Bahasa

Halaman

Undang-undang

Malaysian Income Tax

Reporting System

(MITRS)

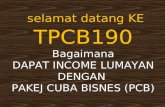

Standard antarabangsa untuk laporan

perniagaan digital bagi menggantikan

laporan berasaskan kertas

Menggunakan sistem ‘tagging’ untuk menterjemahkan

maklumat kewangan dalam bentuk/bahasa yang boleh

diproses oleh sistem supaya data tersebut boleh dibaca secara

automatik oleh mana-mana perisian XBRL

Penggunaan format XML untuk menyusun

atur maklumat perniagaan secara

elektronik

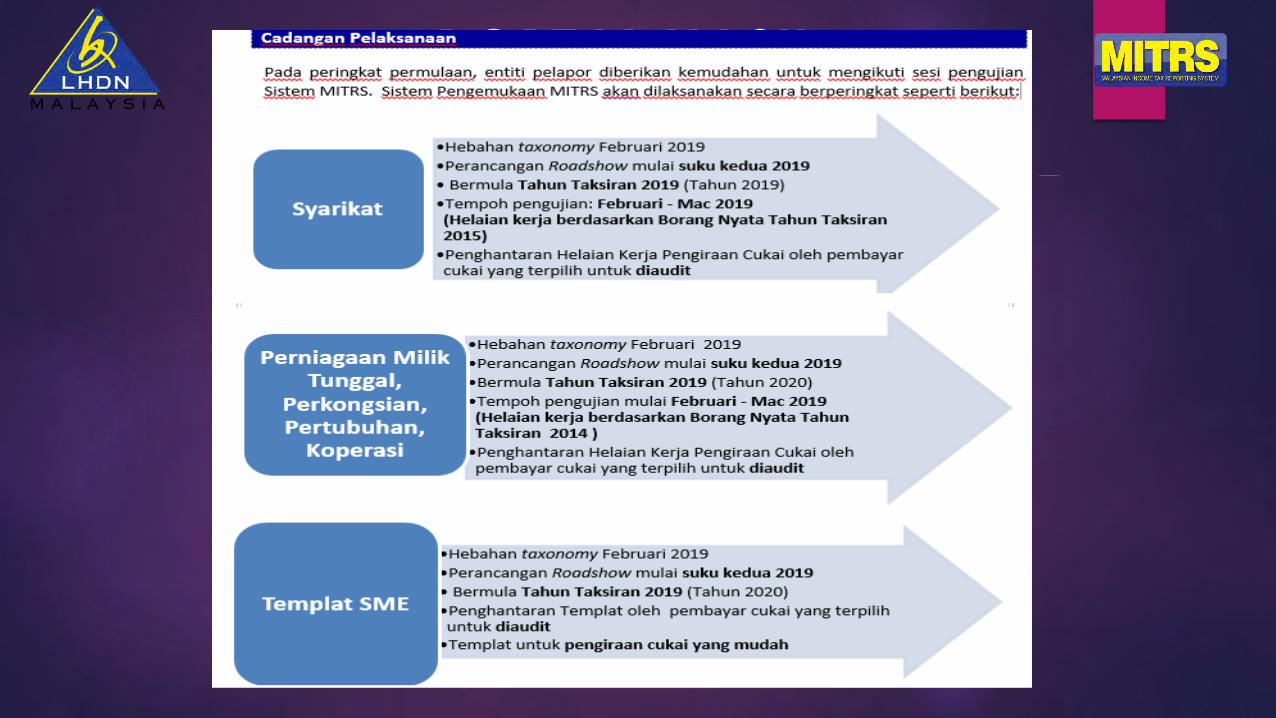

PENGENALAN

Helaian Kerja Pengiraan Cukai

[Syarikat – TT 2015

Selain Syarikat – TT2014]

SME

Templet

Penyata

Kewangan

(HK-FIC)

PENGENALAN

HK

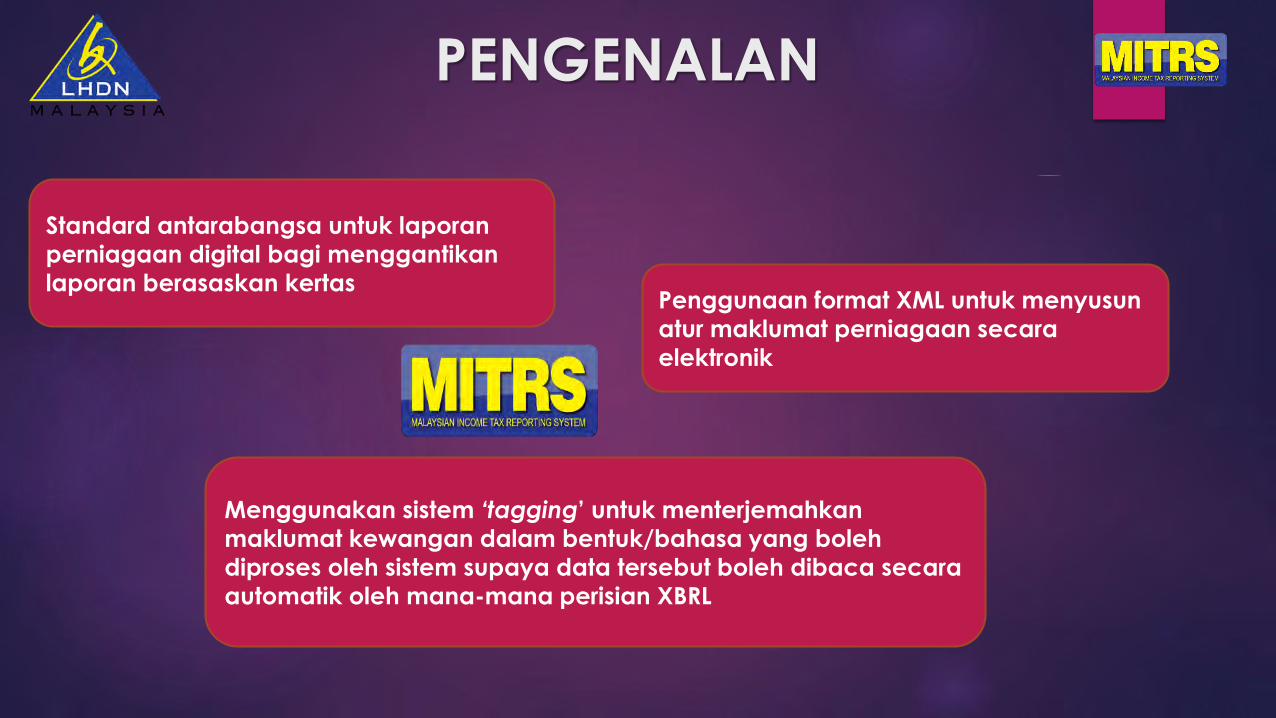

CARA PENGHANTARAN

e-Filing

• Sijil digital

• Secara dalam talian - validasi verikasi dalam talian sebelum tandatangan

• Pengesahan penerimaan (QR Code - maklumat asas pembayar cukai dan senarai helaiankerja)

