![UniFi Network · Terangkan dge aruhan yang terhasil adalah dari aruhan kendiri. [6 marks] [6 markah] Sketch the complete graph of the rise and the fall of the current versus time](https://static.fdokumen.site/doc/165x107/60925b348d40c962497ddc62/unifi-terangkan-dge-aruhan-yang-terhasil-adalah-dari-aruhan-kendiri-6-marks-6.jpg)

Bahasa

Halaman

Undang-undang

TELEKOM MALAYSIA BERHADRHB INVESTMENT BANK REGIONAL CORPORATE DAY

KUALA LUMPUR19 JANUARY 2017

TM Today

Latest Updates

About TM

ANALOG

ERA

DIGITAL TECHNOLOGY

FULL-IP

TRANSFORMATION

at the leading edge of telecommunications in Malaysia

3

TM TODAY*…

MALAYSIA’S CONVERGENCE CHAMPION

No.1 Broadband provider in Malaysia

2.37mn broadband customers

RM8.82bn revenue as at YTD Sept 16, with 3.4% growth

More than 2.16mn HSBB fiber ports

356% Total Shareholder Return since demerger

• As at 30 September 2016• TSR as at 13 January 2017

4

Commercial launch of webe mobile service in Sept 2016

Latest Updates

TM 30th AGM 30 April 2015

Our Vision

Our Brand Values

Refocused PIP3.0

Our Guiding Values & Principles

Realigning our strategy: A refreshed Vision Statement aligned

toward Delivering Convergence and Life/Business Made Easier

6

Our digital transformation supported by Convergence

7

Business Priorities in Delivering Convergence and Going Digital

8

IMMEDIATE KEY FOCUS AREAS 2017 – 2019

ST

RA

TE

GIC

TH

RU

ST

S

REPRIORITISING PRODUCTIVITY

EMBEDDING INNOVATION

UN

DE

RL

YIN

G

PR

INC

IPL

ES

GO DIGITAL

DELIVER

Customer experience

“Generate easy and simpler

ways for customers to

engage with TM”

Process optimisation

“Simplify and streamline

internal processes through

digitalization”

New opportunities

“Create completely new adjacencies/

businesses enabled by digital”

To make life and business easier, for a better Malaysia, enabled by digital

Advanced analytics

Next-gen technology

Evolving organisation

Modernisedculture

1 2 3

Digital Capability

Going Digital for Life/Business Made Easier

7 Guiding Principles and 4 Key Programmes to create value through digitalization

(i) Customer Experience

(ii) Process Optimisation

(iii) Analytics and Omni-Channel

(iv) New adjacent/digital opportunities

Wave 1: Customer Journey Improvement on

track9

10

WE ARE STRATEGICALLY PLACED TO REALISE OUR CONVERGENCE AND

GOING DIGITAL ASPIRATIONS AS WE MOVE BEYOND CONNECTIVITY

B2B2C

B2B

DELIVER

GO DIGITAL

Smarter

BusinessesSmarter

Living

Smarter

Cities

Smarter

Communities

Smarter

Nation

1 2 3 4 5

&

• webe’s network made commercially available to the public from 30th September 2016

• To date more than 1500 sites operational

• Drive momentum toward Convergence by expanding product portfolios and digital services

webe: TM’s Mobility Centre of Excellence

11

Implementation of speed upgrade and introduction of new packages for non-Unifi customers in phases over 2017

