.3

4.5

5.2

7.1

6.8

4.6

5.1

1.71.0

1.3

1.4

1.2

1.4

0.8

0.2

0.2

-0.5-0.7-0.3

4.6

3.3

4Q 2018 1Q 2019

Others Real estate

Finance Manufacturing

WRRH Construction

Total Loan Growth

4Q 18 1Q 19

1Q 19

4Q 18

Business

Household

Outstanding Loan Growth** Outstanding Business Loan Growth

Source: Bank Negara Malaysia

Total

Loans

1Q 19

4Q 18

* WRRH – wholesale and retail trade, hotels and restaurants ** Refers to data from banking system and DFIs

*** Refers to data from banking system

1Q 19

4Q 18

1Q 19

4Q 18

1Q 19

4Q 18

WRRH

Manufacturing

Level of Business Loans Applications***

1Q 194Q 18

Business Loan Application

RM billion

2014 – 2018 Quarterly

Average: RM86.0 bn

Domestic

demand

(annual

change)

1Q 2019:

4.4%4Q 2018:

5.7%

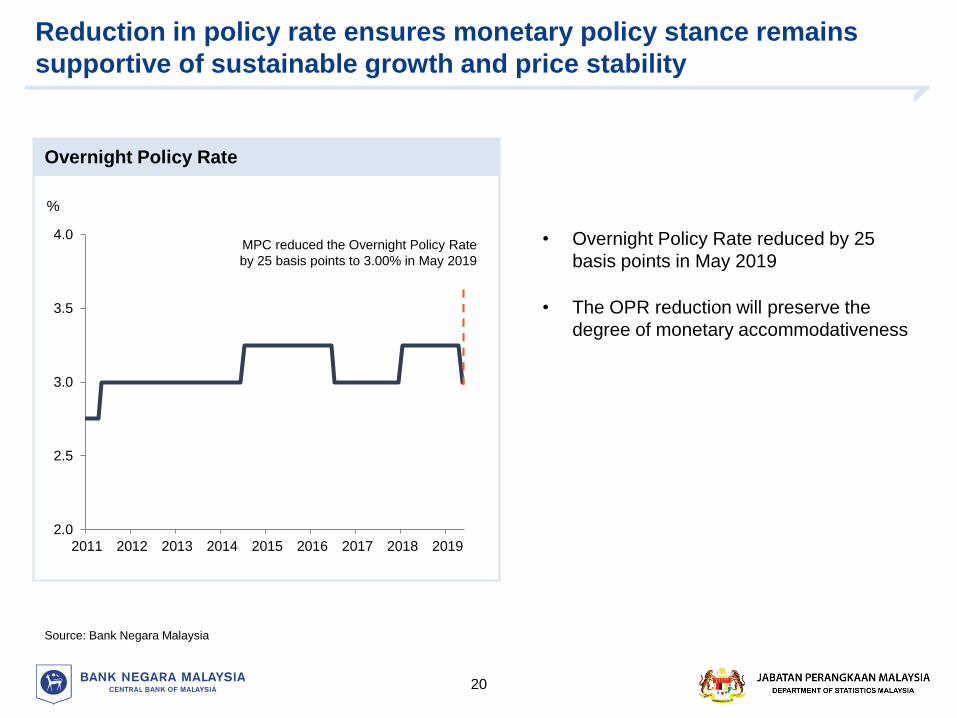

Reduction in policy rate ensures monetary policy stance remains

supportive of sustainable growth and price stability

20

• Overnight Policy Rate reduced by 25

basis points in May 2019

• The OPR reduction will preserve the