• Tidak memerlukan sebarang perisian tambahan

Instance•Sijil digital – tujuan untuk log-in

•Perlu muat turun Instance yang mengandungi taxonomy LHDNM

• Isi secara off-line / export ke dalam format XBRL menggunakan perisian khas ataupun perisianperakaunan khas

•Verifikasi akan dilakukan secara off-line

•Muat naik dan tandatangan secara dalam talian untuk penghantaran

•Pengesahan penerimaan (QR Code - maklumat asas pembayar cukai dan senarai helaiankerja)

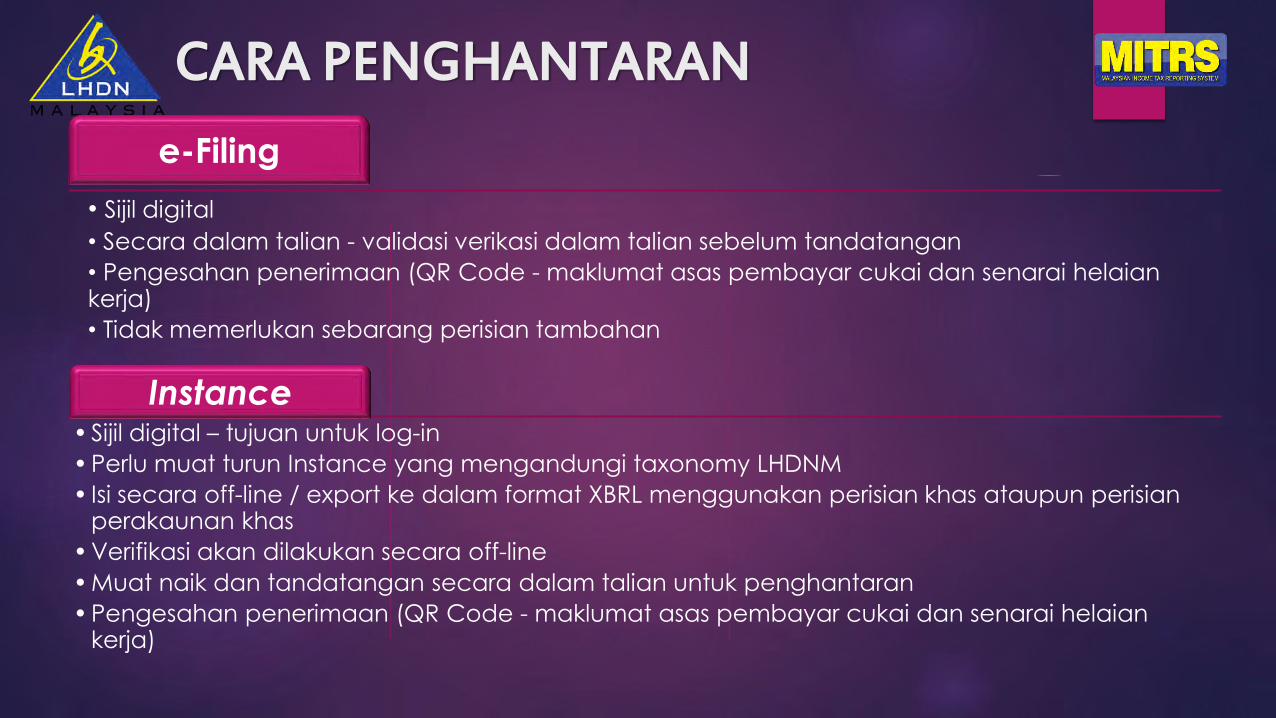

PORTAL HASIL

PORTAL HASIL

MITRS

Link MITRS :

https://taef.hasiL.gov.my ( Agen Cukai)

https://ez.hasil.gov.my ( Selain Agen Cukai)

SENARAI HELAIAN KERJA MENGIKUT

AKTIVITI PERNIAGAAN

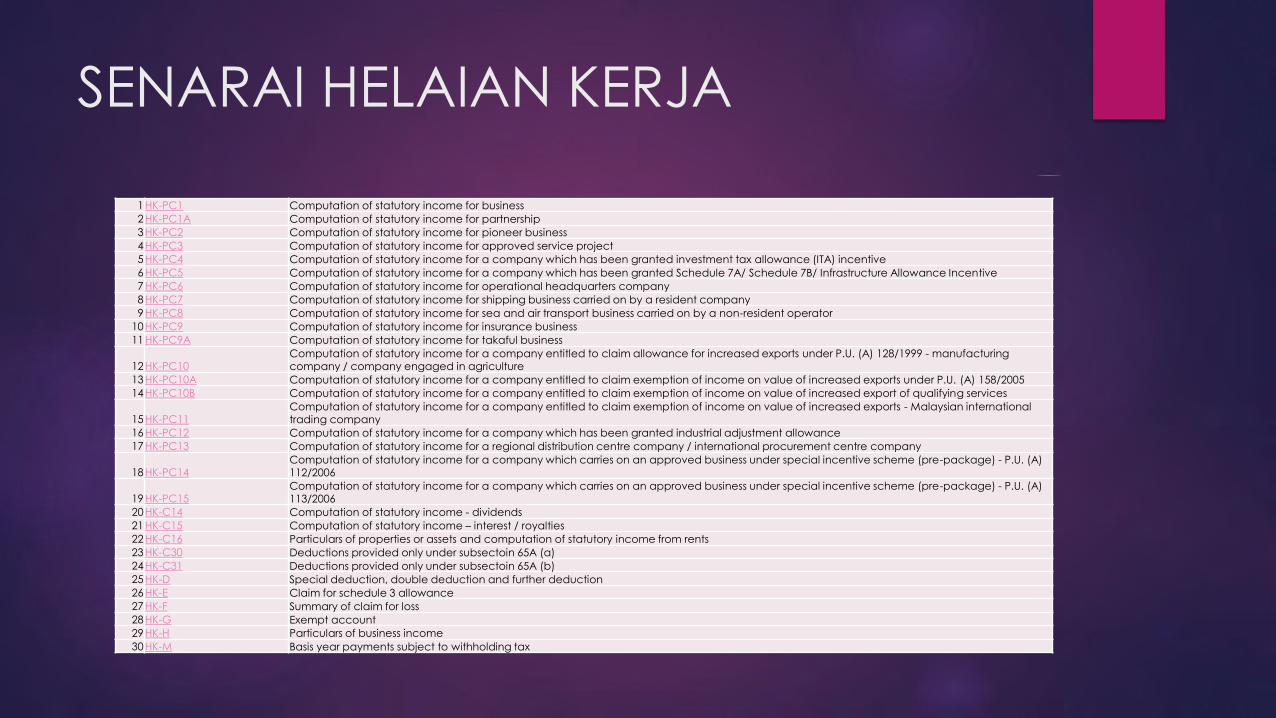

SENARAI HELAIAN KERJA

1HK-PC1 Computation of statutory income for business

2HK-PC1A Computation of statutory income for partnership

3HK-PC2 Computation of statutory income for pioneer business

4HK-PC3 Computation of statutory income for approved service project

5HK-PC4 Computation of statutory income for a company which has been granted investment tax allowance (ITA) incentive