12

Broadband Improvement Plan 2017

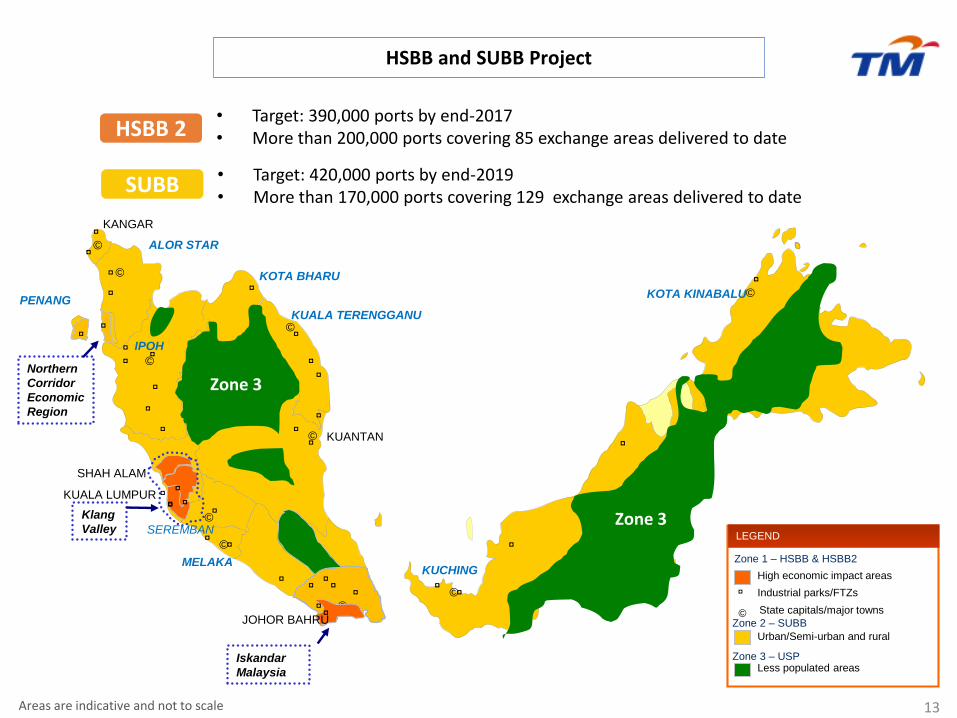

Areas are indicative and not to scale

KUALA TERENGGANU

©

©

©

©

©

©

©

KANGAR

ALOR STAR

IPOH

SHAH ALAM

MELAKA

KUANTAN

KUALA LUMPUR

Klang

Valley

◘

◘

◘

◘

◘

◘◘

◘

◘

◘◘

◘

◘

◘

◘

©

◘◘◘◘

◘

◘

◘

◘

◘

◘◘

◘

◘

◘

◘

◘

©

©KOTA KINABALU

KUCHING

◘

◘

◘

◘

©◘

◘◘

◘◘

Less populated areas

Zone 2 – SUBB

Zone 1 – HSBB & HSBB2

LEGEND

High economic impact areas

Urban/Semi-urban and rural

Industrial parks/FTZs

SEREMBAN

JOHOR BAHRU

Northern

Corridor

Economic

Region

Iskandar

Malaysia

Zone 3

Zone 3

Zone 3 – USP

HSBB and SUBB Project

13

KOTA BHARU

PENANG

State capitals/major towns©

• Target: 390,000 ports by end-2017 • More than 200,000 ports covering 85 exchange areas delivered to date

• Target: 420,000 ports by end-2019• More than 170,000 ports covering 129 exchange areas delivered to date

HSBB 2

SUBB

TM 31st AGM 28 April 2016

About TM

and

Performance Highlights

Capital StructureCredit Rating

Total Return To Shareholders

• Authorised Capital: RM3,528,003,015.00• Issued and Paid-up Capital: RM2,630,554,376.00• Date of Incorporation: 12 October 1984• Date of Listing: 7 November 1990

76.22%FBMKLCI1

356.42%TM1

9.71%AXIATA2

84.43%MAXIS3

234.41%DIGI1

• A3Moody’s

• A-S&P

• AAARAM

Source: Bloomberg1 For the period 22 April 2008 – 13 January 20172 For the period 25 April 2008 – 13 January 20173 For the period 18 November 2009 – 13 January 2017

• As at 13 January 2017• Foreign Shareholding as at 31 December 2016• EPF: Employees Provident Fund Board• Amanah Raya Berhad – for Skim Amanah Saham Bumiputra

About TM..