degree of monetary accommodativeness

Source: Bank Negara Malaysia

%

Overnight Policy Rate

2.0

2.5

3.0

3.5

4.0

2011 2012 2013 2014 2015 2016 2017 2018 2019

MPC reduced the Overnight Policy Rate

by 25 basis points to 3.00% in May 2019

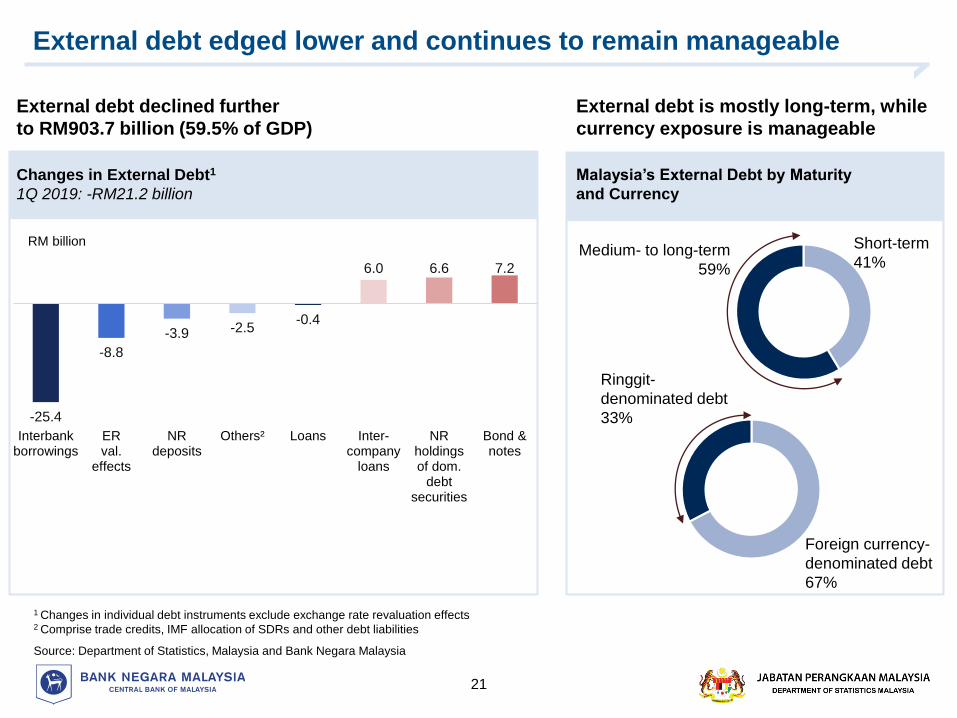

External debt edged lower and continues to remain manageable

21

1 Changes in individual debt instruments exclude exchange rate revaluation effects2 Comprise trade credits, IMF allocation of SDRs and other debt liabilities

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

External debt declined further

to RM903.7 billion (59.5% of GDP)

External debt is mostly long-term, while

currency exposure is manageable

Medium- to long-term

59%

Ringgit-

denominated debt

33%

Foreign currency-

denominated debt

67%

Changes in External Debt1

1Q 2019: -RM21.2 billion

Short-term

41%

Malaysia’s External Debt by Maturity

and Currency

-25.4

-8.8

-3.9 -2.5-0.4

6.0 6.6 7.2

Interbankborrowings

ERval.

effects

NRdeposits

Others² Loans Inter-company

loans

NRholdingsof dom.