6HK-PC5 Computation of statutory income for a company which has been granted Schedule 7A/ Schedule 7B/ Infrastructure Allowance Incentive

7HK-PC6 Computation of statutory income for operational headquarters company

8HK-PC7 Computation of statutory income for shipping business carried on by a resident company

9HK-PC8 Computation of statutory income for sea and air transport business carried on by a non-resident operator

10HK-PC9 Computation of statutory income for insurance business

11HK-PC9A Computation of statutory income for takaful business

12HK-PC10Computation of statutory income for a company entitled to claim allowance for increased exports under P.U. (A) 128/1999 - manufacturing company / company engaged in agriculture

13HK-PC10A Computation of statutory income for a company entitled to claim exemption of income on value of increased exports under P.U. (A) 158/2005

14HK-PC10B Computation of statutory income for a company entitled to claim exemption of income on value of increased export of qualifying services

15HK-PC11Computation of statutory income for a company entitled to claim exemption of income on value of increased exports - Malaysian international trading company

16HK-PC12 Computation of statutory income for a company which has been granted industrial adjustment allowance

17HK-PC13 Computation of statutory income for a regional distribution centre company / international procurement centre company

18HK-PC14Computation of statutory income for a company which carries on an approved business under special incentive scheme (pre-package) - P.U. (A) 112/2006

19HK-PC15Computation of statutory income for a company which carries on an approved business under special incentive scheme (pre-package) - P.U. (A) 113/2006

20HK-C14 Computation of statutory income - dividends

21HK-C15 Computation of statutory income – interest / royalties

22HK-C16 Particulars of properties or assets and computation of statutory income from rents

23HK-C30 Deductions provided only under subsectoin 65A (a)

24HK-C31 Deductions provided only under subsectoin 65A (b)

25HK-D Special deduction, double deduction and further deduction

26HK-E Claim for schedule 3 allowance

27HK-F Summary of claim for loss

28HK-G Exempt account

29HK-H Particulars of business income

30HK-M Basis year payments subject to withholding tax

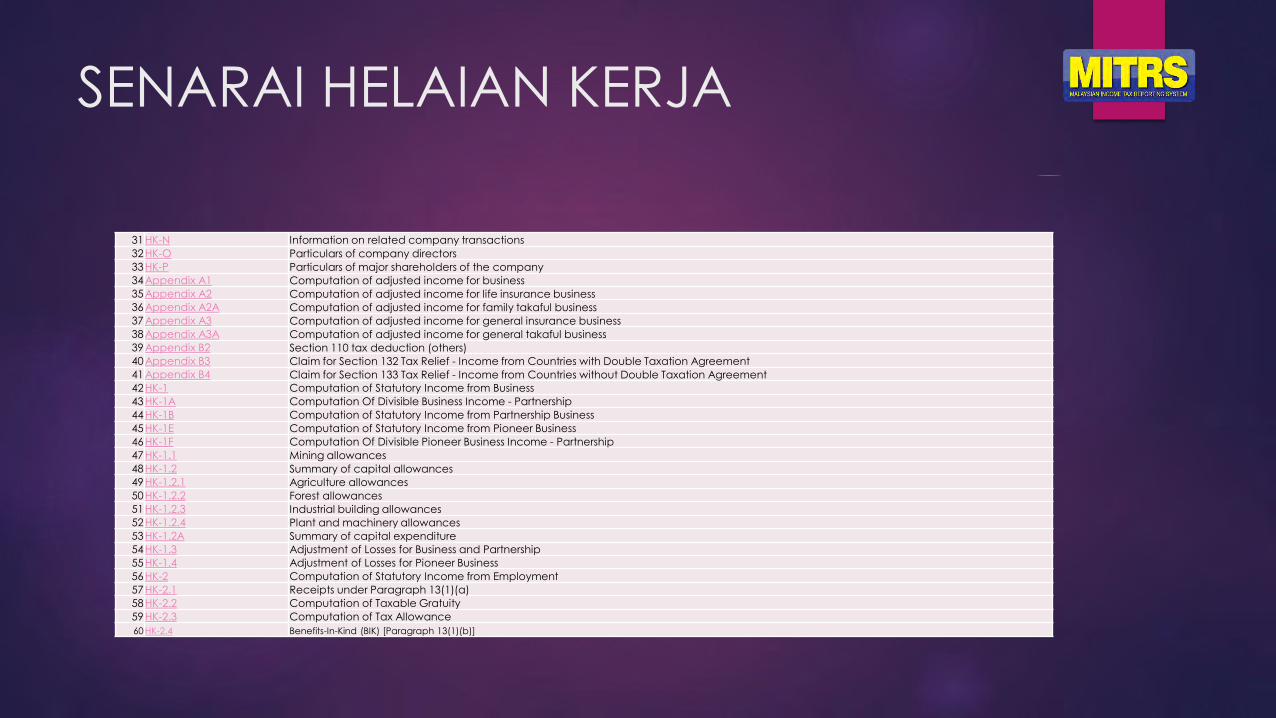

SENARAI HELAIAN KERJA

31HK-N Information on related company transactions

32HK-O Particulars of company directors

33HK-P Particulars of major shareholders of the company

34Appendix A1 Computation of adjusted income for business

35Appendix A2 Computation of adjusted income for life insurance business

36Appendix A2A Computation of adjusted income for family takaful business

37Appendix A3 Computation of adjusted income for general insurance business

38Appendix A3A Computation of adjusted income for general takaful business

39Appendix B2 Section 110 tax deduction (others)

40Appendix B3 Claim for Section 132 Tax Relief - Income from Countries with Double Taxation Agreement

41Appendix B4 Claim for Section 133 Tax Relief - Income from Countries without Double Taxation Agreement

42HK-1 Computation of Statutory Income from Business

43HK-1A Computation Of Divisible Business Income - Partnership

44HK-1B Computation of Statutory Income from Partnership Business

45HK-1E Computation of Statutory Income from Pioneer Business

46HK-1F Computation Of Divisible Pioneer Business Income - Partnership

47HK-1.1 Mining allowances

48HK-1.2 Summary of capital allowances

49HK-1.2.1 Agriculture allowances

50HK-1.2.2 Forest allowances

51HK-1.2.3 Industrial building allowances

52HK-1.2.4 Plant and machinery allowances

53HK-1.2A Summary of capital expenditure

54HK-1.3 Adjustment of Losses for Business and Partnership

55HK-1.4 Adjustment of Losses for Pioneer Business

56HK-2 Computation of Statutory Income from Employment

57HK-2.1 Receipts under Paragraph 13(1)(a)