15

31%

13%

13%

17%

26%

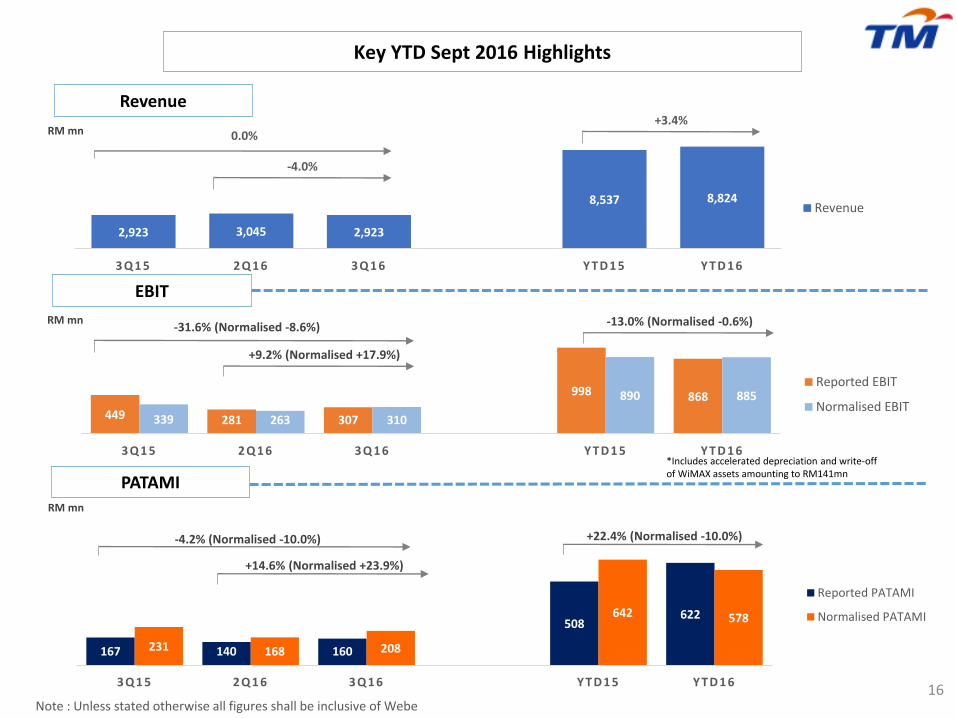

449 281 307

998 868

339 263 310

890 885

3 Q 1 5 2 Q 1 6 3 Q 1 6 Y T D 1 5 Y T D 1 6

Reported EBIT

Normalised EBIT

167 140 160

508622

231 168 208

642 578

3 Q 1 5 2 Q 1 6 3 Q 1 6 Y T D 1 5 Y T D 1 6

Reported PATAMI

Normalised PATAMI

2,923 3,045 2,923

8,537 8,824

3 Q 1 5 2 Q 1 6 3 Q 1 6 Y T D 1 5 Y T D 1 6

Revenue

0.0%

-31.6% (Normalised -8.6%)

RM mn

-4.0%

+9.2% (Normalised +17.9%)

Key YTD Sept 2016 Highlights

Revenue

EBIT

PATAMI

Note : Unless stated otherwise all figures shall be inclusive of Webe16

-4.2% (Normalised -10.0%)

+14.6% (Normalised +23.9%)

+3.4%

-13.0% (Normalised -0.6%)RM mn

RM mn

+22.4% (Normalised -10.0%)

*Includes accelerated depreciation and write-off of WiMAX assets amounting to RM141mn

495 603 541

1,476 1,620

3Q15 2Q16 3Q16 YTD15 YTD16

688 715 662

1,929 2,013

3Q15 2Q16 3Q16 YTD15 YTD16

845 905 919

2,506 2,717

3Q15 2Q16 3Q16 YTD15 YTD16

17

Group Total Revenue by Product

Voice

Internet

Note : Unless stated otherwise all figures shall be inclusive of Webe*Total revenue is after inter-co elimination.