debtsecurities

Bond ¬es

RM billion

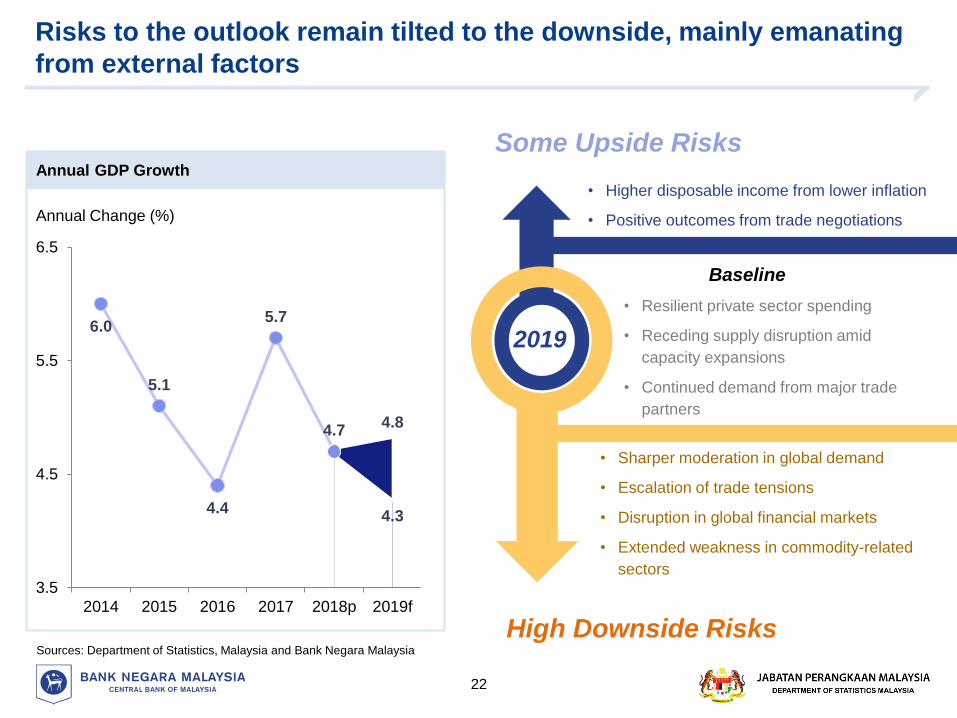

Risks to the outlook remain tilted to the downside, mainly emanating

from external factors

22

6.0

5.1

4.4

5.7

4.74.8

4.3

3.5

4.5

5.5

6.5

2014 2015 2016 2017 2018p 2019f

2019

Some Upside Risks

High Downside Risks

• Sharper moderation in global demand

• Escalation of trade tensions

• Disruption in global financial markets

• Extended weakness in commodity-related

sectors

• Resilient private sector spending

• Receding supply disruption amid

capacity expansions

• Continued demand from major trade

partners

• Higher disposable income from lower inflation

• Positive outcomes from trade negotiations

Annual GDP Growth

Annual Change (%)

Sources: Department of Statistics, Malaysia and Bank Negara Malaysia

Baseline

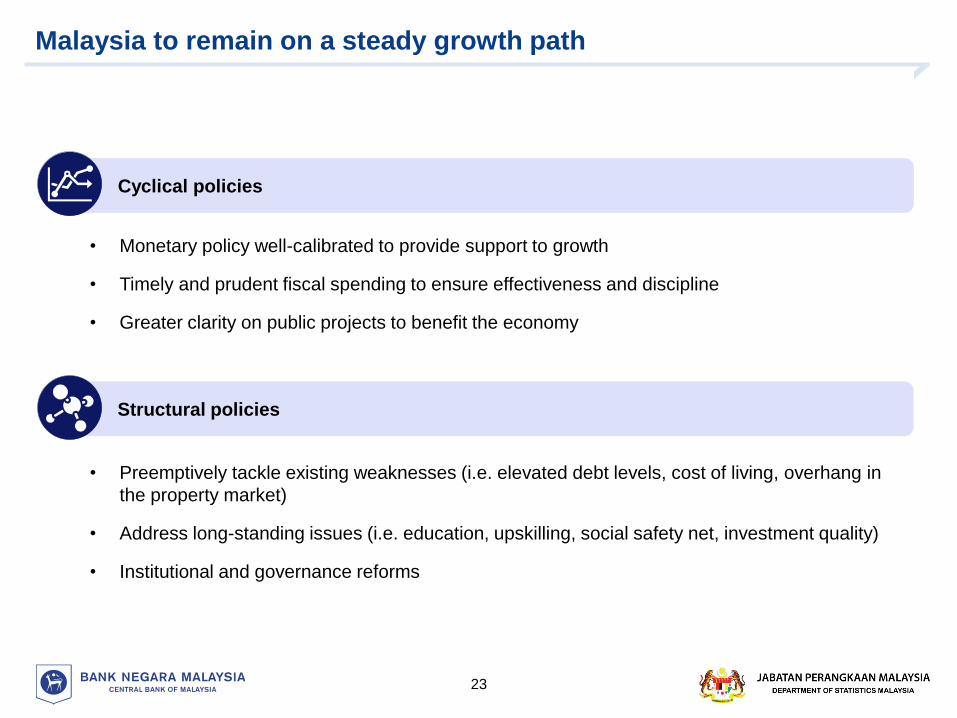

Malaysia to remain on a steady growth path

23

Cyclical policies

Structural policies

• Monetary policy well-calibrated to provide support to growth

• Timely and prudent fiscal spending to ensure effectiveness and discipline

• Greater clarity on public projects to benefit the economy

• Preemptively tackle existing weaknesses (i.e. elevated debt levels, cost of living, overhang in

the property market)