58HK-2.2 Computation of Taxable Gratuity

59HK-2.3 Computation of Tax Allowance

60 HK-2.4 Benefits-In-Kind (BIK) [Paragraph 13(1)(b)]

SENARAI HELAIAN KERJA

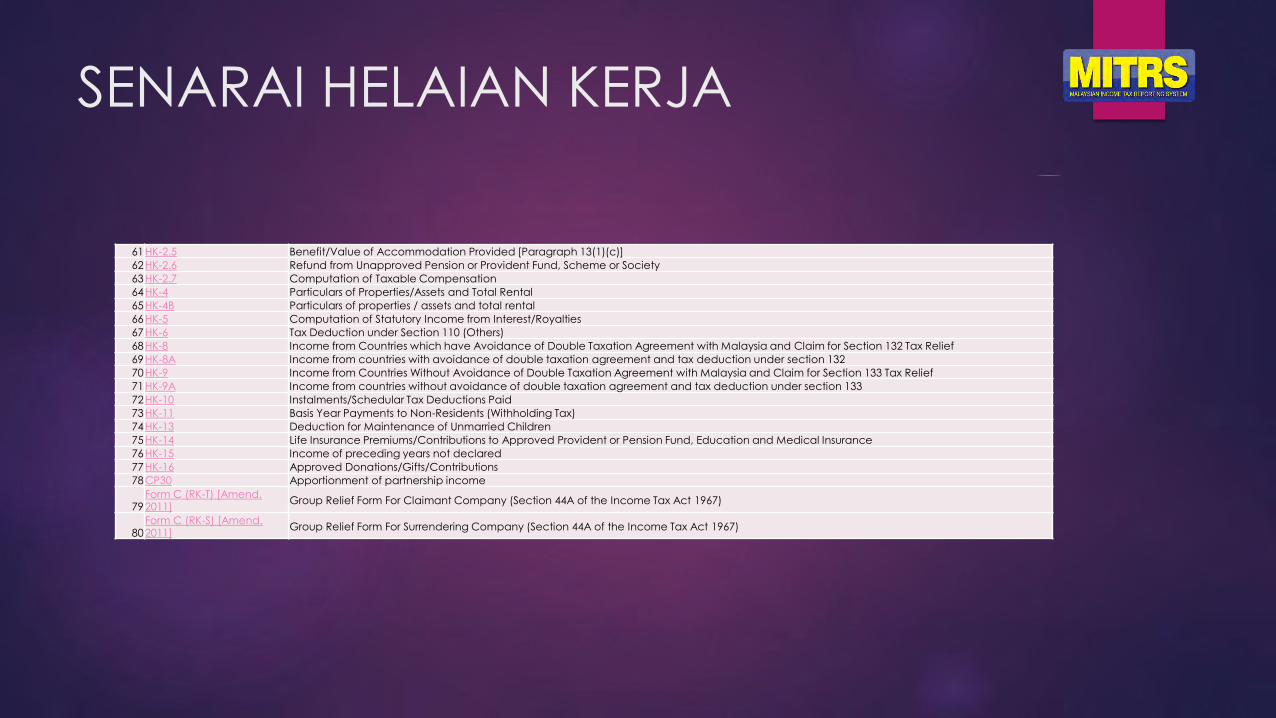

61HK-2.5 Benefit/Value of Accommodation Provided [Paragraph 13(1)(c)]

62HK-2.6 Refund from Unapproved Pension or Provident Fund, Scheme or Society

63HK-2.7 Computation of Taxable Compensation

64HK-4 Particulars of Properties/Assets and Total Rental

65HK-4B Particulars of properties / assets and total rental

66HK-5 Computation of Statutory Income from Interest/Royalties

67HK-6 Tax Deduction under Section 110 (Others)

68HK-8 Income from Countries which have Avoidance of Double Taxation Agreement with Malaysia and Claim for Section 132 Tax Relief

69HK-8A Income from countries with avoidance of double taxation agreement and tax deduction under section 132

70HK-9 Income from Countries Without Avoidance of Double Taxation Agreement with Malaysia and Claim for Section 133 Tax Relief

71HK-9A Income from countries without avoidance of double taxation agreement and tax deduction under section 133

72HK-10 Instalments/Schedular Tax Deductions Paid

73HK-11 Basis Year Payments to Non-Residents (Withholding Tax)

74HK-13 Deduction for Maintenance of Unmarried Children

75HK-14 Life Insurance Premiums/Contributions to Approved Provident or Pension Fund, Education and Medical Insurance

76HK-15 Income of preceding years not declared

77HK-16 Approved Donations/Gifts/Contributions

78CP30 Apportionment of partnership income

79Form C (RK-T) [Amend. 2011]

Group Relief Form For Claimant Company (Section 44A of the Income Tax Act 1967)

80Form C (RK-S) [Amend. 2011]

Group Relief Form For Surrendering Company (Section 44A of the Income Tax Act 1967)