RM mn

RM mn

Data

Others*

*Others comprise other telco and non-telco services (i.e ICT-BPO, MMU tuition fees, customer projects)

RM mn

RM mn

Voice28%

Internet 31%

Data23%

Others*18%

YTD Sept 16

Voice31%

Internet 29%

Data23%

Others*17%

YTD Sept 15

+4.4%-3.9%

-7.4%

+8.5%+8.8%

+1.5%

+9.8%+9.4%

-10.3%

895 823 801

2,627 2,473

3Q15 2Q16 3Q16 YTD15 YTD16

-10.4%

-2.6%

-5.8%

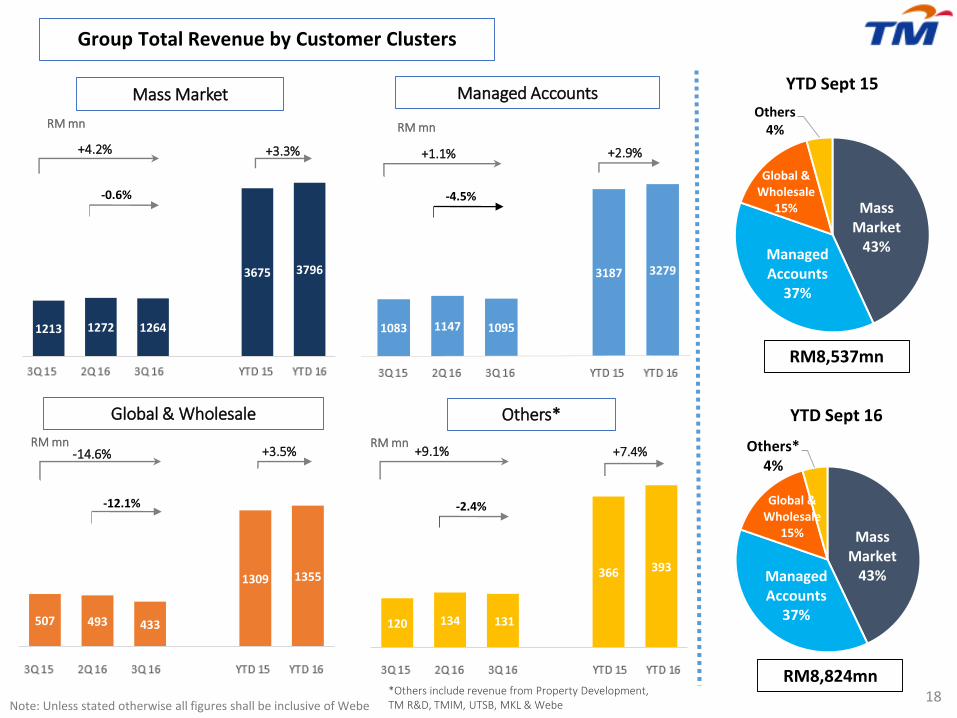

RM8,537mn

RM8,824mn

120 134 131

366 393

3Q 15 2Q 16 3Q 16 YTD Sep15

YTD Sep16

507 493 433

1309 1355

3Q 15 2Q 16 3Q 16 YTD Sep15

YTD Sep16

1213 1272 1264

3675 3796

3Q 15 2Q 16 3Q 16 YTD 15 YTD 16

Group Total Revenue by Customer Clusters

18

+4.2% +3.3%

Mass Market Managed Accounts

+1.1% +2.9%

Note: Unless stated otherwise all figures shall be inclusive of Webe

RM mn RM mn

-14.6%

Global & Wholesale

+3.5%

Others*

*Others include revenue from Property Development, TM R&D, TMIM, UTSB, MKL & Webe