• Address long-standing issues (i.e. education, upskilling, social safety net, investment quality)

• Institutional and governance reforms

Q & A

24

Additional Information

25

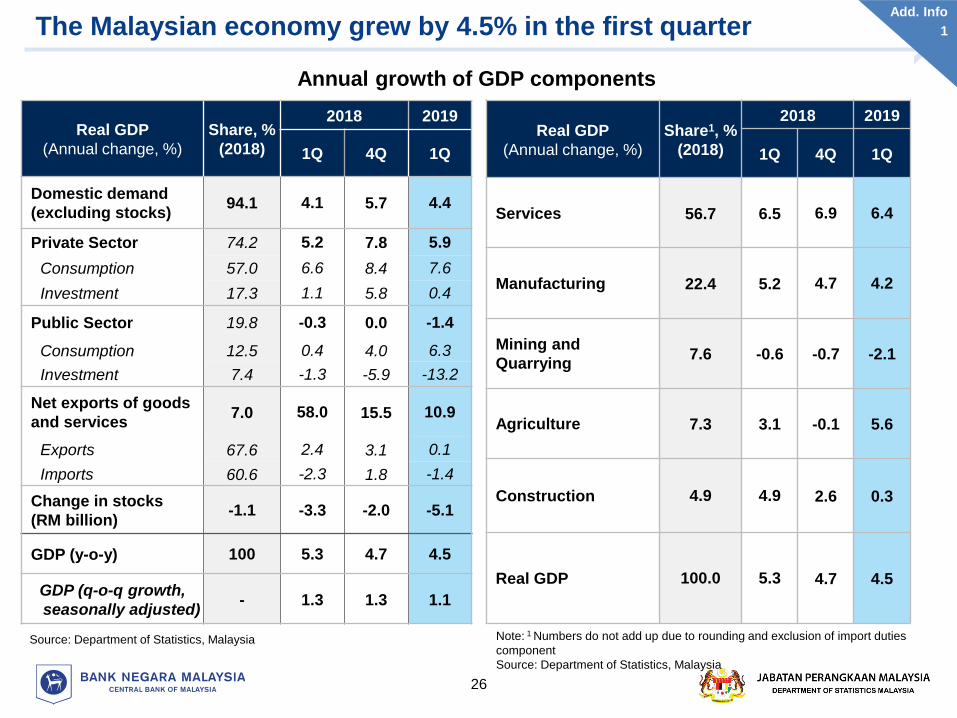

The Malaysian economy grew by 4.5% in the first quarter

26

Source: Department of Statistics, Malaysia Note: 1 Numbers do not add up due to rounding and exclusion of import duties

component

Source: Department of Statistics, Malaysia

Real GDP

(Annual change, %)

Share, %

(2018)

2018 2019

1Q 4Q 1Q

Domestic demand

(excluding stocks)94.1 4.1 5.7 4.4

Private Sector 74.2 5.2 7.8 5.9

Consumption 57.0 6.6 8.4 7.6

Investment 17.3 1.1 5.8 0.4

Public Sector 19.8 -0.3 0.0 -1.4

Consumption 12.5 0.4 4.0 6.3

Investment 7.4 -1.3 -5.9 -13.2

Net exports of goods

and services7.0 58.0 15.5 10.9

Exports 67.6 2.4 3.1 0.1

Imports 60.6 -2.3 1.8 -1.4

Change in stocks

(RM billion)-1.1 -3.3 -2.0 -5.1

GDP (y-o-y) 100 5.3 4.7 4.5

GDP (q-o-q growth,

seasonally adjusted)- 1.3 1.3 1.1

Real GDP

(Annual change, %)

Share1, %

(2018)