SENARAI HELAIAN KERJA

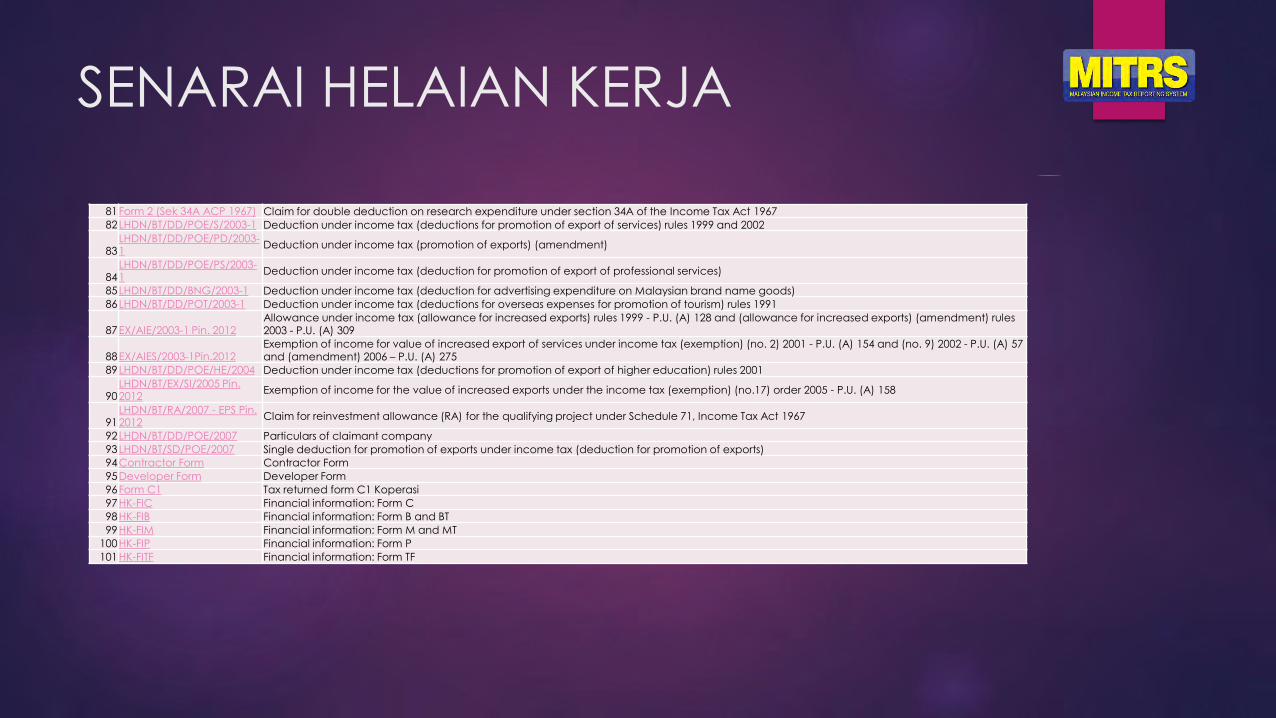

81Form 2 (Sek 34A ACP 1967) Claim for double deduction on research expenditure under section 34A of the Income Tax Act 1967

82LHDN/BT/DD/POE/S/2003-1 Deduction under income tax (deductions for promotion of export of services) rules 1999 and 2002

83LHDN/BT/DD/POE/PD/2003-1

Deduction under income tax (promotion of exports) (amendment)

84LHDN/BT/DD/POE/PS/2003-1

Deduction under income tax (deduction for promotion of export of professional services)

85LHDN/BT/DD/BNG/2003-1 Deduction under income tax (deduction for advertising expenditure on Malaysian brand name goods)

86LHDN/BT/DD/POT/2003-1 Deduction under income tax (deductions for overseas expenses for promotion of tourism) rules 1991

87EX/AIE/2003-1 Pin. 2012Allowance under income tax (allowance for increased exports) rules 1999 - P.U. (A) 128 and (allowance for increased exports) (amendment) rules 2003 - P.U. (A) 309

88EX/AIES/2003-1Pin.2012Exemption of income for value of increased export of services under income tax (exemption) (no. 2) 2001 - P.U. (A) 154 and (no. 9) 2002 - P.U. (A) 57 and (amendment) 2006 – P.U. (A) 275

89LHDN/BT/DD/POE/HE/2004 Deduction under income tax (deductions for promotion of export of higher education) rules 2001

90LHDN/BT/EX/SI/2005 Pin. 2012

Exemption of income for the value of increased exports under the income tax (exemption) (no.17) order 2005 - P.U. (A) 158

91LHDN/BT/RA/2007 - EPS Pin. 2012

Claim for reinvestment allowance (RA) for the qualifying project under Schedule 71, Income Tax Act 1967

92LHDN/BT/DD/POE/2007 Particulars of claimant company

93LHDN/BT/SD/POE/2007 Single deduction for promotion of exports under income tax (deduction for promotion of exports)