+9.1% +7.4%

Mass Market

43%Managed Accounts

37%

Global & Wholesale

15%

Others*4%

YTD Sept 16

1083 1147 1095

3187 3279

Mass Market

43%Managed Accounts

37%

Global & Wholesale

15%

Others4%

YTD Sept 15

-0.6% -4.5%

-12.1% -2.4%

RM mnRM mn

RM8,537mn

RM8,824mn

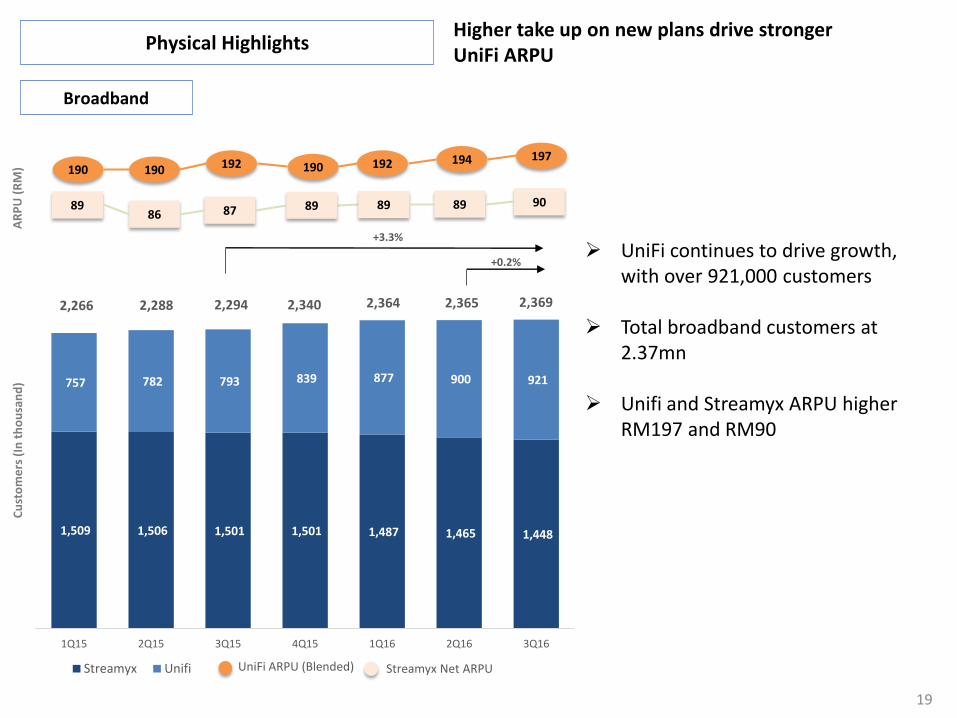

UniFi continues to drive growth, with over 921,000 customers

Total broadband customers at 2.37mn

Unifi and Streamyx ARPU higher RM197 and RM90

Higher take up on new plans drive stronger UniFi ARPU

19

Physical Highlights

Broadband

1,509 1,506 1,501 1,501 1,487 1,465 1,448

757 782 793 839 877 900 921

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Streamyx Unifi

+3.3%

190

+0.2%

86

Cu

sto

me

rs (

In t

ho

usa

nd

)A

RP

U (

RM

)

UniFi ARPU (Blended)

87

192

89

190

2,288 2,294 2,340 2,364

89

192

2,365

89

194

2,266

190

89 90

197

2,369

Streamyx Net ARPU

Note : Unless stated otherwise all figures shall be inclusive of Webe

Cost % of Revenue1

RM mn

Group Capital Expenditure

YTD Sept 2016: CAPEX & OPEX

Capex / Revenue (%)

20

22.2 21.9 21.5 21.1 21.8

18.8 19.3 18.8 17.9 19.0

21.4 20.4 22.2 21.9 21.3

11.7 11.7 11.7 9.4

11.7

5.9 6.2 5.8 6.5

6.0

6.0 6.7 6.6 6.7

6.5 3.3 4.1 3.7

3.0 3.7

1.0 0.6

(0.7)

1.9 0.3

1Q16 2Q16 3Q16 YTD15 YTD16

Dep & Amortisation Direct Costs Manpower

Other Operating Costs Maintenance Cost Supplies & Materials

Marketing Expenses Bad & Doubtful Debts

Total Cost / Revenue (%)

1 Revenue = Operating Revenue + Other Operating Income

88.4%

RM7,630.3 RM8,056.9

90.3%

RM2,795.9RM2,616.9

90.9%90.3%

RM2,644.1

89.6%

159 137

350

630 646

59

363

237

309

659

100

120128

214

348

1Q16 2Q16 3Q16 YTD15 YTD16

Core Network Access Support System

620318

20.4%11.1%

715

24.5%

1,153

13.5%

1,653

18.7%

21

Group Cash Flow

Note : Unless stated otherwise all figures shall be inclusive of Webe

RM mn YTD Sept 16 YTD Sept 15

Cash & cash equivalent at start 3,510.8 2,975.0

Cashflows from operating activities 1,459.1 1,577.7

Cashflows used-in investing activities (2,251.8) (1,631.6)

Capex 1,653.0 1,153.4

Cashflows from financing activities (126.5) (11.8)