2018 2019

1Q 4Q 1Q

Services 56.7 6.5 6.9 6.4

Manufacturing 22.4 5.2 4.7 4.2

Mining and

Quarrying7.6 -0.6 -0.7 -2.1

Agriculture 7.3 3.1 -0.1 5.6

Construction 4.9 4.9 2.6 0.3

Real GDP 100.0 5.3 4.7 4.5

Annual growth of GDP components

Add. Info

1

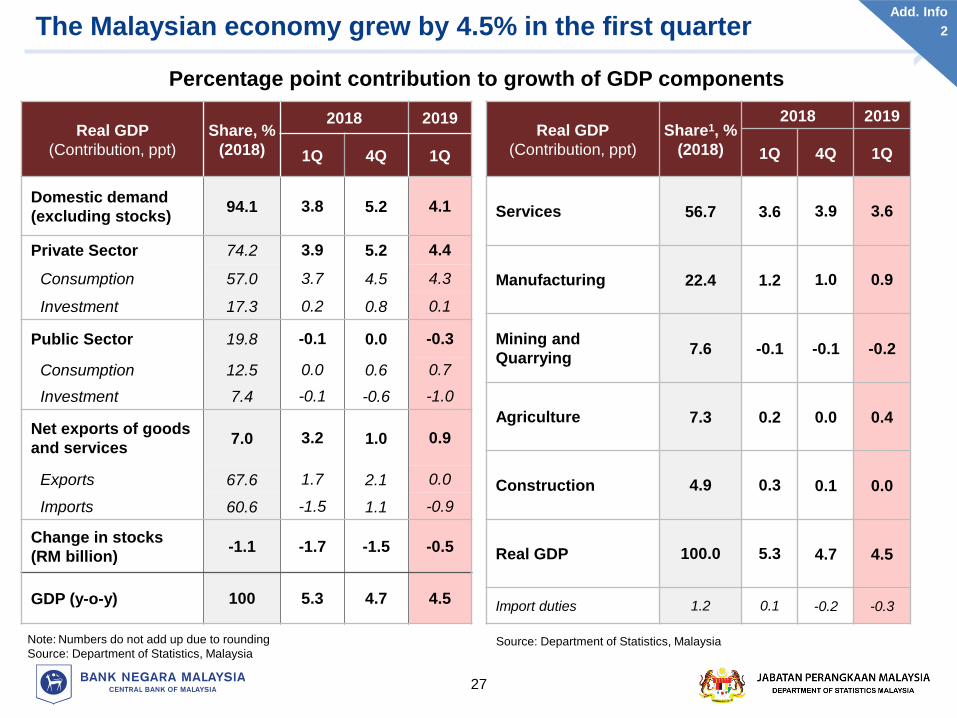

The Malaysian economy grew by 4.5% in the first quarter

27

Note: Numbers do not add up due to rounding

Source: Department of Statistics, MalaysiaSource: Department of Statistics, Malaysia

Real GDP

(Contribution, ppt)

Share, %

(2018)

2018 2019

1Q 4Q 1Q

Domestic demand

(excluding stocks)94.1 3.8 5.2 4.1

Private Sector 74.2 3.9 5.2 4.4

Consumption 57.0 3.7 4.5 4.3

Investment 17.3 0.2 0.8 0.1

Public Sector 19.8 -0.1 0.0 -0.3

Consumption 12.5 0.0 0.6 0.7

Investment 7.4 -0.1 -0.6 -1.0

Net exports of goods

and services7.0 3.2 1.0 0.9

Exports 67.6 1.7 2.1 0.0

Imports 60.6 -1.5 1.1 -0.9

Change in stocks

(RM billion)-1.1 -1.7 -1.5 -0.5

GDP (y-o-y) 100 5.3 4.7 4.5

Real GDP

(Contribution, ppt)

Share1, %

(2018)

2018 2019

1Q 4Q 1Q

Services 56.7 3.6 3.9 3.6

Manufacturing 22.4 1.2 1.0 0.9

Mining and

Quarrying7.6 -0.1 -0.1 -0.2

Agriculture 7.3 0.2 0.0 0.4

Construction 4.9 0.3 0.1 0.0

Real GDP 100.0 5.3 4.7 4.5

Import duties 1.2 0.1 -0.2 -0.3

Percentage point contribution to growth of GDP components

Add. Info

2

End