94Contractor Form Contractor Form

95Developer Form Developer Form

96Form C1 Tax returned form C1 Koperasi

97HK-FIC Financial information: Form C

98HK-FIB Financial information: Form B and BT

99HK-FIM Financial information: Form M and MT

100HK-FIP Financial information: Form P

101HK-FITF Financial information: Form TF

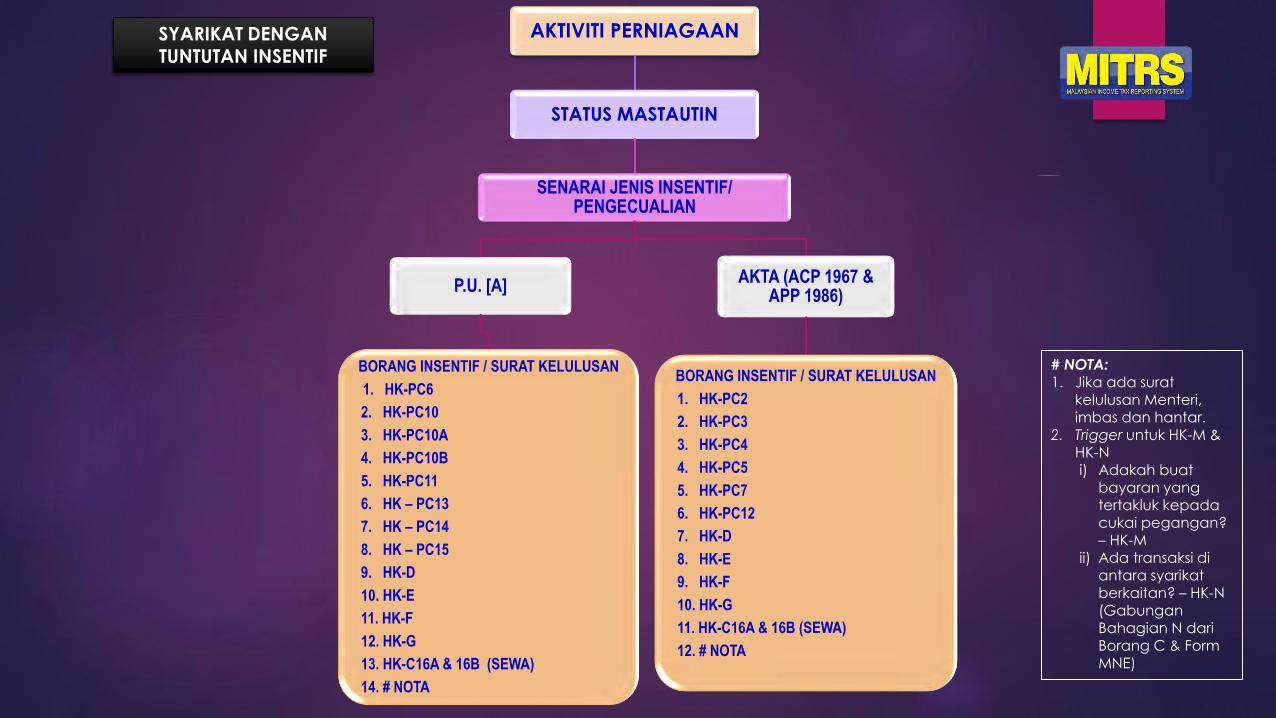

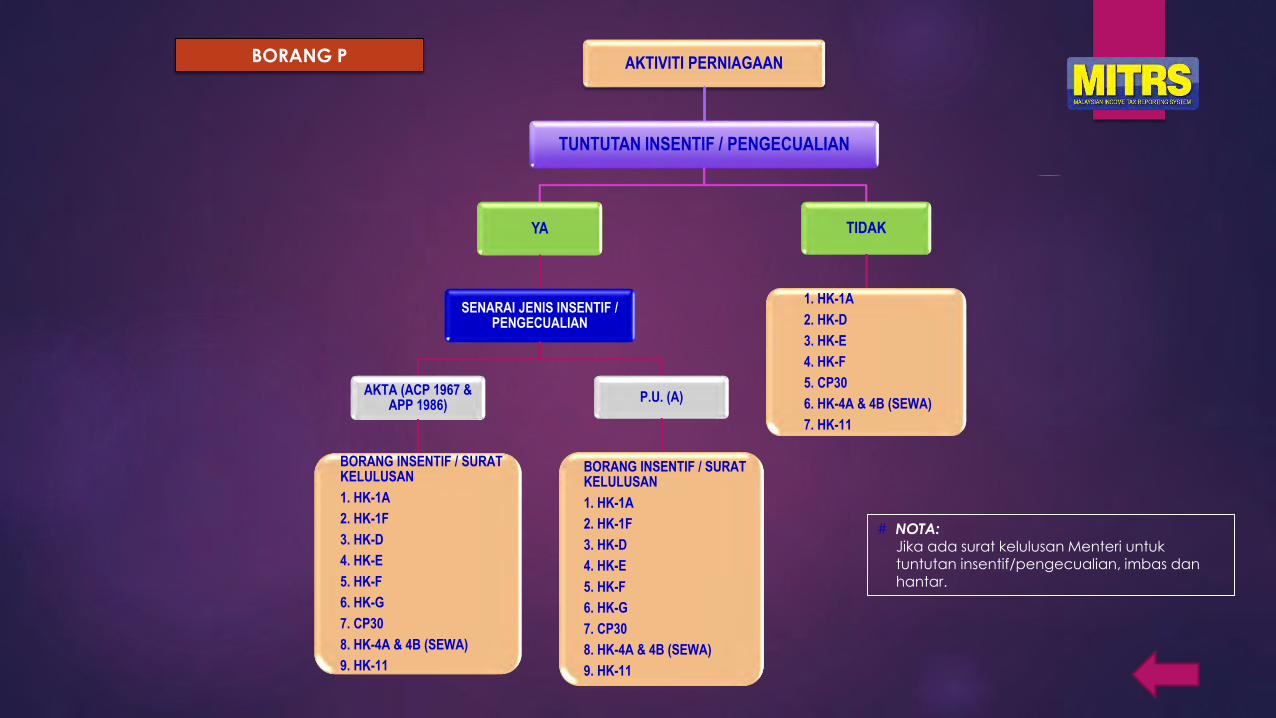

AKTIVITI PERNIAGAAN

STATUS MASTAUTIN

TUNTUTAN INSENTIF / PENGECUALIAN

YA

SENARAI JENIS INSENTIF/ PENGECUALIAN

P.U. [A]

BORANG INSENTIF / SURAT KELULUSAN

1. HK-PC6

2. HK-PC10

3. HK-PC10A

4. HK-PC10B

5. HK-PC11

6. HK – PC13

7. HK – PC14

8. HK – PC15

9. HK-D

10. HK-E

11. HK-F

12. HK-G

13. HK-C16A & 16B (SEWA)

14. # NOTA

AKTA (ACP 1967 & APP 1986)

BORANG INSENTIF / SURAT

KELULUSAN

1. HK-PC2

2. HK-PC3

3. HK-PC4

4. HK-PC5

5. HK-PC7

6. HK-PC12

7. HK-D

8. HK-E

9. HK-F

10. HK-G

11. HK-C16A & 16B (SEWA)

12. # NOTA

TIDAK

KONTRAKTOR

1. LAMPIRAN A1

2. HK-PC1

3. HK-D

4. HK-E

5. HK-F

6. HK-C16A & 16B (SEWA)

7. JADUAL PROJEK

8. # NOTA

PEMAJU

1. LAMPIRAN A1

2. HK-PC1

3. HK-D

4. HK-E

5. HK-F

6. HK-C16A & 16B (SEWA)

7. JADUAL PROJEK

8. # NOTA

PERKAPALAN

1. LAMPIRAN A1

2. HK-PC1

3. HK-PC7

4. HK-PC8

5. HK-D

6. HK-E

7. HK-F

8. HK-C16A & 16B (SEWA)

9. # NOTA

PERKILANGAN & PERDAGANGAN

1. LAMPIRAN A1

2. HK-PC1

3. HK-D

4. HK-E

5. HK-F

6. HK-C16A & 16B (SEWA)

7. # NOTA

INSURANS

1. LAMPIRAN A2 & A3

2. HK-PC9

3. HK-D

4. HK-E

5. HK-F

6. HK-C16A & 16B (SEWA)

7. # NOTA

TAKAFUL

1. LAMPIRAN A2 & A3A

2. LAMPIRAN A4

3. HK-PC9A

4. HK-C16A & 16B (SEWA)

5. # NOTA

UMUM

1. LAMPIRAN A1

2. HK-PC1

3. HK-D

4. HK-E

5. HK-F

6. HK-C16A & 16B (SEWA)

7. # NOTA

# NOTA:1. Jika ada surat kelulusan Menteri, imbas dan hantar.2. Trigger untuk HK-M & HK-N

i) Adakah buat bayaran yang tertakluk kepada cukai pegangan? – HK-M ii) Ada transaksi di antara syarikat berkaitan? – HK-N (Gabungan Bahagian N dari Borang C & Form MNE)

SYARIKAT

AKTIVITI PERNIAGAAN

STATUS MASTAUTIN

SENARAI JENIS INSENTIF/ PENGECUALIAN

P.U. [A]

BORANG INSENTIF / SURAT KELULUSAN

1. HK-PC6

2. HK-PC10

3. HK-PC10A

4. HK-PC10B

5. HK-PC11

6. HK – PC13

7. HK – PC14

8. HK – PC15

9. HK-D

10. HK-E

11. HK-F

12. HK-G

13. HK-C16A & 16B (SEWA)

14. # NOTA

AKTA (ACP 1967 & APP 1986)

BORANG INSENTIF / SURAT KELULUSAN

1. HK-PC2

2. HK-PC3

3. HK-PC4

4. HK-PC5

5. HK-PC7

6. HK-PC12

7. HK-D

8. HK-E

9. HK-F

10. HK-G

11. HK-C16A & 16B (SEWA)

12. # NOTA

# NOTA:1. Jika ada surat

kelulusan Menteri, imbas dan hantar.