Effect of exchange rate changes (0.4) 1.8

Cash & cash equivalent at end 2,591.2 2,911.1

Free cash-flow (EBITDA – Capex) 1,164.7 1,661.3

RM millionAs at

30 Sept 2016As at

31 Dec 2015

Shareholders’ Funds 7,522.1 7,780.6

Non-Controlling Interests 190.6 258.1

Deferred & Long Term Liabilities 11,022.8 10,551.8

Long Term Borrowings 7,525.9 7,175.4

Derivative financial instruments 288.0 321.9

Deferred tax liabilities 1,542.1 1,367.6

Deferred income 1,655.5 1,661.7

Trade and other payables 11.3 25.2

18,735.5 18,590.5

Current Assets 6,944.5 7,297.5

Trade Receivables 2,932.9 2,353.1

Other Receivables 595.4 594.0

Cash & Bank Balances 2,591.8 3,511.6

Others 824.4 838.8

Current Liabilities 5,453.2 5,822.6

Trade and Other Payables 3,560.2 4,367.0

Short Term Borrowings 399.7 408.3

Others 1,493.3 1,047.3

Net Current Assets/(Liabilities) 1,491.3 1,474.9

Property Plant & Equipment 15,245.0 15,186.9

Other Non-Current Assets 1,999.2 1,928.7

18,735.5 18,590.5

Group Balance Sheet

Note : Unless stated otherwise all figures shall be inclusive of Webe

22

Revenue Growth 3-3.5% 3.5-4%

3-5%

72 72

1 Using TRI*M index measuring end to end customer experience at all touch points. TRI*M (Measuring, Managing and Monitoring) is a standardized indicator system. It analyzes, measures and portrays stakeholder relationships on the basis of standardized indicators. The TRI*M Index is an indicator of the status quo of a particular relationship. The index is made up of four points of view on the stakeholder relationship, e.g. for customer loyalty: overall rating, recommendation, repeat purchasing of product/services, and a company's competitive advantage. The information is based on surveys/interviews on a sample customer base.”

*Note: Headline KPI are for TM Group excluding Webe

Headline KPI

2016

Revenue Growth

EBIT Growth

Customer Satisfaction Measure1

3-3.5%

Maintain as per 2015 RM level

2018

23

Appendix

24

10,629

11,235

11,722

FY2013 FY2014 FY2015

Revenue

Revenue EBIT

EBITDA PATAMI

RM mn RM mn

RM mn RM mn

+5.7% +4.3%-5.7% (Normalised +2.0%) -2.9% (Normalised -10.6%)

+2.9% (Normalised +5.9%) +1.6% (Normalised -1.3%)-17.8% (Normalised -9.4%) -15.8% (Normalised -4.9%)

Note: Unless stated otherwise, all figures shall be inclusive of Webe

*Excluding webe: Reported EBIT: RM1.53bn (+13.7%)Norm. EBIT: RM1.52bn (+6.2%)*Excluding webe:

RM11.52bn (+3.0%)

Group Results: 3-Year Performance

25

FY2013 FY2014 FY2015

*”Others” comprise other telco and non-telco services i.e ICT-BPO, MMU tuition fees, customer projects, Yellow Pages

Note: Unless stated otherwise, all figures shall be inclusive of Webe

31%

23%

27%

19%

34%

24%

25%

17%28%

23%

27%

22%

+3.7% +2.5%+11.9% -4.1% +1.1%

+0.6%+18.8%

RM mn RM mn RM mn RM mn

Internet Others*VoiceData

+12.4%

Change in revenue mix: non-voice revenue now 70%

Internet Data

3-Year Performance: Revenue by product

26Voice Others

RM10,629mn RM11,235mn RM11,722mn

Capex & Opex: 3-Year Performance

Total Capex

2,506

Capex / Revenue (%)

*Include Application, Support System & Others (building, land improvement, moveable plants, application & other assets)

Cost % of Revenue1

10,588.2

89.4%

RM mn

Total Cost / Revenue (%)

1 Revenue = Operating Revenue + Other Operating Income

Note: The classification of cost is as per financial reporting

21.4%

RM mn

9,378.3

87.2%

10,095.1

88.6%

1,863

17.5%

1,836

16.3%

3-Year Performance: Capex & Opex

27

41%59%

FY2013

1,580 1,502 1,501

635 729839

FY2013 FY2014 FY2015

Streamyx UniFi

In thousand+0.7%

2,3402,215 2,231

+4.9%

Broadband More customers upgrading to high speed packages

Evolving UniFi customer mix: more on 10Mbps or higher

Below 4Mbps4Mbps and above

Below 10Mbps10Mbps and above

3-Year Performance: Physical Highlights

28

38% 62%

3Q2016

88%

12%

FY2013

25% 75%

3Q2016

webe mobile and webe broadband plans

29

Telekom Malaysia Berhad ("the Company" or "TM") issues a statement to reiterate its stand on the Company's dividend policy. The

Company’s dividend policy as announced at the time of the demerger between TM and TM International Berhad (TMI) remains

valid. The policy states as follows:

“In determining the dividend payout ratio in respect of any financial year after the Proposed Demerger, our Company intends to

adopt a progressive dividend policy which enables us to provide stable and sustainable dividends to our shareholders while

maintaining an efficient capital structure and ensuring sufficiency of funding for future growth.

Upon completion of the Proposed Demerger, our Company intends to distribute yearly dividends of RM700 million or up to 90% of

our normalised PATAMI, whichever is higher.

Dividends will be paid only if approved by our Board out of funds available for such distribution. The actual amount and timing of

dividend payments will depend upon our level of cash and retained earnings, results of operations, business prospects,

monetization of non-core assets, projected levels of capital expenditure and other investment plans, current and expected

obligations and such other matters as our Board may deem relevant.”

This policy remains unchanged for 2009 and beyond. The Company is currently able to meet this dividend policy, because:

• The Company has sufficient consolidated cash and bank balances of RM1.144 billion as at 30 September 2008, and it is

confident that TMI is able to meet its obligation due to TM of RM4.025 billion by April 2009.

• In the event of a downturn in performance due to unforeseen circumstances, the Company wishes to state that its recurring cash

generation ability is sufficient to meet its current dividend policy.

• TM’s retained earnings is also sufficient to support this current dividend policy in the event of unforeseen shortfalls in normalised

PATAMI.

Given the unprecedented volatility in global markets, the Company will continue to examine the likely impact on its business,

cashflow generation, capital structure and methods in which excess cash beyond the dividend policy and prudent level of cash

required for operations, can be efficiently distributed to our shareholders.

Moving forward, TM is focused on building a strong foundation for its future growth and operational excellence.

TELEKOM MALAYSIA BERHAD (Bursa Malaysia Announcement Reference No TM-081113-37325)

Date Announced :13/11/2008

Reiteration of Dividend Policy

30

150.9124.2

110.5

89.389.9 90.0

89.9

6.5

5.6

4.03.6

4.7

3.3 3.2

Shareholder Returns (2009-2015)

Dividend Payout Policy of RM700mn or up to 90.0% of Normalised PATAMI whichever is higher

RM mn

Payout Ratio3

(%)

Net Dividend Yield2

(%)

1 2015 1st Interim Dividend of 9.3 sen per share and 2nd Interim Dividend of 12.1 sen per share2 Net Dividend Yield based on closing share price at year end3 Excludes Capital Distributions/Repayment