2. Trigger untuk HK-M & HK-N i) Adakah buat

bayaran yang tertakluk kepadacukai pegangan? – HK-M

ii) Ada transaksi di antara syarikatberkaitan? – HK-N (GabunganBahagian N dariBorang C & Form MNE)

SYARIKAT DENGAN TUNTUTAN INSENTIF

AKTIVITI PERNIAGAAN

STATUS MASTAUTIN

KONTRAKTOR

1. LAMP IRAN A1

2. HK-PC1

3. HK-D

4. HK-E

5. HK-F

6. HK-C16A & 16B (SEWA)

7. JADUAL PROJEK

8. # NOTA

PEMAJU

1. LAMPIRAN A1

2. HK-PC1

3. HK-D

4. HK-E

5. HK-F

6. HK-C16A & 16B (SEWA)

7. JADUAL PROJEK

8. # NOTA

PERKAPALAN

1. LAMPIRAN A1

2. HK-PC1

3. HK-PC7

4. HK-PC8

5. HK-D

6. HK-E

7. HK-F

8. HK-C16A & 16B (SEWA)

9. # NOTA

PERKILANGAN & PERDAGANGAN

1. LAMPIRAN A1

2. HK-PC1

3. HK-D

4. HK-E

5. HK-F

6. HK-C16A & 16B (SEWA)

7. # NOTA

INSURANS

1. LAMPIRAN A2 & A3

2. HK-PC9

3. HK-D

4. HK-E

5. HK-F

6. HK-C16A & 16B (SEWA)

7. # NOTA

TAKAFUL

1. LAMPIRAN A2 & A3A

2. LAMPIRAN A4

3. HK-PC9A

4. HK-C16A & 16B (SEWA)

5. # NOTA

LAIN-LAIN

1. LAMPIRAN A1

2. HK-PC1

3. HK-D

4. HK-E

5. HK-F

6. HK-C16A & 16B (SEWA)

7. # NOTA

# NOTA:1. Jika ada surat kelulusan Menteri, imbas dan hantar.2. Trigger untuk HK-M & HK-N

i) Adakah buat bayaran yang tertakluk kepada cukai pegangan? – HK-M ii) Ada transaksi di antara syarikat berkaitan? – HK-N (Gabungan Bahagian N dari Borang C & Form MNE)

SYARIKAT TIDAK MENUNTUT INSENTIF

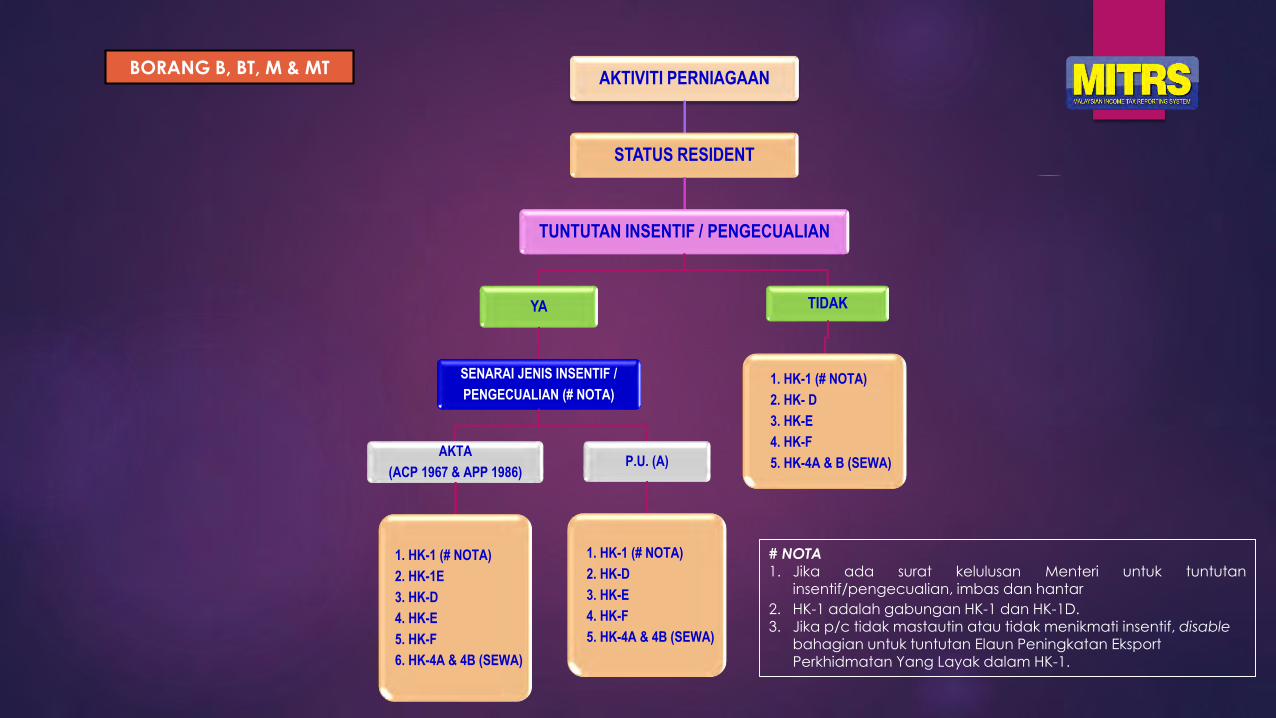

AKTIVITI PERNIAGAAN

STATUS RESIDENT

TUNTUTAN INSENTIF / PENGECUALIAN

YA

SENARAI JENIS INSENTIF /

PENGECUALIAN (# NOTA)

AKTA

(ACP 1967 & APP 1986)

1. HK-1 (# NOTA)

2. HK-1E

3. HK-D

4. HK-E

5. HK-F

6. HK-4A & 4B (SEWA)

P.U. (A)

1. HK-1 (# NOTA)

2. HK-D

3. HK-E

4. HK-F

5. HK-4A & 4B (SEWA)

TIDAK

1. HK-1 (# NOTA)

2. HK- D

3. HK-E

4. HK-F

5. HK-4A & B (SEWA)

BORANG B, BT, M & MT

# NOTA

1. Jika ada surat kelulusan Menteri untuk tuntutaninsentif/pengecualian, imbas dan hantar

2. HK-1 adalah gabungan HK-1 dan HK-1D. 3. Jika p/c tidak mastautin atau tidak menikmati insentif, disable

bahagian untuk tuntutan Elaun Peningkatan EksportPerkhidmatan Yang Layak dalam HK-1.

AKTIVITI PERNIAGAAN

TUNTUTAN INSENTIF / PENGECUALIAN

YA

SENARAI JENIS INSENTIF / PENGECUALIAN

AKTA (ACP 1967 & APP 1986)

BORANG INSENTIF / SURAT KELULUSAN

1. HK-1A

2. HK-1F

3. HK-D

4. HK-E

5. HK-F

6. HK-G

7. CP30

8. HK-4A & 4B (SEWA)

9. HK-11

P.U. (A)