31

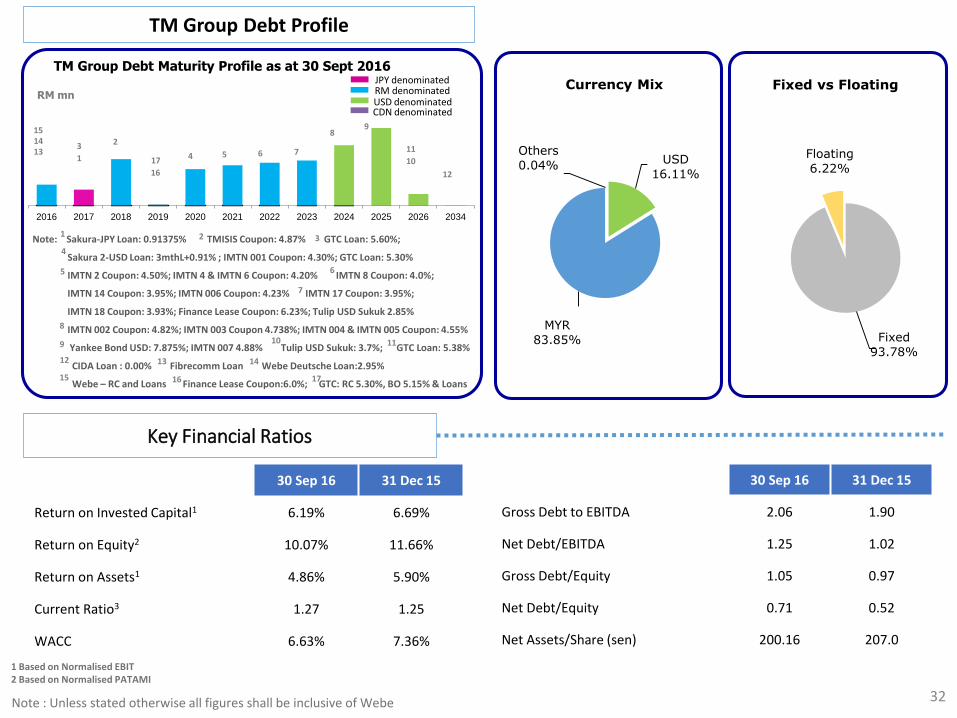

TM Group Debt Profile

32

Key Financial Ratios

1 Based on Normalised EBIT2 Based on Normalised PATAMI

Note : Unless stated otherwise all figures shall be inclusive of Webe

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2034

TM Group Debt Maturity Profile as at 30 Sept 2016

RM mn

Note: Sakura-JPY Loan: 0.91375% TMISIS Coupon: 4.87% GTC Loan: 5.60%;

Sakura 2-USD Loan: 3mthL+0.91% ; IMTN 001 Coupon: 4.30%; GTC Loan: 5.30%

IMTN 2 Coupon: 4.50%; IMTN 4 & IMTN 6 Coupon: 4.20% IMTN 8 Coupon: 4.0%;

IMTN 14 Coupon: 3.95%; IMTN 006 Coupon: 4.23% IMTN 17 Coupon: 3.95%;

IMTN 18 Coupon: 3.93%; Finance Lease Coupon: 6.23%; Tulip USD Sukuk 2.85%

IMTN 002 Coupon: 4.82%; IMTN 003 Coupon 4.738%; IMTN 004 & IMTN 005 Coupon: 4.55%

Yankee Bond USD: 7.875%; IMTN 007 4.88% Tulip USD Sukuk: 3.7%; GTC Loan: 5.38%

CIDA Loan : 0.00% Fibrecomm Loan Webe Deutsche Loan:2.95%

Webe – RC and Loans Finance Lease Coupon:6.0%; GTC: RC 5.30%, BO 5.15% & Loans

1 2 3

5 6

5

8

9 10

12

JPY denominatedRM denominatedUSD denominatedCDN denominated

1

2

4 76

98

11

10

12

13

7

3

4

14

14

15

15

13

11

17 16

17

16

USD

16.11%

MYR

83.85%

Others

0.04%

Currency Mix

Fixed

93.78%

Floating

6.22%

Fixed vs Floating

30 Sep 16 31 Dec 15

Return on Invested Capital1 6.19% 6.69%

Return on Equity2 10.07% 11.66%

Return on Assets1 4.86% 5.90%

Current Ratio3 1.27 1.25

WACC 6.63% 7.36%

30 Sep 16 31 Dec 15

Gross Debt to EBITDA 2.06 1.90

Net Debt/EBITDA 1.25 1.02

Gross Debt/Equity 1.05 0.97

Net Debt/Equity 0.71 0.52

Net Assets/Share (sen) 200.16 207.0

THANK YOUInvestor Relations

Level 11 (South Wing), Menara TMJalan Pantai Baharu50672 Kuala Lumpur

MalaysiaTel: (603) 2240 4848/ 7366 / 7388

Top Related