BORANG INSENTIF / SURAT KELULUSAN

1. HK-1A

2. HK-1F

3. HK-D

4. HK-E

5. HK-F

6. HK-G

7. CP30

8. HK-4A & 4B (SEWA)

9. HK-11

TIDAK

1. HK-1A

2. HK-D

3. HK-E

4. HK-F

5. CP30

6. HK-4A & 4B (SEWA)

7. HK-11

# NOTA:Jika ada surat kelulusan Menteri untuktuntutan insentif/pengecualian, imbas danhantar.

BORANG P

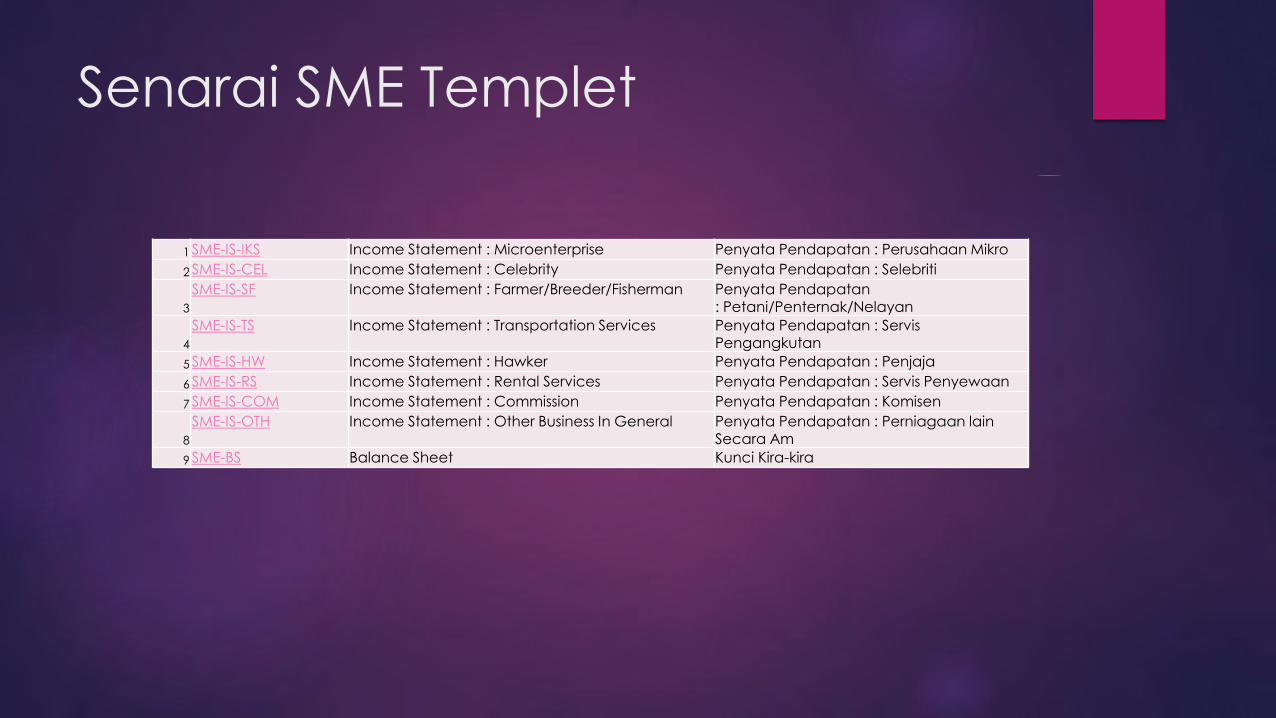

Senarai SME Templet

1 SME-IS-IKS Income Statement : Microenterprise Penyata Pendapatan : Perusahaan Mikro

2 SME-IS-CEL Income Statement : Celebrity Penyata Pendapatan : Selebriti

3

SME-IS-SF Income Statement : Farmer/Breeder/Fisherman Penyata Pendapatan

: Petani/Penternak/Nelayan

4

SME-IS-TS Income Statement : Transportation Services Penyata Pendapatan : Servis Pengangkutan

5 SME-IS-HW Income Statement : Hawker Penyata Pendapatan : Penjaja

6 SME-IS-RS Income Statement : Rental Services Penyata Pendapatan : Servis Penyewaan

7 SME-IS-COM Income Statement : Commission Penyata Pendapatan : Komisen

8

SME-IS-OTH Income Statement : Other Business In General Penyata Pendapatan : Perniagaan lain Secara Am

9 SME-BS Balance Sheet Kunci Kira-kira

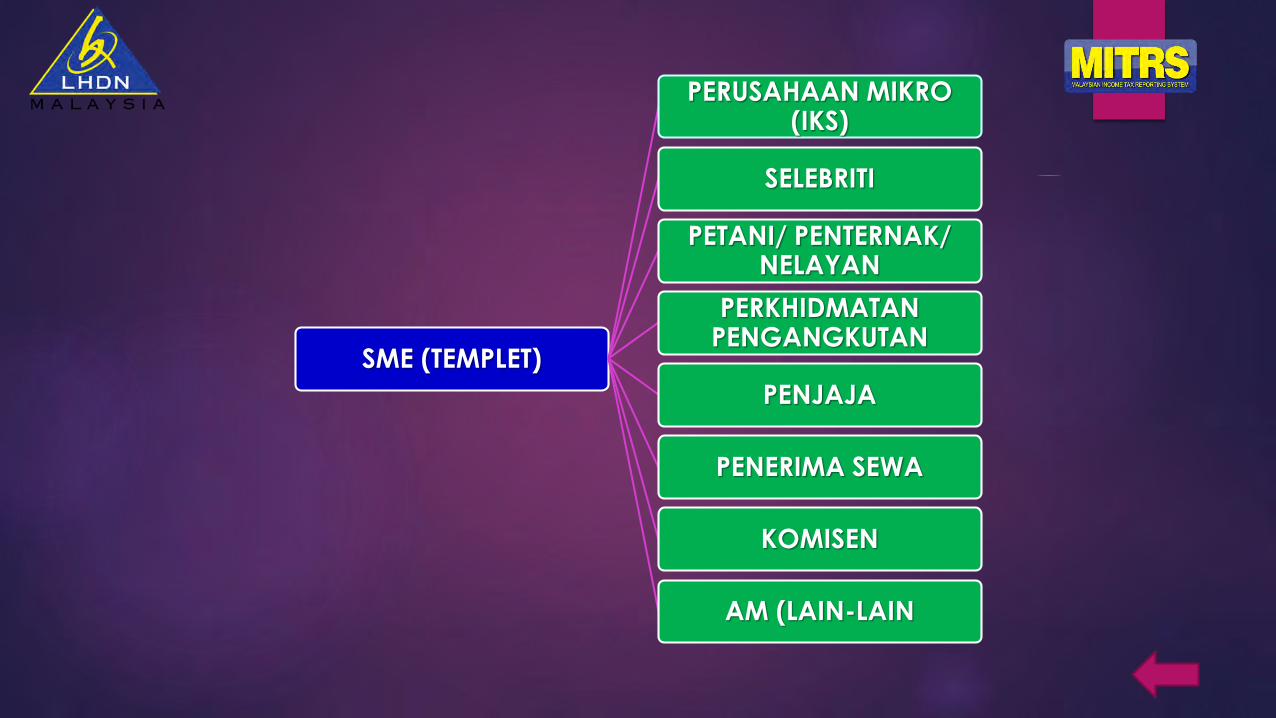

SME (TEMPLET)

PERUSAHAAN MIKRO (IKS)

SELEBRITI

PETANI/ PENTERNAK/ NELAYAN

PERKHIDMATAN PENGANGKUTAN

PENJAJA

PENERIMA SEWA

KOMISEN

AM (LAIN-LAIN

Top Related